Supplementary Panel Data Recordings

TA Session 4: Panel Data and the Error Covariance Matrix | Script

TA Session 5: Estimation of the Error Covariance Matrix and the GLS Estimator | Script

TA Session 6: FGLS Estimator | Script

TA Session 7: Transformation Matrices and the Between Estimator | Script

TA Session 8: Within and First-Difference Estimators | Script

Data Structure

- Section 2.1.1 of “Panel Data Econometrics with R” (Croissant & Millo, 2018)

- Most notation follows the Econometrics I lecture notes.

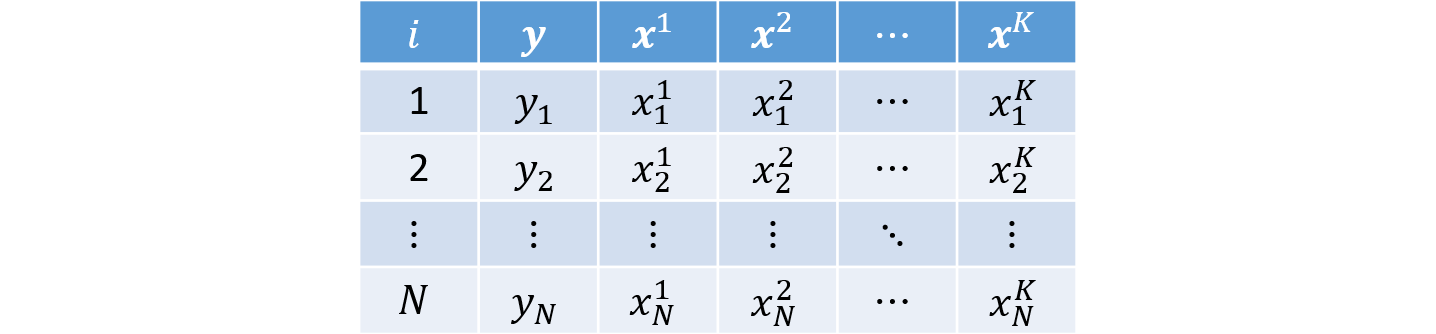

Cross-Section

So far, we have worked with cross-sectional datasets, that is, samples in which each row represents one individual $i = 1, ..., N$ and we observe realizations of the dependent variable $y$ and the explanatory variables $k = 1, 2, ..., K$:

Example

Consider $N = 4$ individuals and $K = 2$ covariates:

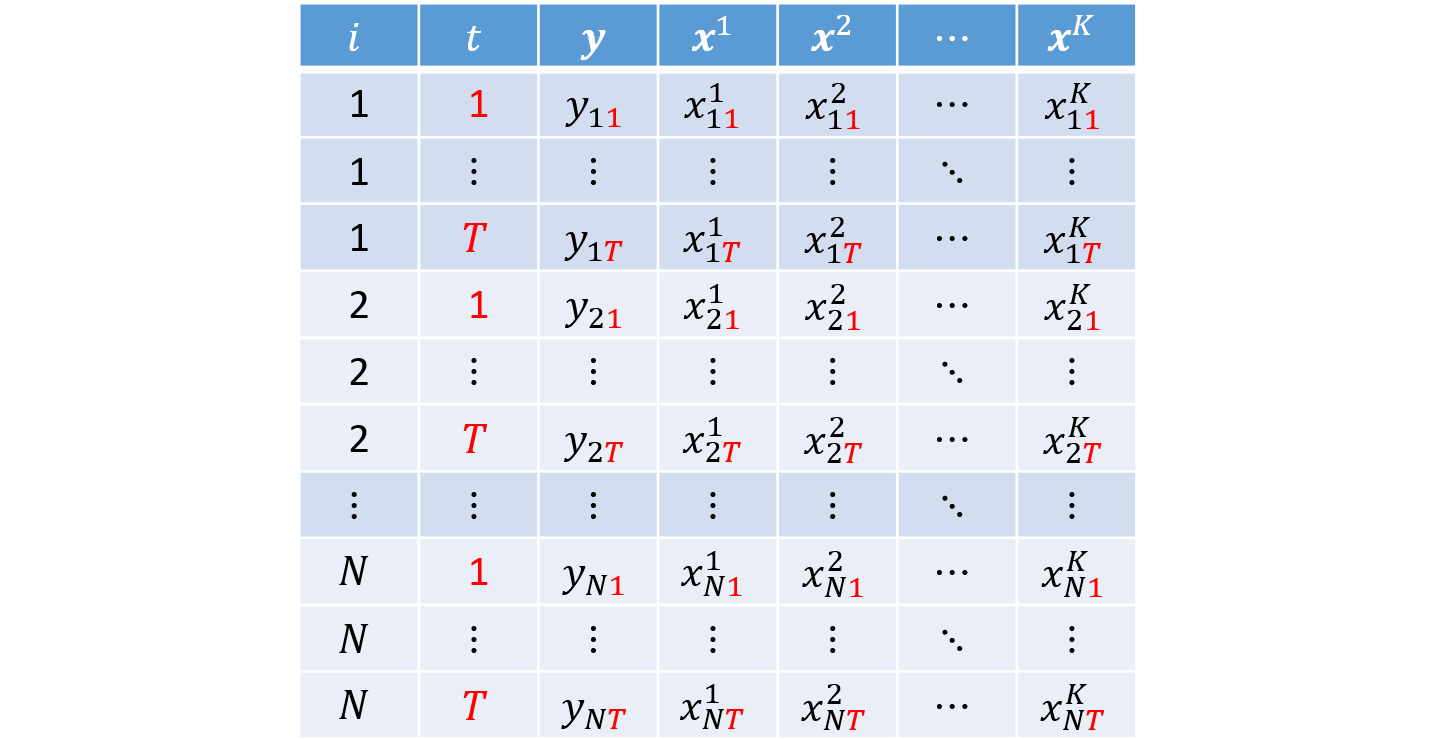

Panel Data

It is also common to work with panel data, that is, datasets in which we observe the same individuals $i = 1, ..., N$ over $t = 1, ..., T$ periods.

This type of structure allows us not only to compare individuals (between), but also to study within-individual variation (within) over time.

For simplicity, we assume a balanced panel, so every individual is observed for the same $T$ periods. Panel data can be organized in either long or wide format.

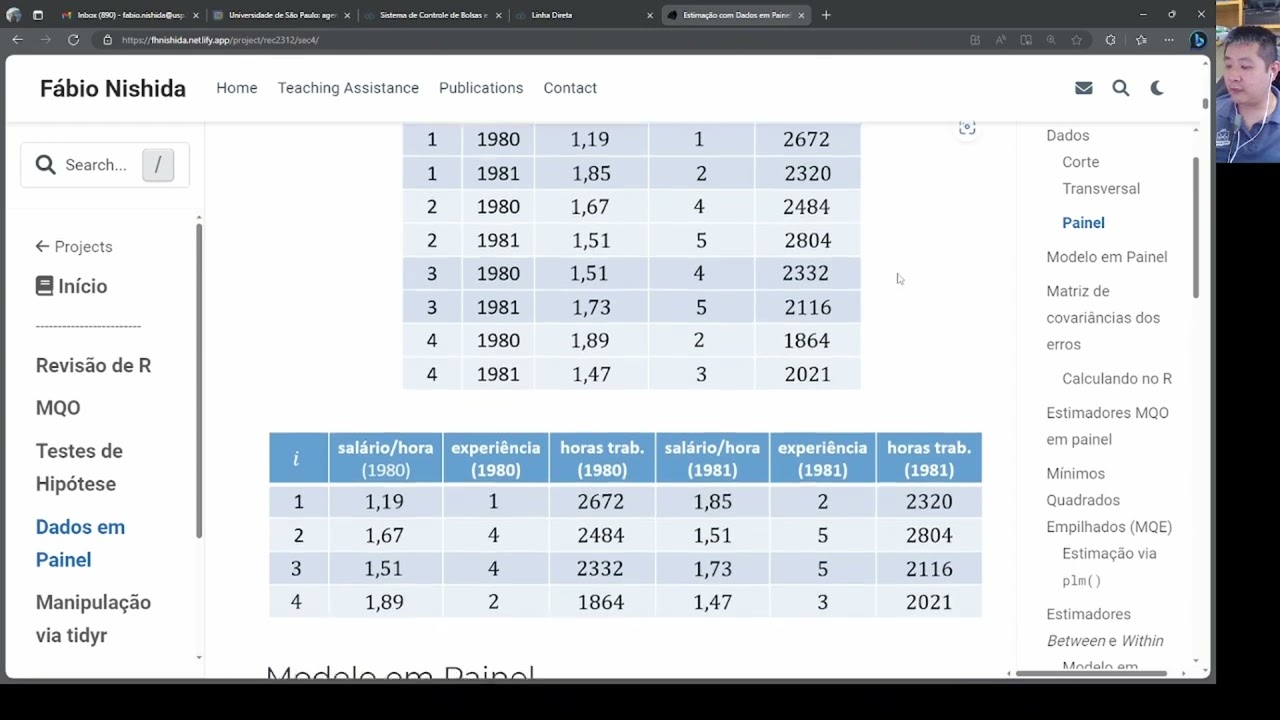

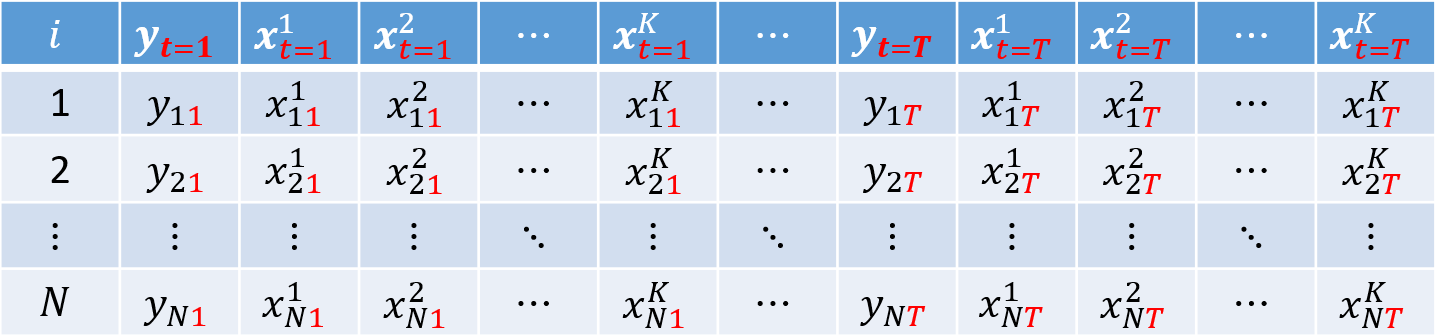

Panel Data in Long Format (long)

In long format, each individual appears in $T$ rows. Each observation is indexed by the pair $i$ and $t$, which serve as the key identifiers in the dataset. This is the standard layout used in econometrics.

Panel Data in Wide Format (wide)

In wide format, the dependent and explanatory variables appear repeated across $T$ columns, with each repetition corresponding to one of the $T$ periods:

Examples

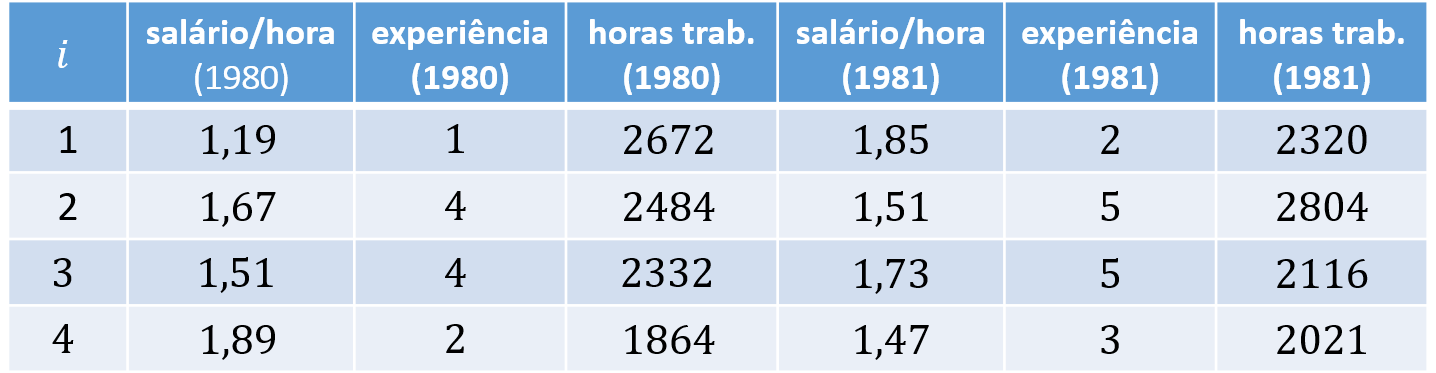

As an example, consider $N = 4$ individuals, $K = 2$ covariates, and $T = 2$ periods. The corresponding long and wide panel layouts are:

Panel Data Model

For observation $(i,t)$, we can write the model as:

$$ y_{it} = \boldsymbol{x}'_{it} \boldsymbol{\beta} + \varepsilon_{it} \tag{1} $$ where $\boldsymbol{\beta}$ is the column vector of parameters

$$ \boldsymbol{\beta} = \left[ \begin{array}{c} \beta_0 \\ \beta_1 \\ \beta_2 \\ \vdots \\ \beta_K \end{array} \right], $$$y_{it}$ is the dependent variable, and $\boldsymbol{x}'_{it}$ is the row vector of dimension $K+1$:

$$ \boldsymbol{x}'_{it} = \left[ \begin{array}{c} 1 & x^1_{it} & x^2_{it} & \cdots & x^K_{it} \end{array} \right], $$and the error $\varepsilon_{it}$ can be written as:

$$ \varepsilon_{it} = u_i + v_{it}, $$ where $u_i$ is the individual-specific error component for individual $i$, and $v_{it}$ is the idiosyncratic error.

Stacking equation (1) over all individuals $i = 1, 2, ..., N$ and periods $t = 1, 2, ..., T$, we obtain

$$ \underbrace{\boldsymbol{y}}_{NT \times 1} = \left[ \begin{array}{c} y_{11} \\ y_{12} \\ \vdots \\ y_{1T} \\\hline y_{21} \\ y_{22} \\ \vdots \\ y_{2T} \\\hline \vdots \\\hline y_{N1} \\ y_{N2} \\ \vdots \\ y_{NT} \end{array} \right] \quad \text{and} \quad \underbrace{\boldsymbol{X}}_{NT \times K} = \left[ \begin{array}{c} \boldsymbol{x}'_{11} \\ \boldsymbol{x}'_{12} \\ \vdots \\ \boldsymbol{x}'_{1T} \\\hline \boldsymbol{x}'_{21} \\ \boldsymbol{x}'_{22} \\ \vdots \\ \boldsymbol{x}'_{2T} \\\hline \vdots \\\hline \boldsymbol{x}'_{N1} \\ \boldsymbol{x}'_{N2} \\ \vdots \\ \boldsymbol{x}'_{NT} \end{array} \right] = \left[ \begin{array}{ccccc} 1 & x^1_{11} & x^2_{11} & \cdots & x^K_{11} \\ 1 & x^1_{12} & x^2_{12} & \cdots & x^K_{12} \\ \vdots & \vdots & \vdots & \ddots & \vdots \\ 1 & x^1_{1T} & x^2_{1T} & \cdots & x^K_{1T} \\\hline 1 & x^1_{21} & x^2_{21} & \cdots & x^K_{21} \\ 1 & x^1_{22} & x^2_{22} & \cdots & x^K_{22} \\ \vdots & \vdots & \vdots & \ddots & \vdots \\ 1 & x^1_{2T} & x^2_{2T} & \cdots & x^K_{2T} \\\hline \vdots & \vdots & \vdots & \ddots & \vdots \\\hline 1 & x^1_{N1} & x^2_{N1} & \cdots & x^K_{N1} \\ 1 & x^1_{N2} & x^2_{N2} & \cdots & x^K_{N2} \\ \vdots & \vdots & \vdots & \ddots & \vdots \\ 1 & x^1_{NT} & x^2_{NT} & \cdots & x^K_{NT} \end{array} \right] $$ The horizontal separators are included only to make it easier to visualize the rows associated with each individual $i$.

Error Variance-Covariance Matrix

- Section 2.2 of “Panel Data Econometrics with R” (Croissant & Millo, 2018)

The error variance-covariance matrix links one error term, $\varepsilon_{it}$, to every other error term $\varepsilon_{js}$, for all $j = 1, ..., N$ and $s = 1, ..., T$.

In this matrix, each row represents one $\varepsilon_{it}$ and each column represents one $\varepsilon_{js}$. Each entry gives the covariance between $\varepsilon_{it}$ and $\varepsilon_{js}$; when $\varepsilon_{it} = \varepsilon_{js}$, the entry is a variance term:

$$ cov(\boldsymbol{\varepsilon}) = \underset{NT \times NT}{\boldsymbol{\Sigma}} =$$ $$ \left[ \tiny \begin{array}{cccc|ccc|c|ccc} var(\varepsilon_{{\color{red}1}1}) & cov(\varepsilon_{{\color{red}1}1}, \varepsilon_{{\color{red}1}2}) & \cdots & cov(\varepsilon_{{\color{red}1}1}, \varepsilon_{{\color{red}1}T}) & cov(\varepsilon_{{\color{red}1}1}, \varepsilon_{{\color{red}2}1}) & \cdots & cov(\varepsilon_{{\color{red}1}1}, \varepsilon_{{\color{red}2}T}) & \cdots & cov(\varepsilon_{{\color{red}1}1}, \varepsilon_{{\color{red}N}1}) & \cdots & cov(\varepsilon_{{\color{red}1}1}, \varepsilon_{{\color{red}N}T}) \\ cov(\varepsilon_{{\color{red}1}2}, \varepsilon_{{\color{red}1}1}) & var(\varepsilon_{{\color{red}1}2}) & \cdots & cov(\varepsilon_{{\color{red}1}2}, \varepsilon_{{\color{red}1}T}) & cov(\varepsilon_{{\color{red}1}2}, \varepsilon_{{\color{red}2}1}) & \cdots & cov(\varepsilon_{{\color{red}1}2}, \varepsilon_{{\color{red}2}T}) & \cdots & cov(\varepsilon_{{\color{red}1}2}, \varepsilon_{{\color{red}N}1}) & \cdots & cov(\varepsilon_{{\color{red}1}2}, \varepsilon_{{\color{red}N}T}) \\ \vdots & \vdots & \ddots & \vdots & \vdots & \ddots & \vdots & \ddots & \vdots & \ddots & \vdots \\ cov(\varepsilon_{{\color{red}1}T}, \varepsilon_{{\color{red}1}1}) & cov(\varepsilon_{{\color{red}1}T}, \varepsilon_{{\color{red}1}2}) & \cdots & var(\varepsilon_{{\color{red}1}T}) & cov(\varepsilon_{{\color{red}1}T}, \varepsilon_{{\color{red}2}1}) & \cdots & cov(\varepsilon_{{\color{red}1}T}, \varepsilon_{{\color{red}2}T}) & \cdots & cov(\varepsilon_{{\color{red}1}T}, \varepsilon_{{\color{red}N}1}) & \cdots & cov(\varepsilon_{{\color{red}1}T}, \varepsilon_{{\color{red}N}T}) \\ \hline cov(\varepsilon_{{\color{red}2}1}, \varepsilon_{{\color{red}1}1}) & cov(\varepsilon_{{\color{red}2}1}, \varepsilon_{{\color{red}1}2}) & \cdots & cov(\varepsilon_{{\color{red}2}1}, \varepsilon_{{\color{red}1}T}) & var(\varepsilon_{{\color{red}2}1}) & \cdots & cov(\varepsilon_{{\color{red}2}1}, \varepsilon_{{\color{red}2}T}) & \cdots & cov(\varepsilon_{{\color{red}2}1}, \varepsilon_{{\color{red}N}1}) & \cdots & cov(\varepsilon_{{\color{red}2}1}, \varepsilon_{{\color{red}N}T}) \\ \vdots & \vdots & \ddots & \vdots & \vdots & \ddots & \vdots & \ddots & \vdots & \ddots & \vdots \\ cov(\varepsilon_{{\color{red}2}T}, \varepsilon_{{\color{red}1}1}) & cov(\varepsilon_{{\color{red}2}T}, \varepsilon_{{\color{red}1}2}) & \cdots & cov(\varepsilon_{{\color{red}2}T}, \varepsilon_{{\color{red}1}T}) & cov(\varepsilon_{{\color{red}2}T}, \varepsilon_{{\color{red}2}1}) & \cdots & var(\varepsilon_{{\color{red}2}T}) & \cdots & cov(\varepsilon_{{\color{red}2}T}, \varepsilon_{{\color{red}N}1}) & \cdots & cov(\varepsilon_{{\color{red}2}T}, \varepsilon_{{\color{red}N}T}) \\ \hline \vdots & \vdots & \ddots & \vdots & \vdots & \ddots & \vdots & \ddots & \vdots & \ddots & \vdots \\ \hline cov(\varepsilon_{{\color{red}N}1}, \varepsilon_{{\color{red}1}1}) & cov(\varepsilon_{{\color{red}N}1}, \varepsilon_{{\color{red}1}2}) & \cdots & cov(\varepsilon_{{\color{red}N}1}, \varepsilon_{{\color{red}1}T}) & cov(\varepsilon_{{\color{red}N}1}, \varepsilon_{{\color{red}2}1}) & \cdots & cov(\varepsilon_{{\color{red}N}1}, \varepsilon_{{\color{red}2}T}) & \cdots & var(\varepsilon_{{\color{red}N}1}) & \cdots & cov(\varepsilon_{{\color{red}N}1}, \varepsilon_{{\color{red}N}T}) \\ \vdots & \vdots & \ddots & \vdots & \vdots & \ddots & \vdots & \ddots & \vdots & \ddots & \vdots \\ cov(\varepsilon_{{\color{red}N}T}, \varepsilon_{{\color{red}1}1}) & cov(\varepsilon_{{\color{red}N}T}, \varepsilon_{{\color{red}1}2}) & \cdots & cov(\varepsilon_{{\color{red}N}T}, \varepsilon_{{\color{red}1}T}) & cov(\varepsilon_{{\color{red}N}T}, \varepsilon_{{\color{red}2}1}) & \cdots & cov(\varepsilon_{{\color{red}N}T}, \varepsilon_{{\color{red}2}T}) & \cdots & cov(\varepsilon_{{\color{red}N}T}, \varepsilon_{{\color{red}N}1}) & \cdots & var(\varepsilon_{{\color{red}N}T}) \end{array} \right]$$

Note that the error variance-covariance matrix can be partitioned into smaller blocks linking the errors of individual $i$ (row block) and individual $j$ (column block). To write $\boldsymbol{\Sigma}$ more compactly, we denote these blocks by $\boldsymbol{\Sigma}_{ij}$:

$$ \underset{NT \times NT}{\boldsymbol{\Sigma}} = \left[ \begin{matrix} \boldsymbol{\Sigma}_1 & \boldsymbol{\Sigma}_{12} & \cdots & \boldsymbol{\Sigma}_{1N} \\ \boldsymbol{\Sigma}_{21} & \boldsymbol{\Sigma}_{2} & \cdots & \boldsymbol{\Sigma}_{2N} \\ \vdots & \vdots & \ddots & \vdots \\ \boldsymbol{\Sigma}_{N1} & \boldsymbol{\Sigma}_{N2} & \cdots & \boldsymbol{\Sigma}_{N} \end{matrix} \right] \tag{1} $$where, when $i = j$, we have

$$ \underset{T \times T}{\boldsymbol{\Sigma}_i} = \left[ \begin{matrix} var(\varepsilon_{i1}) & cov(\varepsilon_{i1}, \varepsilon_{i2}) & \cdots & cov(\varepsilon_{i1}, \varepsilon_{iT}) \\ cov(\varepsilon_{i1}, \varepsilon_{i2}) & var(\varepsilon_{i2}) & \cdots & cov(\varepsilon_{i2}, \varepsilon_{iT}) \\ \vdots & \vdots & \ddots & \vdots \\ cov(\varepsilon_{i1}, \varepsilon_{iT}) & cov(\varepsilon_{i2}, \varepsilon_{iT}) & \cdots & var(\varepsilon_{iT}) \end{matrix} \right] \tag{2} $$and, when $i \neq j$, we have $$ \underset{T \times T}{\boldsymbol{\Sigma}_{ij}} = \left[ \begin{matrix} cov(\varepsilon_{i1}, \varepsilon_{j1}) & cov(\varepsilon_{i1}, \varepsilon_{j2}) & \cdots & cov(\varepsilon_{i1}, \varepsilon_{jT}) \\ cov(\varepsilon_{i1}, \varepsilon_{j2}) & cov(\varepsilon_{i2}, \varepsilon_{j2}) & \cdots & cov(\varepsilon_{i2}, \varepsilon_{jT}) \\ \vdots & \vdots & \ddots & \vdots \\ cov(\varepsilon_{i1}, \varepsilon_{jT}) & cov(\varepsilon_{i2}, \varepsilon_{jT}) & \cdots & cov(\varepsilon_{iT}, \varepsilon_{jT}) \end{matrix} \right]. \tag{3} $$

Because we assume random sampling, the covariance between two distinct individuals

$(i \neq j)$ is

$$ cov(\varepsilon_{it}, \varepsilon_{jt}) = cov(\varepsilon_{it}, \varepsilon_{js}) = 0, \qquad \text{for all } i \neq j.$$

Therefore, $\boldsymbol{\Sigma}_{ij} = \boldsymbol{0}$ (the zero matrix): $$ \underset{T \times T}{\boldsymbol{\Sigma}_{ij}} = \underset{T \times T}{\boldsymbol{0}} = \left[ \begin{matrix} 0 & 0 & \cdots & 0 \\ 0 & 0 & \cdots & 0 \\ \vdots & \vdots & \ddots & \vdots \\ 0 & 0 & \cdots & 0 \end{matrix} \right] $$

Therefore, we can rewrite (1) as

$$ \underset{NT \times NT}{\boldsymbol{\Sigma}} = \left[ \begin{matrix} \boldsymbol{\Sigma}_1 & \boldsymbol{0} & \cdots & \boldsymbol{0} \\ \boldsymbol{0} & \boldsymbol{\Sigma}_2 & \cdots & \boldsymbol{0} \\ \vdots & \vdots & \ddots & \vdots \\ \boldsymbol{0} & \boldsymbol{0} & \cdots & \boldsymbol{\Sigma}_N \end{matrix} \right]. \tag{1'} $$We also assume that the individual-level error variance-covariance matrix depends only on $\sigma^2_u$ and $\sigma^2_v$, because:

- Variance of a single error term: $ var(\varepsilon_{it}) = \sigma^2_u + \sigma^2_v $

- Covariance between two errors for the same individual $i$ across periods $t \neq s$: $ cov(\varepsilon_{it}, \varepsilon_{is}) = \sigma^2_u $

Substituting into (2), we obtain

$$ \underset{T \times T}{\boldsymbol{\Sigma}_i} = \left[ \begin{array}{cccc} \sigma^2_u + \sigma^2_v & \sigma^2_u & \cdots & \sigma^2_u \\ \sigma^2_u & \sigma^2_u + \sigma^2_v & \cdots & \sigma^2_u \\ \vdots & \vdots & \ddots & \vdots \\ \sigma^2_u & \sigma^2_u & \cdots & \sigma^2_u + \sigma^2_v \end{array} \right] \tag{2'} $$Example

For simplicity, let $N = 2$ and $T = 3$. Then the error variance-covariance matrix can be written as:

\begin{align} \underset{6 \times 6}{\boldsymbol{\Sigma}} &= \left[ \begin{array}{cc} \boldsymbol{\Sigma}_1 & \boldsymbol{0} \\ \boldsymbol{0} & \boldsymbol{\Sigma}_2 \end{array} \right] \\ &= \left[ \begin{array} {ccc|ccc} \sigma^2_u + \sigma^2_v & \sigma^2_u & \sigma^2_u & 0 & 0 & 0 \\ \sigma^2_u & \sigma^2_u + \sigma^2_v & \sigma^2_u & 0 & 0 & 0 \\ \sigma^2_u & \sigma^2_u & \sigma^2_u + \sigma^2_v & 0 & 0 & 0\\ \hline 0 & 0 & 0 & \sigma^2_u + \sigma^2_v & \sigma^2_u & \sigma^2_u \\ 0 & 0 & 0 & \sigma^2_u & \sigma^2_u + \sigma^2_v & \sigma^2_u \\ 0 & 0 & 0 & \sigma^2_u & \sigma^2_u & \sigma^2_u + \sigma^2_v \\ \end{array} \right] \end{align}The vertical and horizontal separators above are included only to highlight which elements belong to each block matrix.

Computing It in R

First, let $I_p$ denote the identity matrix of dimension $p \times p$:

$$ \boldsymbol{I}_p= \left[ \begin{array}{cccc} 1 & 0 & 0 & \cdots & 0 \\ 0 & 1 & 0 & \cdots & 0 \\ 0 & 0 & 1 & \cdots & 0 \\ \vdots & \vdots & \vdots & \ddots & \vdots \\ 0 & 0 & 0 & \cdots & 1 \end{array} \right]_{p \times p}, $$and let $\boldsymbol{\iota}_q$ denote a column vector of ones of length $q$: $$ \boldsymbol{\iota}_q = \left[ \begin{array}{c} 1 \\ 1 \\ \vdots \\ 1 \end{array} \right]_{q \times 1} $$

With cross-sectional data, the error variance-covariance matrix is straightforward because there is only one error component, so $\sigma^2$ appears only on the main diagonal:

\begin{align} \boldsymbol{\Sigma}_{\scriptscriptstyle{OLS}} &= \sigma^2 \boldsymbol{I}_N \\ &= \sigma^2 \left[ \begin{array}{cccc} 1 & 0 & \cdots & 0 \\ 0 & 1 & \cdots & 0 \\ \vdots & \vdots & \ddots & \vdots \\ 0 & 0 & \cdots & 1 \end{array} \right] \\ &= \left[ \begin{array}{cccc} \sigma^2 & 0 & \cdots & 0 \\ 0 & \sigma^2 & \cdots & 0 \\ \vdots & \vdots & \ddots & \vdots \\ 0 & 0 & \cdots & \sigma^2 \end{array} \right]_{N \times N} \end{align}For panel data, however, we have two error-component variances. The term $\sigma^2_v$ appears on the main diagonal, while the common individual effect adds $\sigma^2_u$ to all within-individual entries. Therefore, the panel-data error variance-covariance matrix can be written as:

$$ \boldsymbol{\Sigma} = \sigma^2_v \boldsymbol{I}_{NT} + T \sigma^2_u [\boldsymbol{I}_N \otimes \boldsymbol{\iota}_T (\boldsymbol{\iota}'_T \boldsymbol{\iota}_T)^{-1} \boldsymbol{\iota}'_T] \tag{4} $$Note that the first term in the sum creates a main diagonal of $\sigma^2_v$.

\begin{align} \sigma^2_v \boldsymbol{I}_{NT} &= \sigma^2_v \left[ \begin{array}{cccc} 1 & 0 & \cdots & 0 \\ 0 & 1 & \cdots & 0 \\ \vdots & \vdots & \ddots & \vdots \\ 0 & 0 & \cdots & 1 \end{array} \right] \\ &= \left[ \begin{array}{cccc} \sigma^2_v & 0 & \cdots & 0 \\ 0 & \sigma^2_v & \cdots & 0 \\ \vdots & \vdots & \ddots & \vdots \\ 0 & 0 & \cdots & \sigma^2_v \end{array} \right]_{NT \times NT} \end{align}Now we only need to add $\sigma^2_u$ to the entries around that diagonal.

For the moment, ignore $T \sigma^2_u$ and denote the bracketed term by the between (inter-individual) transformation matrix:

$$ \boldsymbol{B}\ \equiv\ \boldsymbol{I}_N \otimes \Big[ \boldsymbol{\iota}_T (\boldsymbol{\iota}'_T \boldsymbol{\iota}_T)^{-1} \boldsymbol{\iota}'_T \Big] $$Note that the matrix $\boldsymbol{B}$ is denoted by $\boldsymbol{N}$ in Professor Daniel’s 2021 Econometrics II lecture notes.

\begin{align} \boldsymbol{B} &\equiv \boldsymbol{I}_{N} \otimes \boldsymbol{\iota}_T (\boldsymbol{\iota}'_T \boldsymbol{\iota}_T)^{-1} \boldsymbol{\iota}'_T \\ &= \left[ \begin{array}{cc} 1 & \cdots & 0 \\ \vdots & \ddots & \vdots \\ 0 & \cdots & 1 \end{array} \right] \otimes \left( \left[ \begin{array}{c} 1 \\ \vdots \\ 1 \end{array} \right] \left( \left[ \begin{array}{ccc} 1 & \cdots & 1 \end{array} \right] \left[ \begin{array}{c} 1 \\ \vdots \\ 1 \end{array} \right] \right)^{-1} \left[ \begin{array}{ccc} 1 & \cdots & 1 \end{array} \right] \right) \\ &= \left[ \begin{array}{cc} 1 & \cdots & 0 \\ \vdots & \ddots & \vdots \\ 0 & \cdots & 1 \end{array} \right] \otimes \left( \left[ \begin{array}{c} 1 \\ \vdots \\ 1 \end{array} \right] \left( T \right)^{-1} \left[ \begin{array}{ccc} 1 & \cdots & 1 \end{array} \right] \right) \\ &= \left[ \begin{array}{cc} 1 & \cdots & 0 \\ \vdots & \ddots & \vdots \\ 0 & \cdots & 1 \end{array} \right] \otimes \left( \left[ \begin{array}{c} 1 \\ \vdots \\ 1 \end{array} \right] \frac{1}{T} \left[ \begin{array}{ccc} 1 & \cdots & 1 \end{array} \right] \right) \\ &= \left[ \begin{array}{cc} 1 & \cdots & 0 \\ \vdots & \ddots & \vdots \\ 0 & \cdots & 1 \end{array} \right] \otimes \left( \frac{1}{T} \left[ \begin{array}{c} 1 & \cdots & 1 \\ \vdots & \ddots & \vdots \\ 1 & \cdots & 1 \end{array} \right] \right) \\ &= \left[ \begin{array}{cc} 1 & \cdots & 0 \\ \vdots & \ddots & \vdots \\ 0 & \cdots & 1 \end{array} \right]_{N \times N} \otimes \left( \begin{array}{ccc} 1/T & \cdots & 1/T \\ \vdots & \ddots & \vdots\\ 1/T & \cdots & 1/T \end{array} \right)_{T \times T} \\ &= \left[ \begin{array}{ccc} 1 \left( \begin{array}{ccc} 1/T & \cdots & 1/T \\ \vdots & \ddots & \vdots\\ 1/T & \cdots & 1/T \end{array} \right) & \cdots & 0 \left( \begin{array}{ccc} 1/T & \cdots & 1/T \\ \vdots & \ddots & \vdots\\ 1/T & \cdots & 1/T \end{array} \right) \\ \vdots & \ddots & \vdots \\ 0 \left( \begin{array}{ccc} 1/T & \cdots & 1/T \\ \vdots & \ddots & \vdots\\ 1/T & \cdots & 1/T \end{array} \right) & \cdots & 1 \left( \begin{array}{ccc} 1/T & \cdots & 1/T \\ \vdots & \ddots & \vdots\\ 1/T & \cdots & 1/T \end{array} \right) \end{array} \right] \\ &= \left[ \begin{array}{rrr|r|rrr} 1/T & \cdots & 1/T & \cdots & 0 & \cdots & 0 \\ \vdots & \ddots & \vdots & \cdots & \vdots & \ddots & \vdots \\ 1/T & \cdots & 1/T & \cdots & 0 & \cdots & 0 \\\hline \vdots & \vdots & \vdots & \ddots & \vdots & \vdots & \vdots \\\hline 0 & \cdots & 0 & \cdots & 1/T & \cdots & 1/T \\ \vdots & \ddots & \vdots & \cdots & \vdots & \ddots & \vdots \\ 0 & \cdots & 0 & \cdots & 1/T & \cdots & 1/T \end{array} \right]_{NT \times NT}, \end{align}where $\otimes$ is the Kronecker product. After multiplying by $T \sigma^2_u$, every $1/T$ entry becomes $\sigma^2_u$:

$$ T \sigma^2_u \boldsymbol{B} = \left[ \begin{array}{rrr|r|rrr} \sigma^2_u & \cdots & \sigma^2_u & \cdots & 0 & \cdots & 0 \\ \vdots & \ddots & \vdots & \cdots & \vdots & \ddots & \vdots \\ \sigma^2_u & \cdots & \sigma^2_u & \cdots & 0 & \cdots & 0 \\\hline \vdots & \vdots & \vdots & \ddots & \vdots & \vdots & \vdots \\\hline 0 & \cdots & 0 & \cdots & \sigma^2_u & \cdots & \sigma^2_u \\ \vdots & \ddots & \vdots & \cdots & \vdots & \ddots & \vdots \\ 0 & \cdots & 0 & \cdots & \sigma^2_u & \cdots & \sigma^2_u \end{array} \right]_{NT \times NT}, $$Adding the two terms in (4), we obtain the error variance-covariance matrix:

\begin{align} \boldsymbol{\Sigma} &= \sigma^2_v \boldsymbol{I}_{NT} + T \sigma^2_u \boldsymbol{B} \\ &= \left[ \begin{array}{cccc} \sigma^2_v & 0 & \cdots & 0 \\ 0 & \sigma^2_v & \cdots & 0 \\ \vdots & \vdots & \ddots & \vdots \\ 0 & 0 & \cdots & \sigma^2_v \end{array} \right] + \left[ \begin{array}{ccc|c|ccc} \sigma^2_u & \cdots & \sigma^2_u & \cdots & 0 & \cdots & 0 \\ \vdots & \ddots & \vdots & \cdots & \vdots & \ddots & \vdots \\ \sigma^2_u & \cdots & \sigma^2_u & \cdots & 0 & \cdots & 0 \\\hline \vdots & \vdots & \vdots & \ddots & \vdots & \vdots & \vdots \\\hline 0 & \cdots & 0 & \cdots & \sigma^2_u & \cdots & \sigma^2_u \\ \vdots & \ddots & \vdots & \cdots & \vdots & \ddots & \vdots \\ 0 & \cdots & 0 & \cdots & \sigma^2_u & \cdots & \sigma^2_u \end{array} \right] \\ &= \left[ \begin{array}{ccc|c|ccc} \sigma^2_u + \sigma^2_v & \cdots & \sigma^2_u & \cdots & 0 & \cdots & 0 \\ \vdots & \ddots & \vdots & \cdots & \vdots & \ddots & \vdots \\ \sigma^2_u & \cdots & \sigma^2_u + \sigma^2_v & \cdots & 0 & \cdots & 0 \\\hline \vdots & \vdots & \vdots & \ddots & \vdots & \vdots & \vdots \\\hline 0 & \cdots & 0 & \cdots & \sigma^2_u + \sigma^2_v & \cdots & \sigma^2_u \\ \vdots & \ddots & \vdots & \cdots & \vdots & \ddots & \vdots \\ 0 & \cdots & 0 & \cdots & \sigma^2_u & \cdots & \sigma^2_u + \sigma^2_v \end{array} \right] \end{align}Example

Consider the case $N = 2$ and $T = 3$. Then we obtain the following error variance-covariance matrix:

$$\boldsymbol{\Sigma} = \left[ \begin{array}{ccc|ccc} \sigma^2_u + \sigma^2_v & \sigma^2_u & \sigma^2_u & 0 & 0 & 0 \\ \sigma^2_u & \sigma^2_u + \sigma^2_v & \sigma^2_u & 0 & 0 & 0 \\ \sigma^2_u & \sigma^2_u & \sigma^2_u + \sigma^2_v & 0 & 0 & 0 \\\hline 0 & 0 & 0 & \sigma^2_u + \sigma^2_v & \sigma^2_u & \sigma^2_u \\ 0 & 0 & 0 & \sigma^2_u & \sigma^2_u + \sigma^2_v & \sigma^2_u \\ 0 & 0 & 0 & \sigma^2_u & \sigma^2_u & \sigma^2_u + \sigma^2_v \end{array} \right]$$Assuming $\sigma^2_u = 2$ and $\sigma^2_v = 3$, it follows that

$$\boldsymbol{\Sigma} = \left[ \begin{array}{ccc|ccc} 5 & 2 & 2 & 0 & 0 & 0 \\ 2 & 5 & 2 & 0 & 0 & 0 \\ 2 & 2 & 5 & 0 & 0 & 0 \\\hline 0 & 0 & 0 & 5 & 2 & 2 \\ 0 & 0 & 0 & 2 & 5 & 2 \\ 0 & 0 & 0 & 2 & 2 & 5 \end{array} \right]$$To compute this in R, define:

N = 2 # number of individuals

T = 3 # number of periods

sig2u = 2 # variance of the individual error component

sig2v = 3 # variance of the idiosyncratic error component

The first term of $\boldsymbol{\Sigma}$ is

I_NT = diag(N*T) # identity matrix of size NT

I_NT

## [,1] [,2] [,3] [,4] [,5] [,6]

## [1,] 1 0 0 0 0 0

## [2,] 0 1 0 0 0 0

## [3,] 0 0 1 0 0 0

## [4,] 0 0 0 1 0 0

## [5,] 0 0 0 0 1 0

## [6,] 0 0 0 0 0 1

termo1 = sig2v * I_NT

termo1

## [,1] [,2] [,3] [,4] [,5] [,6]

## [1,] 3 0 0 0 0 0

## [2,] 0 3 0 0 0 0

## [3,] 0 0 3 0 0 0

## [4,] 0 0 0 3 0 0

## [5,] 0 0 0 0 3 0

## [6,] 0 0 0 0 0 3

For the second term of $\boldsymbol{\Sigma}$, we first create the identity matrix and the vector of ones:

iota_T = matrix(1, T, 1) # column vector of 1s of length T

iota_T

## [,1]

## [1,] 1

## [2,] 1

## [3,] 1

I_N = diag(N) # identity matrix of size N

I_N

## [,1] [,2]

## [1,] 1 0

## [2,] 0 1

We now compute $\boldsymbol{\iota}_T (\boldsymbol{\iota}'_T \boldsymbol{\iota}_T)^{-1} \boldsymbol{\iota}'_T$

# To obtain a T x T matrix filled with 1/T, where T = 3, we proceed as follows:

t(iota_T) %*% iota_T # inner product of iotas equals T

## [,1]

## [1,] 3

solve(t(iota_T) %*% iota_T) # taking the inverse gives 1/T

## [,1]

## [1,] 0.3333333

iota_T %*% solve(t(iota_T) %*% iota_T) %*% t(iota_T) # pre- and post-multiplying by the iota vector

## [,1] [,2] [,3]

## [1,] 0.3333333 0.3333333 0.3333333

## [2,] 0.3333333 0.3333333 0.3333333

## [3,] 0.3333333 0.3333333 0.3333333

Now we compute

$\boldsymbol{B}\ =\ I_N \otimes \boldsymbol{\iota}_T (\boldsymbol{\iota}'_T \boldsymbol{\iota}_T)^{-1} \boldsymbol{\iota}'_T$ using the Kronecker product operator %x%:

B = I_N %x% (iota_T %*% solve(t(iota_T) %*% iota_T) %*% t(iota_T))

round(B, 3)

## [,1] [,2] [,3] [,4] [,5] [,6]

## [1,] 0.333 0.333 0.333 0.000 0.000 0.000

## [2,] 0.333 0.333 0.333 0.000 0.000 0.000

## [3,] 0.333 0.333 0.333 0.000 0.000 0.000

## [4,] 0.000 0.000 0.000 0.333 0.333 0.333

## [5,] 0.000 0.000 0.000 0.333 0.333 0.333

## [6,] 0.000 0.000 0.000 0.333 0.333 0.333

Multiplying $\boldsymbol{B}$ by $T \sigma^2_u$, we obtain the second term of $\boldsymbol{\Sigma}$:

termo2 = T * sig2u * B

termo2

## [,1] [,2] [,3] [,4] [,5] [,6]

## [1,] 2 2 2 0 0 0

## [2,] 2 2 2 0 0 0

## [3,] 2 2 2 0 0 0

## [4,] 0 0 0 2 2 2

## [5,] 0 0 0 2 2 2

## [6,] 0 0 0 2 2 2

Therefore, the error variance-covariance matrix is given by:

Sigma = termo1 + termo2

Sigma

## [,1] [,2] [,3] [,4] [,5] [,6]

## [1,] 5 2 2 0 0 0

## [2,] 2 5 2 0 0 0

## [3,] 2 2 5 0 0 0

## [4,] 0 0 0 5 2 2

## [5,] 0 0 0 2 5 2

## [6,] 0 0 0 2 2 5

Estimating the Error Components

Note that $\sigma^2_v$ and $\sigma^2_u$ are unknown, so $\boldsymbol{\Sigma}$ is also unknown.

First, consider the within transformation matrix, given by

- Note that we can rewrite \begin{align} \hat{\boldsymbol{\Sigma}} &= \hat{\sigma}^2_v \boldsymbol{I}_{NT} + T \hat{\sigma}^2_u \boldsymbol{B}\\ &= \hat{\sigma}^2_v (\boldsymbol{W} + \boldsymbol{B}) + T \hat{\sigma}^2_u \boldsymbol{B}\\ &= \hat{\sigma}^2_v \boldsymbol{W} + \hat{\sigma}^2_v \boldsymbol{B} + T \hat{\sigma}^2_u \boldsymbol{B}\\ &= \hat{\sigma}^2_v \boldsymbol{W} + (\hat{\sigma}^2_v + T \hat{\sigma}^2_u) \boldsymbol{B} \end{align} where $\boldsymbol{W} = \boldsymbol{I}_{NT} - \boldsymbol{B} \iff \boldsymbol{I}_{NT} = \boldsymbol{W} + \boldsymbol{B} $

- This can be generalized as: $$ \hat{\boldsymbol{\Sigma}}^p = (\hat{\sigma}^2_v)^p \boldsymbol{W} + (\hat{\sigma}^2_v + T \hat{\sigma}^2_u)^p \boldsymbol{B}, \tag{2.29} $$ where $p$ is a scalar.

- This formula will be useful later when computing $ \hat{\boldsymbol{\Sigma}}^{-1}$ and $ \hat{\boldsymbol{\Sigma}}^{-0.5}$.

- If $\boldsymbol{\varepsilon}$ were observed, we could estimate the two variances as follows:

Because $\boldsymbol{\varepsilon}$ is unobserved, we instead use residuals from consistent estimators.

Wallace and Hussain (1969): use OLS residuals.

Amemiya (1971): uses within residuals. $$\hat{\sigma}^2_v = \frac{\hat{\boldsymbol{\varepsilon}}'_{\scriptscriptstyle{W}} \boldsymbol{W} \hat{\boldsymbol{\varepsilon}}_{\scriptscriptstyle{W}}}{N(T-1)} \quad \text{and} \quad \hat{\sigma}^2_u = \frac{1}{T} \left( \frac{\hat{\boldsymbol{\varepsilon}}'_{\scriptscriptstyle{W}} \boldsymbol{B} \hat{\boldsymbol{\varepsilon}}_{\scriptscriptstyle{W}}}{N} - \hat{\sigma}^2_v \right)$$

Hausman and Taylor (1981): adjust Amemiya’s method by regressing $\hat{\boldsymbol{\varepsilon}}_{\scriptscriptstyle{W}}$ on all time-invariant regressors in the model and then using the resulting residuals, $\hat{\boldsymbol{\varepsilon}}_{\scriptscriptstyle{HT}}$.

Swamy and Arora (1972): use both between and within residuals to compute: $$\hat{\sigma}^2_v = \frac{\hat{\boldsymbol{\varepsilon}}'_{\scriptscriptstyle{W}} \boldsymbol{W} \hat{\boldsymbol{\varepsilon}}_{\scriptscriptstyle{W}}}{N(T-1) - K} \quad \text{and} \quad \hat{\sigma}^2_u = \frac{1}{T} \left( \frac{\hat{\boldsymbol{\varepsilon}}'_{\scriptscriptstyle{B}} \boldsymbol{B} \hat{\boldsymbol{\varepsilon}}_{\scriptscriptstyle{B}}}{N - K - 1} - \hat{\sigma}^2_v \right)$$

Nerlove (1971): computes $\sigma^2_u$ empirically from the fixed effects of the within model.

After obtaining $\hat{\sigma}^2_u$ and $\hat{\sigma}^2_v$, we only need to compute $\hat{\boldsymbol{\Sigma}}$:

GLS Estimator

- Section 2.1.1 of “Panel Data Econometrics with R” (Croissant & Millo, 2018)

- Pooled GLS uses the same point estimates as OLS, but inference is based on $\boldsymbol{\Sigma} \neq \sigma^2 \boldsymbol{I}$, allowing correlation among observations from the same individual $i$.

The model to be estimated is $$ \boldsymbol{y} = \boldsymbol{X\beta} + \boldsymbol{\varepsilon} $$

The GLS estimator $\hat{\boldsymbol{\beta}}$ (which coincides with OLS in point estimation) is given by $$ \hat{\boldsymbol{\beta}}_{\scriptscriptstyle{GLS}} = (\boldsymbol{X}'\boldsymbol{X})^{-1} \boldsymbol{X}' \boldsymbol{y} $$

Note that the OLS estimator variance-covariance matrix, under $ \boldsymbol{\Sigma} = \sigma^2 \boldsymbol{I} $, simplifies to:

- The GLS estimator variance-covariance matrix, which allows correlation among observations from the same individual, is given by $$ V(\hat{\boldsymbol{\beta}}_{\scriptscriptstyle{GLS}}) = (\boldsymbol{X}'\boldsymbol{X})^{-1} \boldsymbol{X}' \hat{\boldsymbol{\Sigma}} \boldsymbol{X} (\boldsymbol{X}'\boldsymbol{X})^{-1} $$

Estimation via plm()

To illustrate the estimators discussed above, we use the TobinQ dataset from the pder package, which contains data for 188 firms over 35 years (6,580 observations).

data("TobinQ", package = "pder")

str(TobinQ)

## 'data.frame': 6580 obs. of 15 variables:

## $ cusip : int 2824 2824 2824 2824 2824 2824 2824 2824 2824 2824 ...

## $ year : num 1951 1952 1953 1954 1955 ...

## $ isic : int 2835 2835 2835 2835 2835 2835 2835 2835 2835 2835 ...

## $ ikb : num 0.2295 0.0403 0.0404 0.0518 0.055 ...

## $ ikn : num 0.2049 0.1997 0.1103 0.1258 0.0682 ...

## $ qb : num 5.61 6.01 4.19 4 4.47 ...

## $ qn : num 10.91 12.23 7.41 6.78 7.37 ...

## $ kstock: num 27.3 30.5 31.7 32.6 32.3 ...

## $ ikicb : num NA 0.193156 0.002919 -0.007656 -0.000145 ...

## $ ikicn : num 0.012 0.02448 0.09763 -0.00635 0.06144 ...

## $ omphi : num 0.1841 0.0968 0.0745 0.0727 0.0558 ...

## $ qicb : num NA 0.245 1.9 0.421 -0.166 ...

## $ qicn : num NA 0.066 4.685 0.947 -0.135 ...

## $ sb : num NA 1.98 1.55 1.65 1.64 ...

## $ sn : num NA 4.02 3.3 3.09 2.94 ...

cusip: Firm identifieryear: Yearikn: Investment divided by capitalqn: Tobin’s Q (the ratio between firm value and the replacement cost of physical capital). If $Q > 1$, the return on investment exceeds its cost.

We want to estimate the following model: $$ \text{ikn} = \beta_0 + \text{qn} \beta_1 + \varepsilon $$

We use the plm() function from the package of the same name to estimate linear panel-data models. Its main arguments are:

formula: model equationdata: the dataset, either as adata.frame(in which caseindexmust be supplied) or as apdata.frame(the package’s indexed panel-data format)model: estimator to compute:pooling(GLS),between,within(fixed effects), orrandom(random effects / FGLS)index: vector with the names of the individual and time identifiers

Note that pooled estimation via plm() still uses

$\boldsymbol{\Sigma} = \sigma^2 \boldsymbol{I}$, so it incorrectly ignores within-individual error correlation:

library(plm)

# Converting to `pdata.frame` format with individual and time identifiers

pTobinQ = pdata.frame(TobinQ, index=c("cusip", "year"))

# OLS estimation

Q.pooling = plm(ikn ~ qn, pTobinQ, model = "pooling")

Q.ols = lm(ikn ~ qn, TobinQ)

# Comparing both outputs

stargazer::stargazer(Q.pooling, Q.ols, type="text", omit.stat="f")

##

## ================================================

## Dependent variable:

## ----------------------------

## ikn

## panel OLS

## linear

## (1) (2)

## ------------------------------------------------

## qn 0.004*** 0.004***

## (0.0002) (0.0002)

##

## Constant 0.158*** 0.158***

## (0.001) (0.001)

##

## ------------------------------------------------

## Observations 6,580 6,580

## R2 0.111 0.111

## Adjusted R2 0.111 0.111

## Residual Std. Error 0.086 (df = 6578)

## ================================================

## Note: *p<0.1; **p<0.05; ***p<0.01

- We need to conduct inference using an appropriate error variance-covariance matrix. For that, we use the argument

vcov=vcovBKinsidesummary():

# GLS estimation with an error covariance matrix allowing within-individual correlation

summary(Q.pooling, vcov=vcovBK)$coef

## Estimate Std. Error t-value Pr(>|t|)

## (Intercept) 0.15799969 0.0034686968 45.55016 0.000000e+00

## qn 0.00439197 0.0003774606 11.63557 5.458161e-31

Analytical Estimation

The analytical GLS derivation is the same as OLS, but adapted to the panel-data setting. The main differences are the degrees of freedom, $NT - K - 1$, and the panel-specific structure of the error variance-covariance matrix $\boldsymbol{\Sigma}$.

a) Criando vetores/matrizes e definindo N, T e K

# Creating the y vector

y = as.matrix(TobinQ[,"ikn"]) # converting the data frame column into a matrix

head(y)

## [,1]

## [1,] 0.20488372

## [2,] 0.19974634

## [3,] 0.11033265

## [4,] 0.12583384

## [5,] 0.06819211

## [6,] 0.09540332

# Creating the covariate matrix X with a first column of ones

X = cbind( 1, TobinQ[, "qn"] ) # adding a column of ones to the covariates

X = as.matrix(X) # converting to a matrix

head(X)

## [,1] [,2]

## [1,] 1 10.910007

## [2,] 1 12.234629

## [3,] 1 7.410110

## [4,] 1 6.779812

## [5,] 1 7.372266

## [6,] 1 6.097779

# Retrieving N, T, and K

N = length( unique(TobinQ$cusip) )

N # number of individuals

## [1] 188

T = length( unique(TobinQ$year) )

T # number of periods

## [1] 35

K = ncol(X) - 1

K # number of covariates

## [1] 1

b) GLS estimates $\hat{\boldsymbol{\beta}}_{\scriptscriptstyle{GLS}}$

$$ \hat{\boldsymbol{\beta}}_{\scriptscriptstyle{GLS}} = (\boldsymbol{X}'\boldsymbol{X})^{-1} \boldsymbol{X}' \boldsymbol{y} $$bhat = solve( t(X) %*% X ) %*% t(X) %*% y

bhat

## [,1]

## [1,] 0.15799969

## [2,] 0.00439197

c) Fitted values $\hat{\boldsymbol{y}}$

$$ \hat{\boldsymbol{y}} = \boldsymbol{X} \hat{\boldsymbol{\beta}} $$yhat = X %*% bhat

head(yhat)

## [,1]

## [1,] 0.2059161

## [2,] 0.2117338

## [3,] 0.1905447

## [4,] 0.1877764

## [5,] 0.1903785

## [6,] 0.1847810

d) Residuals $\hat{\boldsymbol{\varepsilon}}$

$$ \hat{\boldsymbol{\varepsilon}} = \boldsymbol{y} - \hat{\boldsymbol{y}} $$ehat = y - yhat

head(ehat)

## [,1]

## [1,] -0.001032395

## [2,] -0.011987475

## [3,] -0.080212022

## [4,] -0.061942582

## [5,] -0.122186352

## [6,] -0.089377633

e) Error-term variances

\begin{align} \hat{\sigma}^2_v &= \frac{\hat{\boldsymbol{\varepsilon}}'_{\scriptscriptstyle{OLS}} \boldsymbol{W} \hat{\boldsymbol{\varepsilon}}_{\scriptscriptstyle{OLS}}}{N(T-1)} \\ \hat{\sigma}^2_u &=\frac{1}{T} \left( \frac{\hat{\boldsymbol{\varepsilon}}'_{\scriptscriptstyle{OLS}} \boldsymbol{B} \hat{\boldsymbol{\varepsilon}}_{\scriptscriptstyle{OLS}}}{N} - \hat{\sigma}^2_v \right) \end{align}Because

$\hat{\sigma}^2_u$ and

$\hat{\sigma}^2_v$ are scalars, it is convenient to convert the resulting “1x1 matrices” into numbers with as.numeric():

# Creating the between and within matrices

iota_T = matrix(1, T, 1) # column vector of 1s of length T

I_N = diag(N) # identity matrix of size N

I_NT = diag(N*T) # identity matrix of size NT

B = I_N %x% (iota_T %*% solve(t(iota_T) %*% iota_T) %*% t(iota_T))

W = I_NT - B

# Computing the error-component variances (Wallace and Hussain)

sig2v = as.numeric( (t(ehat) %*% W %*% ehat) / (N*(T-1)) )

sig2u = as.numeric( (1/T) * ( (t(ehat) %*% B %*% ehat)/N - sig2v ) )

f) Error Variance-Covariance Matrix $$\hat{\boldsymbol{\Sigma}} = \hat{\sigma}^2_v \boldsymbol{W} + (\hat{\sigma}^2_v + T \hat{\sigma}^2_u) \boldsymbol{B}$$

# Computing the error variance-covariance matrix

Sigma = sig2v * W + (sig2v + T*sig2u) * B

g) Estimator Variance-Covariance Matrix

$$ \widehat{\text{Var}}(\hat{\boldsymbol{\beta}}) = (\boldsymbol{X}'\boldsymbol{X})^{-1} \boldsymbol{X}' \hat{\boldsymbol{\Sigma}} \boldsymbol{X} (\boldsymbol{X}'\boldsymbol{X})^{-1} $$# Computing the variance-covariance matrix of the estimators

bread = solve( t(X) %*% X )

meat = t(X) %*% Sigma %*% X

Vbhat = bread %*% meat %*% bread # sandwich

Vbhat

## [,1] [,2]

## [1,] 1.220549e-05 -2.839164e-07

## [2,] -2.839164e-07 1.133241e-07

h) Standard errors of the estimator $\text{se}(\hat{\boldsymbol{\beta}})$

It is the square root of the main diagonal of the estimator variance-covariance matrix.

se_bhat = sqrt( diag(Vbhat) )

se_bhat

## [1] 0.0034936352 0.0003366365

i) t statistic

$$ t_{\hat{\beta}_k} = \frac{\hat{\beta}_k}{\text{se}(\hat{\beta}_k)} \tag{4.6} $$# Computing the t statistic

t_bhat = bhat / se_bhat

t_bhat

## [,1]

## [1,] 45.22501

## [2,] 13.04663

j) p-value

$$ p_{\hat{\beta}_k} = 2.\Phi_{t_{(NT-K-1)}}(-|t_{\hat{\beta}_k}|), \tag{4.7} $$# p-value

p_bhat = 2 * pt(-abs(t_bhat), N*T-K-1)

p_bhat

## [,1]

## [1,] 0.000000e+00

## [2,] 1.986019e-38

k) Summary table

data.frame(bhat, se_bhat, t_bhat, p_bhat) # correct GLS result

## bhat se_bhat t_bhat p_bhat

## 1 0.15799969 0.0034936352 45.22501 0.000000e+00

## 2 0.00439197 0.0003366365 13.04663 1.986019e-38

summary(Q.pooling)$coef # OLS result via `plm()` or `lm()`

## Estimate Std. Error t-value Pr(>|t|)

## (Intercept) 0.15799969 0.001124399 140.51928 0.000000e+00

## qn 0.00439197 0.000152940 28.71694 5.789663e-171

summary(Q.pooling, vcov=vcovBK)$coef # with the adjusted error covariance matrix

## Estimate Std. Error t-value Pr(>|t|)

## (Intercept) 0.15799969 0.0034686968 45.55016 0.000000e+00

## qn 0.00439197 0.0003774606 11.63557 5.458161e-31

FGLS Estimator

Section 2.3 of “Panel Data Econometrics with R” (Croissant & Millo, 2018)

Also known as the random-effects estimator, because it treats individual effects as random: $E(\boldsymbol{u}) = 0$

Errors are linked through the error variance-covariance matrix $\boldsymbol{\Sigma}$.

The FGLS estimator is given by $$ {\boldsymbol{\beta}}_{\scriptscriptstyle{FGLS}} = (\boldsymbol{X}' {\boldsymbol{\Sigma}}^{-1} \boldsymbol{X})^{-1} (\boldsymbol{X}' {\boldsymbol{\Sigma}}^{-1} \boldsymbol{y}) \tag{2.27} $$

The variance-covariance matrix of the estimator is given by $$ V(\hat{\boldsymbol{\beta}}_{\scriptscriptstyle{FGLS}}) = (\boldsymbol{X}' \boldsymbol{\Sigma}^{-1} \boldsymbol{X})^{-1} \tag{2.28} $$

The matrix $\boldsymbol{\Sigma}$ depends on only two parameters, $\sigma^2_u$ and $\sigma^2_v$: $$ \boldsymbol{\Sigma}^p = ({\sigma}^2_v)^p \boldsymbol{W} + ({\sigma}^2_v + T {\sigma}^2_u)^p \boldsymbol{B} \tag{2.29} $$

- Because $\boldsymbol{\Sigma}$ is unknown, we can estimate $\hat{\boldsymbol{\Sigma}}$ by estimating the error components using, for example, Wallace and Hussain (1969):

Estimation via plm()

- We use

plm()again, this time settingmodel = "random"so the model is estimated by FGLS. - In

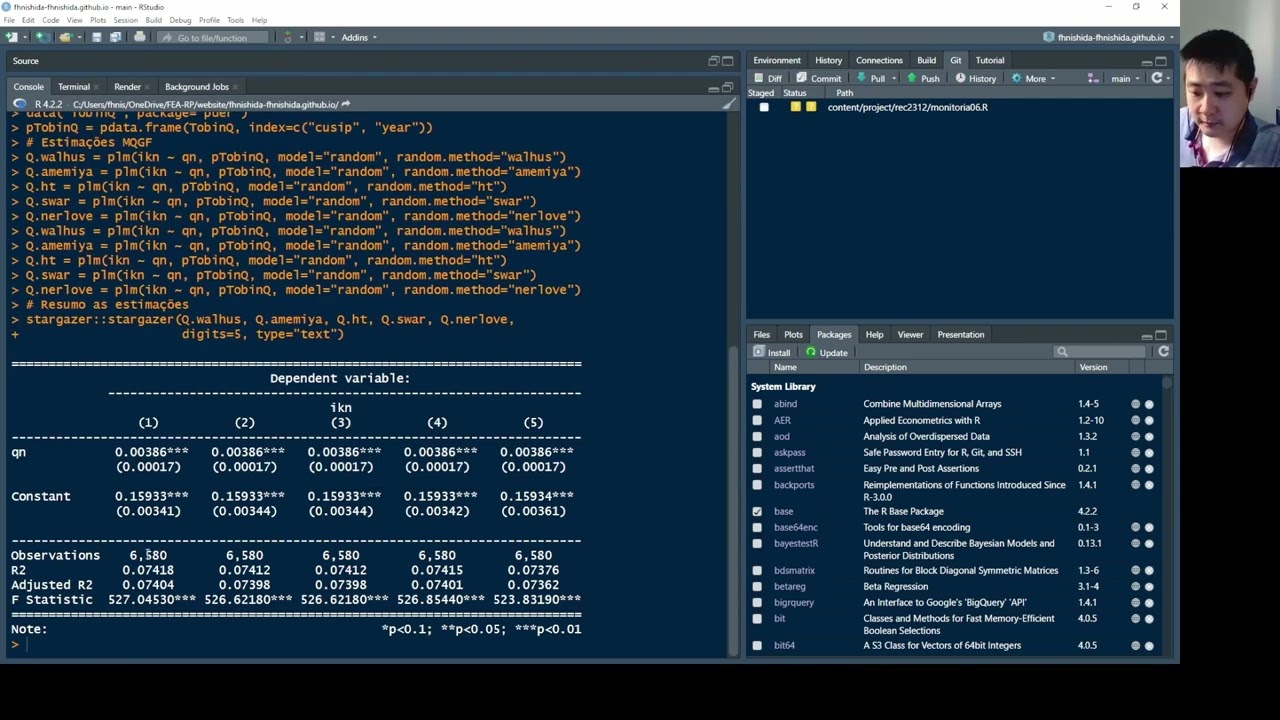

random.method, we can choose the procedure used to estimate the error-component parameters:"walhus"for Wallace and Hussain (1969)"amemiya"for Amemiya (1971)"ht"for Hausman and Taylor (1981)"swar"for Swamy and Arora (1972) [default]"nerlove"for Nerlove (1971)

library(plm)

data("TobinQ", package = "pder")

pTobinQ = pdata.frame(TobinQ, index=c("cusip", "year"))

# FGLS estimations

Q.walhus = plm(ikn ~ qn, pTobinQ, model = "random", random.method = "walhus")

Q.amemiya = plm(ikn ~ qn, pTobinQ, model = "random", random.method = "amemiya")

Q.ht = plm(ikn ~ qn, pTobinQ, model = "random", random.method = "ht")

Q.swar = plm(ikn ~ qn, pTobinQ, model = "random", random.method = "swar")

Q.nerlove = plm(ikn ~ qn, pTobinQ, model = "random", random.method = "nerlove")

# Summarizing the five estimations in a single table

stargazer::stargazer(Q.walhus, Q.amemiya, Q.ht, Q.swar, Q.nerlove,

digits=5, type="text", omit.stat="f")

##

## ===================================================================

## Dependent variable:

## ------------------------------------------------------

## ikn

## (1) (2) (3) (4) (5)

## -------------------------------------------------------------------

## qn 0.00386*** 0.00386*** 0.00386*** 0.00386*** 0.00386***

## (0.00017) (0.00017) (0.00017) (0.00017) (0.00017)

##

## Constant 0.15933*** 0.15933*** 0.15933*** 0.15933*** 0.15934***

## (0.00341) (0.00344) (0.00344) (0.00342) (0.00361)

##

## -------------------------------------------------------------------

## Observations 6,580 6,580 6,580 6,580 6,580

## R2 0.07418 0.07412 0.07412 0.07415 0.07376

## Adjusted R2 0.07404 0.07398 0.07398 0.07401 0.07362

## ===================================================================

## Note: *p<0.1; **p<0.05; ***p<0.01

In this particular case, the results are virtually identical.

Analytical Estimation

- Here, we derive the analytical FGLS estimator using the Wallace and Hussain (1969) method.

- First, we compute $\hat{\boldsymbol{\beta}}_{\scriptscriptstyle{OLS}}$ and $\hat{\boldsymbol{\varepsilon}}_{\scriptscriptstyle{OLS}}$ in order to estimate $\hat{\sigma}^2_{u}$, $\hat{\sigma}^2_{v}$, and $\hat{\boldsymbol{\Sigma}}$.

- Then we estimate $\hat{\boldsymbol{\beta}}_{\scriptscriptstyle{FGLS}}$ and its variance matrix $V_{\hat{\boldsymbol{\beta}}_{\tiny{FGLS}}}$.

a) Criando vetores/matrizes e definindo N, T e K

# Creating the y vector

y = as.matrix(TobinQ[,"ikn"]) # converting the data frame column into a matrix

# Creating the covariate matrix X with a first column of ones

X = as.matrix( cbind(1, TobinQ[, "qn"]) ) # adding a column of ones to the covariates

# Retrieving N, T, and K

N = length( unique(TobinQ$cusip) )

T = length( unique(TobinQ$year) )

K = ncol(X) - 1

b) OLS estimates $\hat{\boldsymbol{\beta}}_{\scriptscriptstyle{OLS}}$

$$ \hat{\boldsymbol{\beta}}_{\scriptscriptstyle{OLS}} = (\boldsymbol{X}'\boldsymbol{X})^{-1} \boldsymbol{X}' \boldsymbol{y} $$bhat_OLS = solve( t(X) %*% X ) %*% t(X) %*% y

c) OLS fitted values $\hat{\boldsymbol{y}}_{\scriptscriptstyle{OLS}}$

$$ \hat{\boldsymbol{y}}_{\scriptscriptstyle{OLS}} = \boldsymbol{X} \hat{\boldsymbol{\beta}}_{\scriptscriptstyle{OLS}} $$yhat_OLS = X %*% bhat_OLS

d) OLS residuals $\hat{\boldsymbol{\varepsilon}}_{\scriptscriptstyle{OLS}}$

$$ \hat{\boldsymbol{\varepsilon}}_{\scriptscriptstyle{OLS}} = \boldsymbol{y} - \hat{\boldsymbol{y}}_{\scriptscriptstyle{OLS}} $$ehat_OLS = y - yhat_OLS

e) Error-term variances

\begin{align} \hat{\sigma}^2_v &= \frac{\hat{\boldsymbol{\varepsilon}}'_{\scriptscriptstyle{OLS}} \boldsymbol{W} \hat{\boldsymbol{\varepsilon}}_{\scriptscriptstyle{OLS}}}{N(T-1)} \\ \hat{\sigma}^2_u &=\frac{1}{T} \left( \frac{\hat{\boldsymbol{\varepsilon}}'_{\scriptscriptstyle{OLS}} \boldsymbol{B} \hat{\boldsymbol{\varepsilon}}_{\scriptscriptstyle{OLS}}}{N} - \hat{\sigma}^2_v \right) \end{align}Because

$\hat{\sigma}^2_u$ and

$\hat{\sigma}^2_v$ are scalars, it is convenient to convert the resulting “1x1 matrices” into numbers with as.numeric():

# Creating the between and within matrices

iota_T = matrix(1, T, 1) # column vector of 1s of length T

I_N = diag(N) # identity matrix of size N

I_NT = diag(N*T) # identity matrix of size NT

B = I_N %x% (iota_T %*% solve(t(iota_T) %*% iota_T) %*% t(iota_T))

W = I_NT - B

# Computing the error-component variances (Wallace and Hussain)

sig2v = as.numeric( (t(ehat_OLS) %*% W %*% ehat_OLS) / (N*(T-1)) )

sig2u = as.numeric( (1/T) * ( (t(ehat_OLS) %*% B %*% ehat_OLS)/N - sig2v ) )

f) Error Variance-Covariance Matrix

$$ \hat{\boldsymbol{\Sigma}}^p = (\hat{\sigma}^2_v)^p \boldsymbol{W} + (\hat{\sigma}^2_v + T \hat{\sigma}^2_u)^p \boldsymbol{B} $$# Computing the error variance-covariance matrix

Sigma = sig2v * W + (sig2v + T*sig2u) * B

# Matrix inverse

Sigma_1 = sig2v^(-1) * W + (sig2v + T*sig2u)^(-1) * B

*Note that using solve() on the Sigma matrix is computationally slower than using the formula

g) FGLS estimates $\hat{\boldsymbol{\beta}}_{\scriptscriptstyle{FGLS}}$

$$ \hat{\boldsymbol{\beta}}_{\scriptscriptstyle{FGLS}} = (\boldsymbol{X}' \boldsymbol{\Sigma}^{-1} \boldsymbol{X})^{-1} \boldsymbol{X}' \boldsymbol{\Sigma}^{-1} \boldsymbol{y} $$bhat_FGLS = solve( t(X) %*% Sigma_1 %*% X ) %*% t(X) %*% Sigma_1 %*% y

bhat_FGLS

## [,1]

## [1,] 0.159325869

## [2,] 0.003862631

h) Estimator Variance-Covariance Matrix

$$ \widehat{\text{Var}}(\hat{\boldsymbol{\beta}}_{\scriptscriptstyle{FGLS}}) = (\boldsymbol{X}' \boldsymbol{\Sigma}^{-1} \boldsymbol{X})^{-1} $$# Computing the variance-covariance matrix of the estimators

Vbhat = solve( t(X) %*% Sigma_1 %*% X )

Vbhat

## [,1] [,2]

## [1,] 1.167208e-05 -7.100808e-08

## [2,] -7.100808e-08 2.834259e-08

i) Standard errors of the estimator $\text{se}(\hat{\boldsymbol{\beta}}_{\scriptscriptstyle{FGLS}})$

It is the square root of the main diagonal of the estimator variance-covariance matrix.

se_bhat = sqrt( diag(Vbhat) )

se_bhat

## [1] 0.0034164422 0.0001683526

j) t statistic

$$ t_{\hat{\beta}_k} = \frac{\hat{\beta}_k}{\text{se}(\hat{\beta}_k)} \tag{4.6} $$# Computing the t statistic

t_bhat = bhat_FGLS / se_bhat

t_bhat

## [,1]

## [1,] 46.63503

## [2,] 22.94370

k) p-value

$$ p_{\hat{\beta}_k} = 2.\Phi_{t_{(NT-K-1)}}(-|t_{\hat{\beta}_k}|), \tag{4.7} $$# p-value

p_bhat = 2 * pt(-abs(t_bhat), N*T-K-1)

p_bhat

## [,1]

## [1,] 0.000000e+00

## [2,] 3.904386e-112

l) Summary table

data.frame(bhat_FGLS, se_bhat, t_bhat, p_bhat) # correct GLS result

## bhat_FGLS se_bhat t_bhat p_bhat

## 1 0.159325869 0.0034164422 46.63503 0.000000e+00

## 2 0.003862631 0.0001683526 22.94370 3.904386e-112

summary(Q.walhus)$coef # FGLS result via `plm()`

## Estimate Std. Error z-value Pr(>|z|)

## (Intercept) 0.159325869 0.0034143937 46.66300 0.000000e+00

## qn 0.003862631 0.0001682516 22.95747 1.240977e-116

Transforming and Estimating by OLS

In addition to the form shown above, we can transform the variables and solve by OLS after premultiplying $\boldsymbol{X}$ and $\boldsymbol{y}$ by $\boldsymbol{\Sigma}^{-0.5}$, defining:

$$\tilde{\boldsymbol{X}} \equiv \boldsymbol{\Sigma}^{-0.5} \boldsymbol{X} \qquad \text{and} \qquad \tilde{\boldsymbol{y}} \equiv \boldsymbol{\Sigma}^{-0.5} \boldsymbol{y}$$f’) Error Variance-Covariance Matrix

$$ \hat{\boldsymbol{\Sigma}}^p = (\hat{\sigma}^2_v)^p \boldsymbol{W} + (\hat{\sigma}^2_v + T \hat{\sigma}^2_u)^p \boldsymbol{B} $$# Error Variance-Covariance Matrix ^ (-0.5)

Sigma_05 = sig2v^(-0.5) * W + (sig2v + T*sig2u)^(-0.5) * B

# Transformed variables

X_til = Sigma_05 %*% X

y_til = Sigma_05 %*% y

g’) FGLS estimates via OLS

\begin{align} \hat{\boldsymbol{\beta}}_{\scriptscriptstyle{FGLS}} &= (\boldsymbol{X}' \boldsymbol{\Sigma}^{-1} \boldsymbol{X})^{-1} \boldsymbol{X}' \boldsymbol{\Sigma}^{-1} \boldsymbol{y} \\ &= (\boldsymbol{X}' \boldsymbol{\Sigma}^{-0.5} \boldsymbol{\Sigma}^{-0.5} \boldsymbol{X})^{-1} \boldsymbol{X}' \boldsymbol{\Sigma}^{-0.5} \boldsymbol{\Sigma}^{-0.5} \boldsymbol{y} \\ &= (\boldsymbol{X}' \boldsymbol{\Sigma}'^{-0.5} \boldsymbol{\Sigma}^{-0.5} \boldsymbol{X})^{-1} \boldsymbol{X}' \boldsymbol{\Sigma}'^{-0.5} \boldsymbol{\Sigma}^{-0.5} \boldsymbol{y} \\ &= ([\boldsymbol{\Sigma}^{-0.5} \boldsymbol{X}]' [\boldsymbol{\Sigma}^{-0.5} \boldsymbol{X}])^{-1} [\boldsymbol{\Sigma}^{-0.5} \boldsymbol{X}]' [\boldsymbol{\Sigma}^{-0.5} \boldsymbol{y}] \\ &\equiv (\tilde{\boldsymbol{X}}' \tilde{\boldsymbol{X}})^{-1} \tilde{\boldsymbol{X}}' \tilde{\boldsymbol{y}}= \tilde{\hat{\boldsymbol{\beta}}}_{\scriptscriptstyle{OLS}} \end{align}Note that $\boldsymbol{\Sigma}'^{-0.5} = \boldsymbol{\Sigma}^{-0.5}$.

bhat_OLS = solve( t(X_til) %*% X_til ) %*% t(X_til) %*% y_til

bhat_OLS

## [,1]

## [1,] 0.159325869

## [2,] 0.003862631

h’) Valores Ajustados e Residuals OLS $$\tilde{\hat{y}} = \tilde{\boldsymbol{X}} \tilde{\hat{\boldsymbol{\beta}}}_{\scriptscriptstyle{OLS}} \qquad \text{and} \qquad \tilde{\hat{\boldsymbol{\varepsilon}}} = \boldsymbol{y} - \tilde{\hat{y}} $$

yhat_OLS = X_til %*% bhat_OLS # Fitted values

ehat_OLS = y_til - yhat_OLS # Residuals

i’) Error-term variance OLS $$\hat{\sigma}^2 = \frac{\tilde{\hat{\boldsymbol{\varepsilon}}}'\tilde{\hat{\boldsymbol{\varepsilon}}}}{NT - K - 1} $$

sig2hat = as.numeric( t(ehat_OLS) %*% ehat_OLS / (N*T - K - 1) )

j’) Error Variance-Covariance Matrix OLS $$ \widehat{\text{Var}}(\hat{\boldsymbol{\beta}}_{\scriptscriptstyle{FGLS}}) = \hat{\sigma}^2 (\tilde{\boldsymbol{X}}' \tilde{\boldsymbol{X}})^{-1} $$

Vbhat_OLS = sig2hat * solve(t(X_til) %*% X_til)

Vbhat_OLS

## [,1] [,2]

## [1,] 1.165808e-05 -7.092295e-08

## [2,] -7.092295e-08 2.830861e-08

k’) Standard errors, t statistics, and p-values

se_bhat_OLS = sqrt( diag(Vbhat_OLS) )

t_bhat_OLS = bhat_OLS / se_bhat_OLS

p_bhat_OLS = 2 * pt(-abs(t_bhat_OLS), N*T-K-1)

l’) Comparativo

# Analytical FGLS via OLS

data.frame(bhat_OLS, se_bhat_OLS, t_bhat_OLS, p_bhat_OLS)

## bhat_OLS se_bhat_OLS t_bhat_OLS p_bhat_OLS

## 1 0.159325869 0.0034143937 46.66300 0.000000e+00

## 2 0.003862631 0.0001682516 22.95747 2.912584e-112

# FGLS via plm

summary(Q.walhus)$coef

## Estimate Std. Error z-value Pr(>|z|)

## (Intercept) 0.159325869 0.0034143937 46.66300 0.000000e+00

## qn 0.003862631 0.0001682516 22.95747 1.240977e-116

Transformation Matrices

- Section 2.1.2 of “Panel Data Econometrics with R” (Croissant & Millo, 2018)

Panel Data Model (2)

- We now distinguish time-invariant explanatory variables from time-varying ones.

- Suppose that among the $K$ explanatory variables, $J$ are time-invariant and $L$ are time-varying:

Model (1) is: \begin{align} y_{it} &= \boldsymbol{x}'_{it} \boldsymbol{\beta} + \varepsilon_{it} \tag{1} \\ &= 1.\beta_0 + x^1_{it} \beta_1 + ... + x^J_{it} \beta_J + x^{J+1}_{it} \beta_{J+1} + ... + x^K_{it} \beta_K + \varepsilon_{it} \end{align} and it can be rewritten as: \begin{align} y_{it} &= \boldsymbol{x}'_{i} \boldsymbol{\Gamma} + \boldsymbol{x}^{*\prime}_{it} \boldsymbol{\delta} + \varepsilon_{it} \tag{2} \\ &= 1.\Gamma_0 + x^1_{i} \Gamma_1 + ... + x^J_{i} \Gamma_J + x^{*1}_{it} \delta_{1} + ... + x^{*L}_{it} \delta_L + \varepsilon_{it} \end{align} where:

- $\boldsymbol{x}'_{it} = [\boldsymbol{x}'_{i}, \boldsymbol{x}^{*\prime}_{it}] $

$\boldsymbol{x}'_{i}$ collects the realizations of the $J$ time-invariant variables, together with the intercept: $$ \boldsymbol{x}'_{i} = \begin{bmatrix} 1 & x^1_i & x^2_i & \cdots & x^J_i \end{bmatrix} $$

$\boldsymbol{x}^{*\prime}_{it}$ collects the realizations of the $L$ time-varying variables: $$ \boldsymbol{x}^{*\prime}_{it} = \begin{bmatrix} x^{*1}_{it} & x^{*2}_{it} & \cdots & x^{*L}_{it} \end{bmatrix} $$

$\varepsilon_{it} = u_i + v_{it}$.

$\boldsymbol{\Gamma}$ and $\boldsymbol{\delta}$ are the parameter vectors for time-invariant and time-varying variables, respectively, so that \begin{align} \boldsymbol{\beta}\quad\ &\equiv \begin{bmatrix} \ \boldsymbol{\Gamma}\ \\ \ \boldsymbol{\delta}\ \end{bmatrix} \\ \begin{bmatrix} \beta_0 \\ \beta_1 \\ \beta_2 \\ \vdots \\ \beta_J \\\hline \beta_{J+1} \\ \beta_{J+2} \\ \vdots \\ \beta_{K} \end{bmatrix} &\equiv \begin{bmatrix} \Gamma_0 \\ \Gamma_1 \\ \Gamma_2 \\ \vdots \\ \Gamma_J \\\hline \delta_1 \\ \delta_2 \\ \vdots \\ \delta_L \end{bmatrix} \end{align}

Stacking equation (2) over all $i$ and $t$, we obtain $$ \boldsymbol{y}\ =\ \boldsymbol{X} \boldsymbol{\beta} + \boldsymbol{\varepsilon} \ =\ \boldsymbol{X}_0 \boldsymbol{\Gamma} + \boldsymbol{X}^{*} \boldsymbol{\delta} + \boldsymbol{\varepsilon} $$ or, using

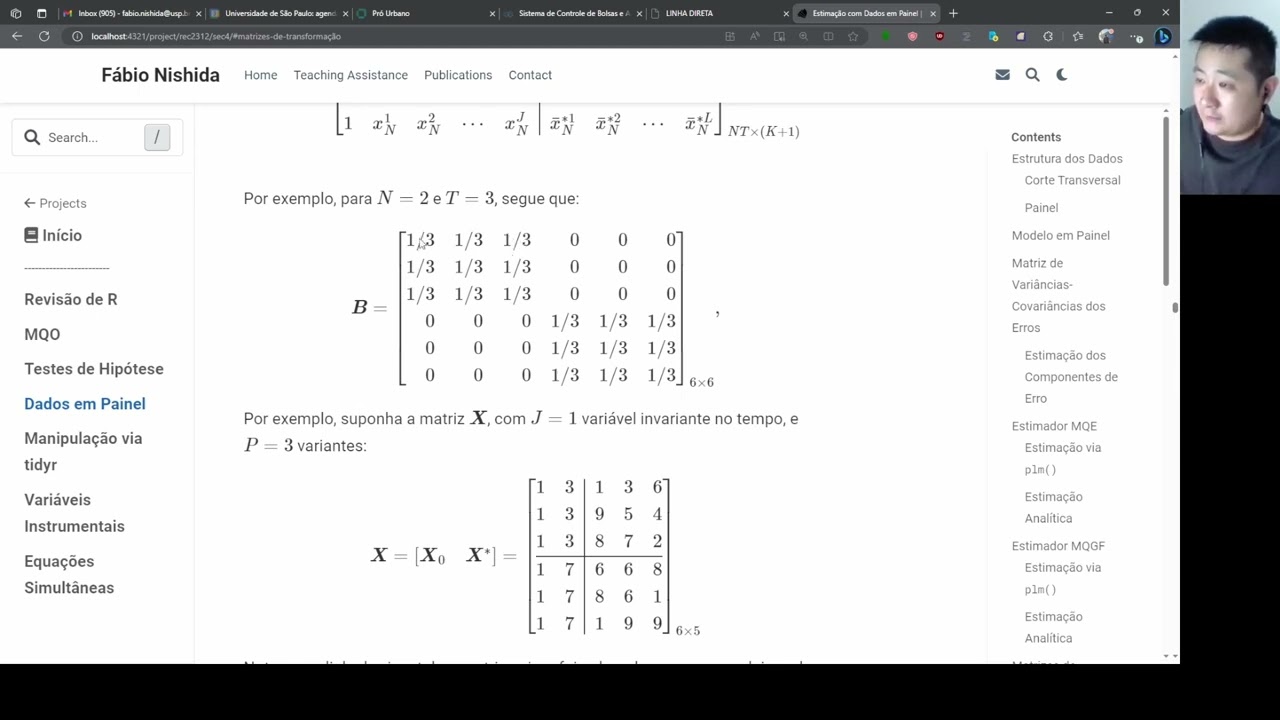

\begin{align} \boldsymbol{X} &= \left[ \begin{array}{ccccc|cccc} 1 & x^1_{11} & x^2_{11} & \cdots & x^J_{11} & x^{J+1}_{11} & x^{J+2}_{11} & \cdots & x^K_{11} \\ 1 & x^1_{12} & x^2_{12} & \cdots & x^J_{12} & x^{J+1}_{12} & x^{J+2}_{12} & \cdots & x^K_{12} \\ \vdots & \vdots & \vdots & \ddots & \vdots & \vdots & \vdots & \ddots & \vdots \\ 1 & x^1_{1T} & x^2_{1T} & \cdots & x^J_{1T} & x^{J+1}_{1T} & x^{J+2}_{1T} & \cdots & x^K_{1T} \\\hline 1 & x^1_{21} & x^2_{21} & \cdots & x^J_{21} & x^{J+1}_{21} & x^{J+2}_{21} & \cdots & x^K_{21} \\ 1 & x^1_{22} & x^2_{22} & \cdots & x^J_{22} & x^{J+1}_{22} & x^{J+2}_{22} & \cdots & x^K_{22} \\ \vdots & \vdots & \vdots & \ddots & \vdots & \vdots & \vdots & \ddots & \vdots \\ 1 & x^1_{2T} & x^2_{2T} & \cdots & x^J_{2T} & x^{J+1}_{2T} & x^{J+2}_{2T} & \cdots & x^K_{2T} \\\hline \vdots & \vdots & \vdots & \ddots & \vdots & \vdots & \vdots & \ddots & \vdots \\\hline 1 & x^1_{N1} & x^2_{N1} & \cdots & x^J_{N1} & x^{J+1}_{N1} & x^{J+2}_{N1} & \cdots & x^K_{21} \\ 1 & x^1_{N2} & x^2_{N2} & \cdots & x^J_{N2} & x^{J+1}_{N2} & x^{J+2}_{N2} & \cdots & x^K_{N2} \\ \vdots & \vdots & \vdots & \ddots & \vdots & \vdots & \vdots & \ddots & \vdots \\ 1 & x^1_{NT} & x^2_{NT} & \cdots & x^J_{NT} & x^{J+1}_{NT} & x^{J+2}_{NT} & \cdots & x^K_{NT} \end{array} \right] \\\\ \equiv \begin{bmatrix} \boldsymbol{X}_0, \boldsymbol{X}^{*} \end{bmatrix} &= \left[ \begin{array}{ccccc|cccc} 1 & x^1_{1} & x^2_{1} & \cdots & x^J_{1} & x^{*1}_{11} & x^{*2}_{11} & \cdots & x^{*L}_{11} \\ 1 & x^1_{1} & x^2_{1} & \cdots & x^J_{1} & x^{*1}_{12} & x^{*2}_{12} & \cdots & x^{*L}_{12} \\ \vdots & \vdots & \vdots & \ddots & \vdots & \vdots & \vdots & \ddots & \vdots \\ 1 & x^1_{1} & x^2_{1} & \cdots & x^J_{1} & x^{*1}_{1T} & x^{*2}_{1T} & \cdots & x^{*L}_{1T} \\\hline 1 & x^1_{2} & x^2_{2} & \cdots & x^J_{2} & x^{*1}_{21} & x^{*2}_{21} & \cdots & x^{*L}_{21} \\ 1 & x^1_{2} & x^2_{2} & \cdots & x^J_{2} & x^{*1}_{22} & x^{*2}_{22} & \cdots & x^{*L}_{22} \\ \vdots & \vdots & \vdots & \ddots & \vdots & \vdots & \vdots & \ddots & \vdots \\ 1 & x^1_{2} & x^2_{2} & \cdots & x^J_{2} & x^{*1}_{2T} & x^{*2}_{2T} & \cdots & x^{*L}_{2T} \\\hline \vdots & \vdots & \vdots & \ddots & \vdots & \vdots & \vdots & \ddots & \vdots \\\hline 1 & x^1_{N} & x^2_{N} & \cdots & x^J_{N} & x^{*1}_{N1} & x^{*2}_{N1} & \cdots & x^{*L}_{21} \\ 1 & x^1_{N} & x^2_{N} & \cdots & x^J_{N} & x^{*1}_{N2} & x^{*2}_{N2} & \cdots & x^{*L}_{N2} \\ \vdots & \vdots & \vdots & \ddots & \vdots & \vdots & \vdots & \ddots & \vdots \\ 1 & x^1_{N\ \ \ } & x^2_{N\ \ \ } & \cdots & x^J_{N\ \ \ } & x^{*1}_{NT} & x^{*2}_{NT} & \cdots & x^{*L}_{NT} \end{array} \right] \end{align}Between

The between (inter-individual) transformation matrix is denoted by: $$ \boldsymbol{B}\ =\ \boldsymbol{I}_N \otimes \Big[ \boldsymbol{\iota}_T (\boldsymbol{\iota}'_T \boldsymbol{\iota}_T)^{-1} \boldsymbol{\iota}'_T \Big] $$ Note that the matrix $\boldsymbol{B}$ corresponds to $\boldsymbol{N}$ in the Econometrics II lecture notes.

Premultiplying $\boldsymbol{X}$ by the between transformation matrix $\boldsymbol{B}$ yields: $$ x^k_{it}\ \overset{\boldsymbol{B}}{\Longrightarrow}\ \bar{x}^k_{i}\ =\ \frac{1}{T} \sum^T_{i=1}{x^k_{it}}, \qquad \forall i, t, k $$

Thus,

$$ \boldsymbol{BX} = \left[ \begin{array}{ccccc|cccc} 1 & x^1_{1} & x^2_{1} & \cdots & x^J_{1} & \bar{x}^{*1}_{1} & \bar{x}^{*2}_{1} & \cdots & \bar{x}^{*L}_{1} \\ 1 & x^1_{1} & x^2_{1} & \cdots & x^J_{1} & \bar{x}^{*1}_{1} & \bar{x}^{*2}_{1} & \cdots & \bar{x}^{*L}_{1} \\ \vdots & \vdots & \vdots & \ddots & \vdots & \vdots & \vdots & \ddots & \vdots \\ 1 & x^1_{1} & x^2_{1} & \cdots & x^J_{1} & \bar{x}^{*1}_{1} & \bar{x}^{*2}_{1} & \cdots & \bar{x}^{*L}_{1} \\\hline 1 & x^1_{2} & x^2_{2} & \cdots & x^J_{2} & \bar{x}^{*1}_{2} & \bar{x}^{*2}_{2} & \cdots & \bar{x}^{*L}_{2} \\ 1 & x^1_{2} & x^2_{2} & \cdots & x^J_{2} & \bar{x}^{*1}_{2} & \bar{x}^{*2}_{2} & \cdots & \bar{x}^{*L}_{2} \\ \vdots & \vdots & \vdots & \ddots & \vdots & \vdots & \vdots & \ddots & \vdots \\ 1 & x^1_{2} & x^2_{2} & \cdots & x^J_{2} & \bar{x}^{*1}_{2} & \bar{x}^{*2}_{2} & \cdots & \bar{x}^{*L}_{2} \\\hline \vdots & \vdots & \vdots & \ddots & \vdots & \vdots & \vdots & \ddots & \vdots \\\hline 1 & x^1_{N} & x^2_{N} & \cdots & x^J_{N} & \bar{x}^{*1}_{N} & \bar{x}^{*2}_{N} & \cdots & \bar{x}^{*L}_{2} \\ 1 & x^1_{N} & x^2_{N} & \cdots & x^J_{N} & \bar{x}^{*1}_{N} & \bar{x}^{*2}_{N} & \cdots & \bar{x}^{*L}_{N} \\ \vdots & \vdots & \vdots & \ddots & \vdots & \vdots & \vdots & \ddots & \vdots \\ 1 & x^1_{N} & x^2_{N} & \cdots & x^J_{N} & \bar{x}^{*1}_{N} & \bar{x}^{*2}_{N} & \cdots & \bar{x}^{*L}_{N} \end{array} \right]_{NT \times (K+1)} $$For example, when $N = 2$ and $T = 3$, we have:

$$ \boldsymbol{B} = \left[ \begin{array}{rrrrrr} 1/3 & 1/3 & 1/3 & 0 & 0 & 0 \\ 1/3 & 1/3 & 1/3 & 0 & 0 & 0 \\ 1/3 & 1/3 & 1/3 & 0 & 0 & 0 \\ 0 & 0 & 0 & 1/3 & 1/3 & 1/3 \\ 0 & 0 & 0 & 1/3 & 1/3 & 1/3 \\ 0 & 0 & 0 & 1/3 & 1/3 & 1/3 \end{array} \right]_{6 \times 6}, $$For instance, suppose $\boldsymbol{X}$ has $J=1$ time-invariant variable and $P=3$ time-varying variables:

$$ \boldsymbol{X} = \begin{bmatrix} \boldsymbol{X}_0 & \boldsymbol{X}^{*} \end{bmatrix} = \left[ \begin{array}{cc|ccc} 1 & 3 & 1 & 3 & 6 \\ 1 & 3 & 9 & 5 & 4 \\ 1 & 3 & 8 & 7 & 2 \\ \hline 1 & 7 & 6 & 6 & 8 \\ 1 & 7 & 8 & 6 & 1 \\ 1 & 7 & 1 & 9 & 9 \end{array} \right]_{6 \times 5} $$The horizontal separator is included only to emphasize that the first three rows refer to individual $i=1$ and the last three rows to individual $i=2$. There are three rows for each because we assume $t=1,2,3$.

Thus, we have:

\begin{align} \boldsymbol{BX} &= \left[ \begin{array}{rrrrrr} 1/3 & 1/3 & 1/3 & 0 & 0 & 0 \\ 1/3 & 1/3 & 1/3 & 0 & 0 & 0 \\ 1/3 & 1/3 & 1/3 & 0 & 0 & 0 \\\hline 0 & 0 & 0 & 1/3 & 1/3 & 1/3 \\ 0 & 0 & 0 & 1/3 & 1/3 & 1/3 \\ 0 & 0 & 0 & 1/3 & 1/3 & 1/3 \end{array} \right] \left[ \begin{array}{cc|ccc} 1 & 3 & 1 & 3 & 6 \\ 1 & 3 & 9 & 5 & 4 \\ 1 & 3 & 8 & 7 & 2 \\ \hline 1 & 7 & 6 & 6 & 8 \\ 1 & 7 & 8 & 6 & 1 \\ 1 & 7 & 1 & 9 & 9 \end{array} \right] \\ &= \left[ \begin{array}{cc|ccc} 1 & 3 & 6 & 5 & 4 \\ 1 & 3 & 6 & 5 & 4 \\ 1 & 3 & 6 & 5 & 4 \\ \hline 1 & 7 & 5 & 7 & 6 \\ 1 & 7 & 5 & 7 & 6 \\ 1 & 7 & 5 & 7 & 6 \end{array} \right]_{6 \times 5} \end{align}Note that, for each individual $i$ and column $k$, the entries are filled with that individual’s time average over $t=1,2,3$.

Now let us define a covariate matrix X and premultiply it by B.

N = 2 # nº individuals

T = 3 # nº periods

K = 4 # nº explanatory variables

# Computing the between transformation matrix

iota_T = matrix(1, nrow=T, ncol=1) # vector of ones of dimension T

I_N = diag(N) # identity matrix of dimension N

B = I_N %x% (iota_T %*% solve(t(iota_T) %*% iota_T) %*% t(iota_T))

B # between transformation matrix

## [,1] [,2] [,3] [,4] [,5] [,6]

## [1,] 0.3333333 0.3333333 0.3333333 0.0000000 0.0000000 0.0000000

## [2,] 0.3333333 0.3333333 0.3333333 0.0000000 0.0000000 0.0000000

## [3,] 0.3333333 0.3333333 0.3333333 0.0000000 0.0000000 0.0000000

## [4,] 0.0000000 0.0000000 0.0000000 0.3333333 0.3333333 0.3333333

## [5,] 0.0000000 0.0000000 0.0000000 0.3333333 0.3333333 0.3333333

## [6,] 0.0000000 0.0000000 0.0000000 0.3333333 0.3333333 0.3333333

# Covariate matrix X

X = matrix(c(rep(1, 6), # 1st column of 1s

rep(3, 3), rep(7, 3), # 2a coluna

1,9,8,6,8,1, # 3a coluna

3,5,7,6,6,9, # 4a coluna

6,4,2,8,1,9 # 5a coluna

), ncol=K+1) # covariate matrix of dimension NT x (K+1)

X

## [,1] [,2] [,3] [,4] [,5]

## [1,] 1 3 1 3 6

## [2,] 1 3 9 5 4

## [3,] 1 3 8 7 2

## [4,] 1 7 6 6 8

## [5,] 1 7 8 6 1

## [6,] 1 7 1 9 9

# Premultiplying X by B

B %*% X # matrix of individual-specific covariate means (NT x K)

## [,1] [,2] [,3] [,4] [,5]

## [1,] 1 3 6 5 4

## [2,] 1 3 6 5 4

## [3,] 1 3 6 5 4

## [4,] 1 7 5 7 6

## [5,] 1 7 5 7 6

## [6,] 1 7 5 7 6

Note that:

- Columns 1 and 2 remain unchanged after the between transformation because they are time-invariant (the average of a constant is the constant itself).

- for a given variable $k$, each individual $i$ is represented by a single average value;

- as a result, a sample with $NT$ observations is reduced to only $N$ distinct observations, so we lose $N(T-1)$ degrees of freedom.

Within

The within (intra-individual) transformation matrix is given by: $$ \boldsymbol{W}\ =\ \boldsymbol{I}_{NT} - \boldsymbol{B}\ =\ \boldsymbol{I}_{NT} - \Big[ \boldsymbol{I}_N \otimes \boldsymbol{\iota}_T (\boldsymbol{\iota}'_T \boldsymbol{\iota}_T)^{-1} \boldsymbol{\iota}'_T \Big]. $$

Note that the matrix $\boldsymbol{W}$ corresponds to $\boldsymbol{M}$ in the Econometrics II lecture notes (2021).

Premultiplying $\boldsymbol{X}$ by the within transformation matrix $\boldsymbol{W}$ yields: $$ x^{k}_{it}\ \overset{\boldsymbol{W}}{\Longrightarrow}\ x^{k}_{it} - \bar{x}^{k}_i\ =\ x^{k}_{it} - \frac{1}{T} \sum^T_{i=1}{x^{k}_{it}}, \qquad \forall i, t, l=1,...,L $$

Thus, \begin{align} \boldsymbol{WX} &= \left[ \begin{array}{ccc|cccc} 0 & \cdots & 0 & x^{*1}_{11} - \bar{x}^{*1}_{1} & x^{*2}_{11} - \bar{x}^{*2}_{1} & \cdots & x^{*L}_{11} - \bar{x}^{*L}_{1} \\ 0 & \cdots & 0 & x^{*1}_{12} - \bar{x}^{*1}_{1} & x^{*2}_{12} - \bar{x}^{*2}_{1} & \cdots & x^{*2}_{1T} - \bar{x}^{*L}_{1} \\ \vdots & \ddots & \vdots & \vdots & \vdots & \ddots & \vdots \\ 0 & \cdots & 0 & x^{*1}_{1T} - \bar{x}^{*1}_{1} & x^{*2}_{1T} - \bar{x}^{*2}_{1} & \cdots & x^{*L}_{1T} - \bar{x}^{*L}_{1} \\\hline 0 & \cdots & 0 & x^{*1}_{21} - \bar{x}^{*1}_{2} & x^{*2}_{21} - \bar{x}^{*2}_{2} & \cdots & x^{*L}_{21} - \bar{x}^{*L}_{2} \\ 0 & \cdots & 0 & x^{*1}_{22} - \bar{x}^{*1}_{2} & x^{*2}_{22} - \bar{x}^{*2}_{2} & \cdots & x^{*2}_{22} - \bar{x}^{*L}_{2} \\ \vdots & \ddots & \vdots & \vdots & \vdots & \ddots & \vdots \\ 0 & \cdots & 0 & x^{*1}_{2T} - \bar{x}^{*1}_{2} & x^{*2}_{2T} - \bar{x}^{*2}_{2} & \cdots & x^{*L}_{2T} - \bar{x}^{*L}_{2} \\\hline \vdots & \ddots & \vdots & \vdots & \vdots & \ddots & \vdots \\\hline 0 & \cdots & 0 & x^{*1}_{N1} - \bar{x}^{*1}_{N} & x^{*2}_{N1} - \bar{x}^{*2}_{N} & \cdots & x^{*L}_{N1} - \bar{x}^{*L}_{N} \\ 0 & \cdots & 0 & x^{*1}_{N2} - \bar{x}^{*1}_{N} & x^{*2}_{N2} - \bar{x}^{*2}_{N} & \cdots & x^{*2}_{N2} - \bar{x}^{*L}_{N} \\ \vdots & \ddots & \vdots & \vdots & \vdots & \ddots & \vdots \\ 0 & \cdots & 0 & x^{*1}_{NT} - \bar{x}^{*1}_{N} & x^{*2}_{NT} - \bar{x}^{*2}_{N} & \cdots & x^{*L}_{NT} - \bar{x}^{*L}_{N} \end{array} \right]_{NT \times L} \\ &= \boldsymbol{WX}^* \end{align}

For example, when $N = 2$ and $T = 3$, we have:

\begin{align} \boldsymbol{W} &= \boldsymbol{I}_{6} - \boldsymbol{B} \\ &= \left[ \begin{array}{cccccc} 1 & 0 & 0 & 0 & 0 & 0 \\ 0 & 1 & 0 & 0 & 0 & 0 \\ 0 & 0 & 1 & 0 & 0 & 0 \\ 0 & 0 & 0 & 1 & 0 & 0 \\ 0 & 0 & 0 & 0 & 1 & 0 \\ 0 & 0 & 0 & 0 & 0 & 1 \end{array} \right] - \left[ \begin{array}{rrrrrr} 1/3 & 1/3 & 1/3 & 0 & 0 & 0 \\ 1/3 & 1/3 & 1/3 & 0 & 0 & 0 \\ 1/3 & 1/3 & 1/3 & 0 & 0 & 0 \\ 0 & 0 & 0 & 1/3 & 1/3 & 1/3 \\ 0 & 0 & 0 & 1/3 & 1/3 & 1/3 \\ 0 & 0 & 0 & 1/3 & 1/3 & 1/3 \end{array} \right] \\ &= \left[ \begin{array}{rrrrrr} 2/6 & -1/3 & -1/3 & 0 & 0 & 0 \\ -1/3 & 2/6 & -1/3 & 0 & 0 & 0 \\ -1/3 & -1/3 & 2/6 & 0 & 0 & 0 \\ 0 & 0 & 0 & 2/6 & -1/3 & -1/3 \\ 0 & 0 & 0 & -1/3 & 2/6 & -1/3 \\ 0 & 0 & 0 & -1/3 & -1/3 & 2/6 \end{array} \right]_{6 \times 6} , \end{align}Thus, we have:

\begin{align} \boldsymbol{WX} = &\left[ \begin{array}{rrrrrr} 2/6 & -1/3 & -1/3 & 0 & 0 & 0 \\ -1/3 & 2/6 & -1/3 & 0 & 0 & 0 \\ -1/3 & -1/3 & 2/6 & 0 & 0 & 0 \\ 0 & 0 & 0 & 2/6 & -1/3 & -1/3 \\ 0 & 0 & 0 & -1/3 & 2/6 & -1/3 \\ 0 & 0 & 0 & -1/3 & -1/3 & 2/6 \end{array} \right] \\ &\left[ \begin{array}{cc|ccc} 1 & 3 & 1 & 3 & 6 \\ 1 & 3 & 9 & 5 & 4 \\ 1 & 3 & 8 & 7 & 2 \\ \hline 1 & 7 & 6 & 6 & 8 \\ 1 & 7 & 8 & 6 & 1 \\ 1 & 7 & 1 & 9 & 9 \end{array} \right] \\ = &\left[ \begin{array}{cc|ccc} 0 & 0 & -5 & -2 & 2 \\ 0 & 0 & 3 & 0 & 0 \\ 0 & 0 & 2 & 2 & -2 \\ \hline 0 & 0 & 1 & -1 & 2 \\ 0 & 0 & 3 & -1 & -5 \\ 0 & 0 & -4 & 2 & 3 \end{array} \right]_{6 \times 5} = \boldsymbol{WX}^* \end{align}Note that we lose all variation in the first two columns, which are time-invariant. In other words, the entire submatrix $\boldsymbol{X}_0$ drops out, leaving only $\boldsymbol{X}^{*}$ with the time-varying covariates.

I_NT = diag(N*T) # identity matrix of dimension NT

W = I_NT - B

W # within transformation matrix

## [,1] [,2] [,3] [,4] [,5] [,6]

## [1,] 0.6666667 -0.3333333 -0.3333333 0.0000000 0.0000000 0.0000000

## [2,] -0.3333333 0.6666667 -0.3333333 0.0000000 0.0000000 0.0000000

## [3,] -0.3333333 -0.3333333 0.6666667 0.0000000 0.0000000 0.0000000

## [4,] 0.0000000 0.0000000 0.0000000 0.6666667 -0.3333333 -0.3333333

## [5,] 0.0000000 0.0000000 0.0000000 -0.3333333 0.6666667 -0.3333333

## [6,] 0.0000000 0.0000000 0.0000000 -0.3333333 -0.3333333 0.6666667

# Premultiplying X by W

round(W %*% X, 10) # rounding

## [,1] [,2] [,3] [,4] [,5]

## [1,] 0 0 -5 -2 2

## [2,] 0 0 3 0 0

## [3,] 0 0 2 2 -2

## [4,] 0 0 1 -1 2

## [5,] 0 0 3 -1 -5

## [6,] 0 0 -4 2 3

Observe que:

- for each variable $k$, we obtain deviations from the individual-specific mean;

- columns 1 and 2, which are time-invariant, become zero after the within transformation and therefore drop out of the regression.

- the zero column in R is numerically very close to zero ( $1.11 \times 10^{-16}$), so rounding is useful.

First Differences

- The first-difference matrix transforms variables into changes between periods $t+1$ and $t$, and has the following non-square form: $$\boldsymbol{D} = \boldsymbol{I}_N \otimes \boldsymbol{D}_i $$ where $\boldsymbol{I}_N$ is the identity matrix of size $N$, and

$$\boldsymbol{D}_i = \begin{bmatrix} -1 & 1 & 0 & \cdots & 0 & 0 \\ 0 & -1 & 1 & \cdots & 0 & 0 \\ \vdots & \vdots & \vdots & \ddots & \vdots & \vdots \\ 0 & 0 & 0 & \cdots & -1 & 1 \end{bmatrix}_{(T-1)\times T}$$ This is not a square matrix and has the main off-diagonals equal to $-1$ and $1$.

Premultiplying $\boldsymbol{X}$ by the first-difference transformation matrix $\boldsymbol{D}$ yields: $$ x^{k}_{it}\ \overset{\boldsymbol{D}}{\Longrightarrow}\ \Delta x^{k}_{it} \ =\ x^{k}_{i,t+1} - x^{k}_{it}, \qquad \forall i, k, t = 1, 2, ..., T-1 $$

Thus, \begin{align} \boldsymbol{DX} &= \left[ \begin{array}{c|cccc} 0 \cdots 0 & x^{*1}_{12} - x^{*1}_{11} & x^{*2}_{12} - x^{*2}_{11} & \cdots & x^{*L}_{12} - x^{*L}_{11} \\ 0 \cdots 0 & x^{*1}_{13} - x^{*1}_{12} & x^{*2}_{13} - x^{*2}_{12} & \cdots & x^{*2}_{13} - x^{*L}_{12} \\ \vdots \ddots \vdots & \vdots & \vdots & \ddots & \vdots \\ 0 \cdots 0 & x^{*1}_{1T} - x^{*1}_{1,T-1} & x^{*2}_{1T} - x^{*2}_{1,T-1} & \cdots & x^{*L}_{1T} - x^{*L}_{1,T-1} \\\hline 0 \cdots 0 & x^{*1}_{22} - x^{*1}_{21} & x^{*2}_{22} - x^{*2}_{21} & \cdots & x^{*L}_{22} - x^{*L}_{21} \\ 0 \cdots 0 & x^{*1}_{23} - x^{*1}_{2} & x^{*2}_{22} - x^{*2}_{2} & \cdots & x^{*2}_{23} - x^{*L}_{22} \\ \vdots \ddots \vdots & \vdots & \vdots & \ddots & \vdots \\ 0 \cdots 0 & x^{*1}_{2T} - x^{*1}_{2,T-1} & x^{*2}_{2T} - x^{*2}_{2,T-1} & \cdots & x^{*L}_{2T} - x^{*L}_{2,T-1} \\\hline \vdots \ddots \vdots & \vdots & \vdots & \ddots & \vdots \\\hline 0 \cdots 0 & x^{*1}_{N2} - x^{*1}_{N1} & x^{*2}_{N2} - x^{*2}_{N1} & \cdots & x^{*L}_{N2} - x^{*L}_{N1} \\ 0 \cdots 0 & x^{*1}_{N3} - x^{*1}_{N2} & x^{*2}_{N3} - x^{*2}_{N2} & \cdots & x^{*2}_{N3} - x^{*L}_{N2} \\ \vdots \ddots \vdots & \vdots & \vdots & \ddots & \vdots \\ 0 \cdots 0 & x^{*1}_{NT} - x^{*1}_{N,T-1} & x^{*2}_{NT} - x^{*2}_{N,T-1} & \cdots & x^{*L}_{NT} - x^{*L}_{N,T-1} \end{array} \right] \\ &= \underset{N(T-1) \times L}{\boldsymbol{DX}^*} \end{align}

For example, when $N = 2$ and $T = 3$, we have:

$$ \boldsymbol{D}_i = \begin{bmatrix} -1 & 1 & 0 \\ 0 & -1 & 1 \end{bmatrix}_{2 \times 3},\quad i=1,2 $$Thus, we have

\begin{align} \boldsymbol{DX} &= \left[ \begin{array}{rrr|rrr} -1 & 1 & 0 & 0 & 0 & 0 \\ 0 & -1 & 1 & 0 & 0 & 0 \\\hline 0 & 0 & 0 & -1 & 1 & 0 \\ 0 & 0 & 0 & 0 & -1 & 1 \end{array} \right] \left[ \begin{array}{cc|ccc} 1 & 3 & 1 & 3 & 6 \\ 1 & 3 & 9 & 5 & 4 \\ 1 & 3 & 8 & 7 & 2 \\ \hline 1 & 7 & 6 & 6 & 8 \\ 1 & 7 & 8 & 6 & 1 \\ 1 & 7 & 1 & 9 & 9 \end{array} \right] \\ &= \left[ \begin{array}{cc|ccc} 0 & 0 & 8 & 2 & -2 \\ 0 & 0 & -1 & 2 & -2 \\\hline 0 & 0 & 2 & 0 & -7 \\ 0 & 0 & -7 & 3 & 8 \end{array} \right]_{4 \times 5} = \boldsymbol{DX}^* \end{align}Note that we lose all variation in the first two columns, which are time-invariant $(\boldsymbol{X}_0)$. In addition, we lose one period for each individual $i$.

To build $\boldsymbol{D}_i$ in R, we:

a) create an identity matrix of size $T$ and multiply it by $-1$ $$ -\boldsymbol{I}_T = \begin{bmatrix} -1 & 0 & 0 \\ 0 & -1 & 0 \\ 0 & 0 & -1 \end{bmatrix} $$.

Di = -diag(T) # main diagonal set to -1

Di

## [,1] [,2] [,3]

## [1,] -1 0 0

## [2,] 0 -1 0

## [3,] 0 0 -1

b) modify the superdiagonal, which is the diagonal of the $(T-1)$ identity submatrix obtained by excluding the first column and the last row of the $T \times T$ matrix $$ \left[ \begin{array}{c|cc} -1 & 0 & 0 \\ 0 & -1 & 0 \\\hline 0 & 0 & -1 \end{array} \right] \Longrightarrow \left[ \begin{array}{ccc} -1 & 1 & 0 \\ 0 & -1 & 1 \\ 0 & 0 & -1 \end{array} \right] $$

diag(Di[-nrow(Di),-1]) = 1 # superdiagonal

Di

## [,1] [,2] [,3]

## [1,] -1 1 0

## [2,] 0 -1 1

## [3,] 0 0 -1

c) drop the last row, leaving a matrix of dimension $(T-1)\times T$ $$ \Longrightarrow \boldsymbol{D}_i = \left[ \begin{array}{ccc} -1 & 1 & 0 \\ 0 & -1 & 1 \end{array} \right]_{2 \times 3} $$

Di = Di[-nrow(Di),] # dropping the last row

Di

## [,1] [,2] [,3]

## [1,] -1 1 0

## [2,] 0 -1 1

Then we simply take the Kronecker product, $\otimes$, between the identity matrix $\boldsymbol{I}_N$ and $\boldsymbol{D}_i$:

\begin{align}\boldsymbol{D} &= \boldsymbol{I}_N \otimes \boldsymbol{D}_i \\ &= \begin{bmatrix} 1 & 0 \\ 0 & 1 \end{bmatrix}_{2 \times 2} \otimes \begin{pmatrix} 1 & -1 & 0 \\ 0 & 1 & -1 \end{pmatrix}_{2 \times 3} \\ &= \begin{bmatrix} 1\begin{pmatrix} 1 & -1 & 0 \\ 0 & 1 & -1 \end{pmatrix} & 0\begin{pmatrix} 1 & -1 & 0 \\ 0 & 1 & -1 \end{pmatrix} \\ 0\begin{pmatrix} 1 & -1 & 0 \\ 0 & 1 & -1 \end{pmatrix} & 1\begin{pmatrix} 1 & -1 & 0 \\ 0 & 1 & -1 \end{pmatrix} \end{bmatrix} \\ &= \left[\begin{array}{ccc|ccc} 1 & -1 & 0 & 0 & 0 & 0 \\ 0 & 1 & -1 & 0 & 0 & 0 \\\hline 0 & 0 & 0 & 1 & -1 & 0 \\ 0 & 0 & 0 & 0 & 1 & -1 \\ \end{array}\right]_{4 \times 6} \end{align}I_N = diag(N) # identity matrix of size N

D = I_N %x% Di

D # first-difference matrix

## [,1] [,2] [,3] [,4] [,5] [,6]

## [1,] -1 1 0 0 0 0

## [2,] 0 -1 1 0 0 0

## [3,] 0 0 0 -1 1 0

## [4,] 0 0 0 0 -1 1

# DX transformation

D %*% X

## [,1] [,2] [,3] [,4] [,5]

## [1,] 0 0 8 2 -2

## [2,] 0 0 -1 2 -2

## [3,] 0 0 2 0 -7

## [4,] 0 0 -7 3 8

Observe que:

- columns 1 and 2, which are time-invariant, become zero after first differencing and therefore drop out of the regression.

- we also lose one row per individual in order to compute changes across periods.

Between Estimator

The model to be estimated is OLS premultiplied by $\boldsymbol{B} = \boldsymbol{I}_N \otimes \boldsymbol{\iota} (\boldsymbol{\iota}' \boldsymbol{\iota})^{-1} \boldsymbol{\iota}'$: $$ \boldsymbol{By}\ =\ \boldsymbol{BX\beta} + \boldsymbol{B\varepsilon} $$

The between estimator is given by $$ \hat{\boldsymbol{\beta}}_{\scriptscriptstyle{B}}\ =\ (\boldsymbol{X}' \boldsymbol{B} \boldsymbol{X} )^{-1} \boldsymbol{X}' \boldsymbol{B} y $$

Defina $$ \hat{\sigma}^2_l \equiv \hat{\sigma}^2_v + T \hat{\sigma}^2_u $$

The covariance matrix of the estimator can be written as \begin{align} V(\hat{\boldsymbol{\beta}}_{\scriptscriptstyle{B}}) &= (\boldsymbol{X}'\boldsymbol{BX})^{-1} \boldsymbol{X}' \boldsymbol{B}\boldsymbol{\Sigma} \boldsymbol{B} \boldsymbol{X} (\boldsymbol{X}'\boldsymbol{BX})^{-1} \\ &\ \ \vdots \\ &= \hat{\sigma}^2_l (\boldsymbol{X}' \boldsymbol{B} \boldsymbol{X})^{-1}, \end{align}

The unbiased estimator of $\sigma^2_l$ is $$ \hat{\sigma}^2_l = \frac{\hat{\boldsymbol{\varepsilon}_{\scriptscriptstyle{B}}}' \boldsymbol{B} \hat{\boldsymbol{\varepsilon}_{\scriptscriptstyle{B}}}}{N-K-1} $$ where $\boldsymbol{\varepsilon}_{\scriptscriptstyle{B}}$ denotes the residual vector obtained from $\hat{\boldsymbol{\beta}}_{\scriptscriptstyle{B}}$.

The between estimator can also be obtained by OLS after premultiplying the variables by the between matrix $(\boldsymbol{B})$: $$ \tilde{\boldsymbol{X}} \equiv \boldsymbol{BX} \qquad \text{and} \qquad \tilde{\boldsymbol{y}} \equiv \boldsymbol{By} $$

Then \begin{align} \hat{\boldsymbol{\beta}}_{\scriptscriptstyle{B}} &= (\boldsymbol{X}' \boldsymbol{B} \boldsymbol{X} )^{-1} \boldsymbol{X}' \boldsymbol{B} y \\ &= (\boldsymbol{X}' \boldsymbol{B} \boldsymbol{B} \boldsymbol{X} )^{-1} \boldsymbol{X}' \boldsymbol{B} \boldsymbol{B} y \\ &= (\boldsymbol{X}' \boldsymbol{B}' \boldsymbol{B} \boldsymbol{X} )^{-1} \boldsymbol{X}' \boldsymbol{B}' \boldsymbol{B} y \\ &= ([\boldsymbol{B} \boldsymbol{X}]' \boldsymbol{B} \boldsymbol{X} )^{-1} [\boldsymbol{B} \boldsymbol{X}]' \boldsymbol{B} y \\ &\equiv ( \tilde{\boldsymbol{X}}' \tilde{\boldsymbol{X}} )^{-1} \tilde{\boldsymbol{X}}' \tilde{\boldsymbol{y}} = \tilde{\hat{\boldsymbol{\beta}}}_{\scriptscriptstyle{OLS}} \end{align}

Note that we use: $$ \boldsymbol{B} = \boldsymbol{B}\boldsymbol{B} \qquad \text{and} \qquad \boldsymbol{B}=\boldsymbol{B}' $$

Estimation via plm()

Again, we use the TobinQ dataset from the pder package and estimate the following model:

$$ \text{ikn} = \beta_0 + \text{qn} \beta_1 + \varepsilon $$

# Loading the required package and dataset

library(plm)

data(TobinQ, package="pder")

# Converting to `pdata.frame` format with individual and time identifiers

pTobinQ = pdata.frame(TobinQ, index=c("cusip", "year"))

# Estimations

Q.between = plm(ikn ~ qn, pTobinQ, model = "between")

summary(Q.between)

## Oneway (individual) effect Between Model

##

## Call:

## plm(formula = ikn ~ qn, data = pTobinQ, model = "between")

##

## Balanced Panel: n = 188, T = 35, N = 6580

## Observations used in estimation: 188

##

## Residuals:

## Min. 1st Qu. Median 3rd Qu. Max.

## -0.109457 -0.027820 -0.009795 0.024550 0.193177

##

## Coefficients:

## Estimate Std. Error t-value Pr(>|t|)

## (Intercept) 0.15601353 0.00388203 40.1886 < 2.2e-16 ***

## qn 0.00518474 0.00074907 6.9216 7.013e-11 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Total Sum of Squares: 0.50783

## Residual Sum of Squares: 0.40382

## R-Squared: 0.20482

## Adj. R-Squared: 0.20054

## F-statistic: 47.9079 on 1 and 186 DF, p-value: 7.0128e-11

Analytical Estimation

a) Criando vetores/matrizes e definindo N, T e K

data("TobinQ", package="pder")

# Creating the y vector

y = as.matrix(TobinQ[,"ikn"]) # converting the data frame column into a matrix

# Creating the covariate matrix X with a first column of ones

X = as.matrix( cbind(1, TobinQ[, "qn"]) ) # adding a column of ones to the covariates

# Retrieving N, T, and K

N = length( unique(TobinQ$cusip) )

T = length( unique(TobinQ$year) )

K = ncol(X) - 1

b) Calculando a matriz between

$$ \boldsymbol{B} = \boldsymbol{I}_{N} \otimes \left[ \boldsymbol{\iota}_T \left( \boldsymbol{\iota}'_T \boldsymbol{\iota}_T \right)^{-1} \boldsymbol{\iota}'_T \right] $$# Creating the between matrix

iota_T = matrix(1, T, 1) # column vector of 1s of length T

I_N = diag(N) # identity matrix of size N

B = I_N %x% (iota_T %*% solve(t(iota_T) %*% iota_T) %*% t(iota_T))

c) Between estimates $\hat{\boldsymbol{\beta}}_{\scriptscriptstyle{B}}$

$$ \hat{\boldsymbol{\beta}}_{\scriptscriptstyle{B}} = (\boldsymbol{X}' \boldsymbol{B} \boldsymbol{X})^{-1} \boldsymbol{X}' \boldsymbol{B} \boldsymbol{y} $$bhat_B = solve( t(X) %*% B %*% X ) %*% t(X) %*% B %*% y

bhat_B

## [,1]

## [1,] 0.156013534

## [2,] 0.005184737

d) Fitted values Between $\hat{\boldsymbol{y}}_{\scriptscriptstyle{B}}$

$$ \hat{\boldsymbol{y}}_{\scriptscriptstyle{B}} = \boldsymbol{X} \hat{\boldsymbol{\beta}}_{\scriptscriptstyle{B}} $$yhat_B = X %*% bhat_B

e) Residuals Between $\hat{\boldsymbol{\varepsilon}}_{\scriptscriptstyle{B}}$

$$ \hat{\boldsymbol{\varepsilon}}_{\scriptscriptstyle{B}} = \boldsymbol{y} - \hat{\boldsymbol{y}}_{\scriptscriptstyle{B}} $$ehat_B = y - yhat_B

f) Error-term variance

$$ \hat{\sigma}^2_l \equiv \frac{\hat{\boldsymbol{\varepsilon}}'_{\scriptscriptstyle{B}} \boldsymbol{B} \hat{\boldsymbol{\varepsilon}}_{\scriptscriptstyle{B}}}{N - K - 1} $$Because

$\hat{\sigma}^2_l$ is a scalar, it is convenient to convert the “1x1 matrix” into a number using as.numeric():

# Computing the error-term variances

sig2l = as.numeric( (t(ehat_B) %*% B %*% ehat_B) / (N - K - 1) )

IMPORTANT: Adjust the degrees of freedom of the between estimator to $N - K - 1$ (instead of $NT - K - 1$).

g) Estimator Variance-Covariance Matrix Between

$$ \widehat{\text{Var}}(\hat{\boldsymbol{\beta}}_{\scriptscriptstyle{B}}) = \hat{\sigma}^2_l (\boldsymbol{X}' B \boldsymbol{X})^{-1} $$# Computing the variance-covariance matrix of the estimators

Vbhat_B = sig2l * solve( t(X) %*% B %*% X )

Vbhat_B

## [,1] [,2]

## [1,] 1.507017e-05 -1.405770e-06

## [2,] -1.405770e-06 5.611075e-07

i) Standard errors $\text{se}(\hat{\boldsymbol{\beta}}_{\scriptscriptstyle{B}})$

It is the square root of the main diagonal of the estimator variance-covariance matrix.

se_bhat_B = sqrt( diag(Vbhat_B) )

se_bhat_B

## [1] 0.0038820321 0.0007490711

j) t statistic

$$ t_{\hat{\beta}_k} = \frac{\hat{\beta}_k}{\text{se}(\hat{\beta}_k)} \tag{4.6} $$# Computing the t statistic

t_bhat_B = bhat_B / se_bhat_B

t_bhat_B

## [,1]

## [1,] 40.188625

## [2,] 6.921555

k) p-value

$$ p_{\hat{\beta}_k} = 2.\Phi_{t_{(N-K-1)}}(-|t_{\hat{\beta}_k}|), \tag{4.7} $$# p-value

p_bhat_B = 2 * pt(-abs(t_bhat_B), N-K-1)

p_bhat_B

## [,1]

## [1,] 1.227764e-93

## [2,] 7.012814e-11

l) Summary table

data.frame(bhat_B, se_bhat_B, t_bhat_B, p_bhat_B) # _Between_ result

## bhat_B se_bhat_B t_bhat_B p_bhat_B

## 1 0.156013534 0.0038820321 40.188625 1.227764e-93

## 2 0.005184737 0.0007490711 6.921555 7.012814e-11

summary(Q.between)$coef # _Between_ result via plm()

## Estimate Std. Error t-value Pr(>|t|)

## (Intercept) 0.156013534 0.0038820321 40.188625 1.227764e-93

## qn 0.005184737 0.0007490711 6.921555 7.012814e-11

Transforming and Estimating by OLS

In addition to the form shown above, we can transform the variables and solve by OLS after premultiplying $\boldsymbol{X}$ and $\boldsymbol{y}$ by $\boldsymbol{B}$, defining: