- We now turn to more general hypothesis tests that are not usually reported directly in standard regression output.

Wald Test

Consider:

- $G$: the number of linear restrictions

- $\boldsymbol{\beta}$: a $(K+1) \times 1$ parameter vector

- $\boldsymbol{h}$: a $G \times 1$ vector of constants

- $\boldsymbol{R}$: a $G \times (K+1)$ matrix formed by stacking $G$ row vectors $\boldsymbol{r}'_g$ of dimension $1 \times (K+1)$, for $g=1, 2, ..., G$

- A multivariate model:

Using these matrices and vectors, we can write hypothesis tests in the form: \begin{align} \text{H}_0: &\underset{G\times (K+1)}{\boldsymbol{R}} \underset{(K+1)\times 1}{\boldsymbol{\beta}} = \underset{G \times 1}{\boldsymbol{h}} \\ \text{H}_0: &\left[ \begin{matrix} \boldsymbol{r}'_1 \\ \boldsymbol{r}'_2 \\ \vdots \\ \boldsymbol{r}'_{G} \end{matrix} \right] \boldsymbol{\beta} = \left[ \begin{matrix} h_1 \\ h_2 \\ \vdots \\ h_G \end{matrix} \right] \\ \text{H}_0: &\left\{ \begin{matrix} \boldsymbol{r}'_1 \boldsymbol{\beta} = h_1 \\ \boldsymbol{r}'_2 \boldsymbol{\beta} = h_2 \\ \vdots \\ \boldsymbol{r}'_G \boldsymbol{\beta} = h_G \end{matrix} \right. \end{align}

One Linear Restriction

Consider the model: $$y = \beta_0 + \beta_1 x_1 + \beta_2 x_2 + \varepsilon$$

There are $K=2$ explanatory variables (and therefore 3 parameters).

One linear restriction $\Longrightarrow \ G=1$

In this particular case, we have $$\boldsymbol{R} = \boldsymbol{r}'_1\ \implies\ \text{H}_0:\ \boldsymbol{r}'_1 \boldsymbol{\beta} = h_1 $$

Evaluating the Null Hypothesis with a Single Restriction

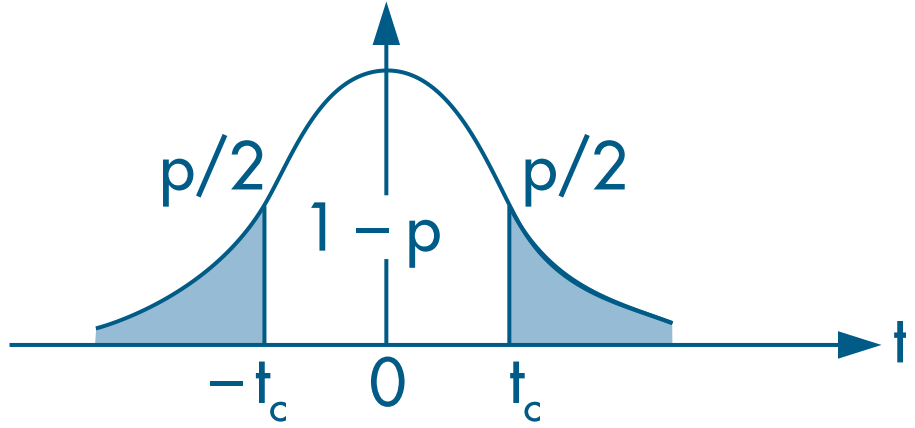

With a single restriction, we assume that $$ \boldsymbol{r}'_1 \hat{\boldsymbol{\beta}} \sim N(\boldsymbol{r}'_1 \hat{\boldsymbol{\beta}};\ \boldsymbol{r}'_1 \boldsymbol{V(\hat{\boldsymbol{\beta}}) r_1})$$

The Wald statistic is then computed as follows. With a single restriction, it coincides with the usual t statistic: $$ w = t = \frac{\boldsymbol{r}'_1 \hat{\boldsymbol{\beta}} - h_1}{\sqrt{\boldsymbol{r}'_1 \hat{\sigma}^2 (\boldsymbol{X}'\boldsymbol{X})^{-1} \boldsymbol{r}_1}} = \frac{\boldsymbol{r}'_1 \hat{\boldsymbol{\beta}} - h_1}{\sqrt{\boldsymbol{r}'_1 \boldsymbol{V(\hat{\boldsymbol{\beta}})} \boldsymbol{r}_1}} $$

Choose a significance level $\alpha$ and reject the null hypothesis when the t statistic lies outside the relevant confidence interval.

Example 1: H$_0: \ \beta_1 = 4$

- Note that $h_1 = 4$.

- The vector $r'_1$ can be written as

So the null hypothesis is $$\text{H}_0:\ \boldsymbol{r}'_1 \boldsymbol{\beta}\ =\ \left[ \begin{matrix} 0 & 1 & 0 \end{matrix} \right] \left[ \begin{matrix} \beta_0 \\ \beta_1 \\ \beta_2 \end{matrix} \right] = 4\ \iff\ \beta_1 = 4 $$

And the denominator of the t statistic is: \begin{align} &\sqrt{\boldsymbol{r}'_1 \boldsymbol{V(\hat{\boldsymbol{\beta}})} \boldsymbol{r}_1} \\ &= \sqrt{\left[ \begin{matrix} 0 & 1 & 0 \end{matrix} \right] {\small \begin{bmatrix} var(\hat{\beta}_0) & cov(\hat{\beta}_0, \hat{\beta}_1) & cov(\hat{\beta}_0, \hat{\beta}_2) \\ cov(\hat{\beta}_0, \hat{\beta}_1) & var(\hat{\beta}_1) & cov(\hat{\beta}_1, \hat{\beta}_2) \\ cov(\hat{\beta}_0, \hat{\beta}_2) & cov(\hat{\beta}_1, \hat{\beta}_2) & var(\hat{\beta}_2) \\ \end{bmatrix}} \left[ \begin{matrix} 0 \\ 1 \\ 0 \end{matrix} \right]} \\ &= \sqrt{\small{\begin{bmatrix} cov(\hat{\beta}_0, \hat{\beta}_1) & var(\hat{\beta}_1) & cov(\hat{\beta}_1, \hat{\beta}_2) \end{bmatrix}} \left[ \begin{matrix} 0 \\ 1 \\ 0 \end{matrix} \right]} \\ &= \sqrt{var(\hat{\beta}_1)} = se(\hat{\beta}_1) \end{align}

Example 2: H$_0: \ \beta_1 + \beta_2 = 2$

- Note that $h_1 = 2$.

- The vector $r'_1$ can be written as

So the null hypothesis is $$\text{H}_0:\ \boldsymbol{r}'_1 \boldsymbol{\beta}\ =\ \left[ \begin{matrix} 0 & 1 & 1 \end{matrix} \right] \left[ \begin{matrix} \beta_0 \\ \beta_1 \\ \beta_2 \end{matrix} \right] = 2\ \iff\ \beta_1 + \beta_2 = 2 $$

And the denominator of the t statistic is: \begin{align} &\sqrt{\boldsymbol{r}'_1 \boldsymbol{V(\hat{\boldsymbol{\beta}})} \boldsymbol{r}_1} \\ &= \sqrt{\left[ \begin{matrix} 0 & 1 & 1 \end{matrix} \right] {\small \begin{bmatrix} var(\hat{\beta}_0) & cov(\hat{\beta}_0, \hat{\beta}_1) & cov(\hat{\beta}_0, \hat{\beta}_2) \\ cov(\hat{\beta}_0, \hat{\beta}_1) & var(\hat{\beta}_1) & cov(\hat{\beta}_1, \hat{\beta}_2) \\ cov(\hat{\beta}_0, \hat{\beta}_2) & cov(\hat{\beta}_1, \hat{\beta}_2) & var(\hat{\beta}_2) \\ \end{bmatrix}} \left[ \begin{matrix} 0 \\ 1 \\ 1 \end{matrix} \right]} \\ &= \sqrt{\small{\begin{bmatrix} cov(\hat{\beta}_0, \hat{\beta}_1)+cov(\hat{\beta}_0, \hat{\beta}_2) \\ var(\hat{\beta}_1) + cov(\hat{\beta}_1, \hat{\beta}_2) \\ cov(\hat{\beta}_1, \hat{\beta}_2) + var(\hat{\beta}_2) \end{bmatrix}}' \left[ \begin{matrix} 0 \\ 1 \\ 1 \end{matrix} \right]} \\ &= \sqrt{var(\hat{\beta}_1) + var(\hat{\beta}_2) + 2cov(\hat{\beta}_1, \hat{\beta}_2)} = \sqrt{var(\hat{\beta}_1 + \hat{\beta}_2)} \end{align}

Example 3: H$_0: \ \beta_1 = \beta_2$

Note that $$\beta_1 = \beta_2 \iff \beta_1 - \beta_2 = 0 $$

Hence, $h_1 = 0$.

The vector $r'_1$ can be written as

So the null hypothesis is $$\text{H}_0:\ \boldsymbol{r}'_1 \boldsymbol{\beta}\ =\ \left[ \begin{matrix} 0 & 1 & -1 \end{matrix} \right] \left[ \begin{matrix} \beta_0 \\ \beta_1 \\ \beta_2 \end{matrix} \right] = 0\ \iff\ \beta_1 - \beta_2 = 0 $$

And the denominator of the t statistic is: \begin{align} &\sqrt{\boldsymbol{r}'_1 \boldsymbol{V(\hat{\boldsymbol{\beta}})} \boldsymbol{r}_1} \\ &= \sqrt{\left[ \begin{matrix} 0 & 1 & -1 \end{matrix} \right] {\small \begin{bmatrix} var(\hat{\beta}_0) & cov(\hat{\beta}_0, \hat{\beta}_1) & cov(\hat{\beta}_0, \hat{\beta}_2) \\ cov(\hat{\beta}_0, \hat{\beta}_1) & var(\hat{\beta}_1) & cov(\hat{\beta}_1, \hat{\beta}_2) \\ cov(\hat{\beta}_0, \hat{\beta}_2) & cov(\hat{\beta}_1, \hat{\beta}_2) & var(\hat{\beta}_2) \\ \end{bmatrix}} \left[ \begin{matrix} 0 \\ 1 \\ -1 \end{matrix} \right]} \\ &= \sqrt{\small{\begin{bmatrix} cov(\hat{\beta}_0, \hat{\beta}_1)-cov(\hat{\beta}_0, \hat{\beta}_2) \\ var(\hat{\beta}_1) - cov(\hat{\beta}_1, \hat{\beta}_2) \\ cov(\hat{\beta}_1, \hat{\beta}_2) - var(\hat{\beta}_2) \end{bmatrix}}' \left[ \begin{matrix} 0 \\ 1 \\ -1 \end{matrix} \right]} \\ &= \sqrt{var(\hat{\beta}_1) + var(\hat{\beta}_2) - 2cov(\hat{\beta}_1, \hat{\beta}_2)} = \sqrt{var(\hat{\beta}_1 - \hat{\beta}_2)} \end{align}

Implementing It in R

(Continued) Example 7.5: Log Hourly Wage Equation (Wooldridge, 2006)

- Earlier, we estimated the following model:

\begin{align} \log(\text{wage}) = &\beta_0 + \beta_1 \text{female} + \beta_2 \text{married} + \delta_2 \text{female*married} + \beta_3 \text{educ} +\\ &\beta_4 \text{exper} + \beta_5 \text{exper}^2 + \beta_6 \text{tenure} + \beta_7 \text{tenure}^2 + \varepsilon \end{align} where:

wage: average hourly wagefemale: dummy equal to (1) for women and (0) for menmarried: dummy equal to (1) for married individuals and (0) otherwisefemale*married: interaction term between thefemaleandmarrieddummieseduc: years of educationexper: years of experience (expersq= years squared)tenure: years with the current employer (tenursq= years squared)

# Loading the required dataset

data(wage1, package="wooldridge")

# Estimating the model

res_7.14 = lm(lwage ~ female*married + educ + exper + expersq + tenure + tenursq, data=wage1)

round( summary(res_7.14)$coef, 4 )

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 0.3214 0.1000 3.2135 0.0014

## female -0.1104 0.0557 -1.9797 0.0483

## married 0.2127 0.0554 3.8419 0.0001

## educ 0.0789 0.0067 11.7873 0.0000

## exper 0.0268 0.0052 5.1118 0.0000

## expersq -0.0005 0.0001 -4.8471 0.0000

## tenure 0.0291 0.0068 4.3016 0.0000

## tenursq -0.0005 0.0002 -2.3056 0.0215

## female:married -0.3006 0.0718 -4.1885 0.0000

- We can see that the effect of marriage for women differs from the effect for men because the coefficient on

female:married( $\delta_2$) is statistically significant. - However, to determine whether the effect of marriage for women is itself significant, we need to test whether H$_0 :\ \beta_2 + \delta_2 = 0$.

- Because there is only one restriction, we can evaluate this hypothesis with a t test:

# Extracting objects from the regression

bhat = matrix(coef(res_7.14), ncol=1) # coefficients as a column vector

Vbhat = vcov(res_7.14) # variance-covariance matrix of the estimator

N = nrow(wage1) # number of observations

K = length(bhat) - 1 # number of covariates

ehat = residuals(res_7.14) # regression residuals

# Building the row vector for the restriction

r1prime = matrix(c(0, 0, 1, 0, 0, 0, 0, 0, 1), nrow=1) # restriction vector

h1 = 0 # constant in H0

G = 1 # number of restrictions

# Computing the t statistic

t = (r1prime %*% bhat - h1) / sqrt(r1prime %*% Vbhat %*% t(r1prime))

abs(t)

## [,1]

## [1,] 1.679475

# Computing the p-value

p = 2 * pt(-abs(t), N-K-1)

p

## [,1]

## [1,] 0.09366368

Since $|t| < 2$ (an approximate critical value for a 5% significance level), we do not reject the null hypothesis and conclude that the effect of marriage on women’s wages ( $\beta_2 + \delta_2$) is not statistically significant.

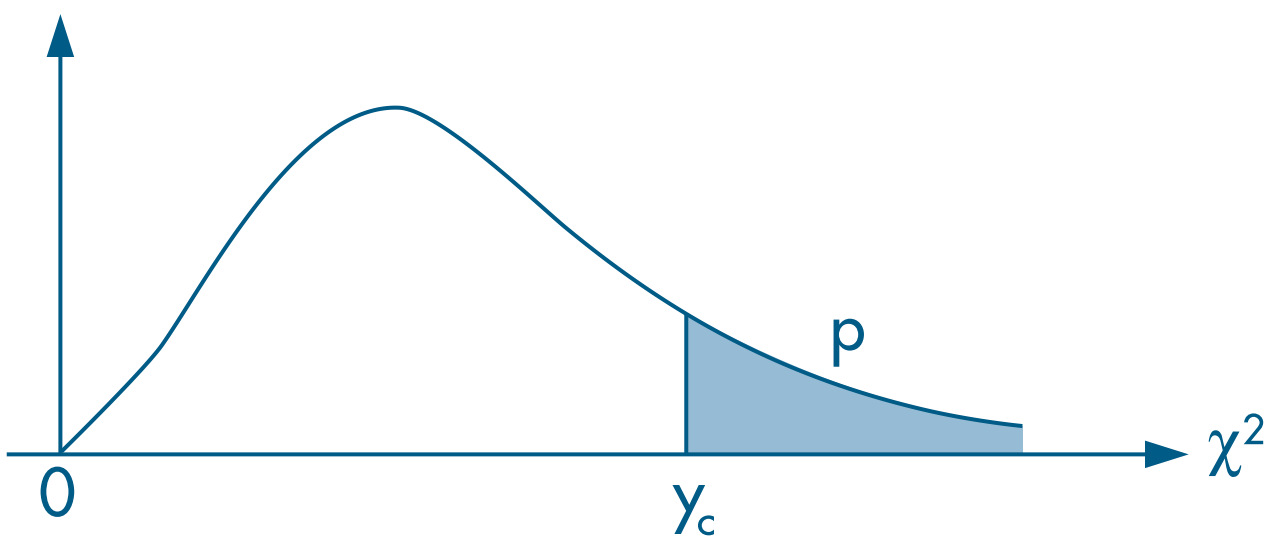

We can also assess the same restriction with a Wald test, evaluating the statistic against a $\chi^2$ distribution with 1 degree of freedom (because there is only $G=1$ restriction).

Recall that the chi-squared test is right-tailed.

# Computing the Wald statistic

aux = r1prime %*% bhat - h1 # R \beta - h

w = t(aux) %*% solve( r1prime %*% Vbhat %*% t(r1prime)) %*% aux

w

## [,1]

## [1,] 2.820636

# Computing the p-value for w

p = 1 - pchisq(w, df=G)

p

## [,1]

## [1,] 0.09305951

Multiple Linear Restrictions

Evaluating the Null Hypothesis with Multiple Restrictions

With G restrictions, we assume that $$ \boldsymbol{R} \hat{\boldsymbol{\beta}} \sim N(\boldsymbol{R} \hat{\boldsymbol{\beta}};\ \sigma^2 \boldsymbol{R} \boldsymbol{V(\hat{\boldsymbol{\beta}}) R'})$$

The Wald statistic is then $$ w = \left[ \boldsymbol{R}\hat{\boldsymbol{\beta}} - \boldsymbol{h} \right]' \left[ \boldsymbol{R V(\hat{\beta}) R}' \right]^{-1} \left[ \boldsymbol{R}\hat{\boldsymbol{\beta}} - \boldsymbol{h} \right]\ \sim\ \chi^2_{(G)} $$

Choose a significance level $\alpha$ and reject the null hypothesis when the statistic $w$ falls outside the acceptance region (from zero to the critical value).

Example 4: H$_0: \ \beta_1 = 0\ \text{ e }\ \beta_1 + \beta_2 = 2$

- Note that $h_1 = 0 \text{ and } h_2 = 2$.

- The vectors $r'_1 \text{ and } r'_2$ can be written as

Therefore, $\boldsymbol{R}$ is $$ \boldsymbol{R} = \left[ \begin{matrix} \boldsymbol{r}'_1 \\ \boldsymbol{r}'_2 \end{matrix} \right] = \left[ \begin{matrix} 0 & 1 & 0 \\ 0 & 1 & 1 \end{matrix} \right] $$

So the null hypothesis is $$\text{H}_0:\ \boldsymbol{R} \boldsymbol{\beta} = \left[ \begin{matrix} 0 & 1 & 0 \\ 0 & 1 & 1 \end{matrix} \right] \left[ \begin{matrix} \beta_0 \\ \beta_1 \\ \beta_2 \end{matrix} \right] = \left[ \begin{matrix} h_1 \\ h_2 \end{matrix} \right]\ \iff\ \text{H}_0:\ \left\{ \begin{matrix} \beta_1 &= 0 \\ \beta_1 + \beta_2 &= 2 \end{matrix} \right. $$

Implementing It in R

- As an example, we use the

mlb1dataset from thewooldridgepackage, which contains baseball-player statistics (Wooldridge, 2006, Section 4.5). - We want to estimate the model:

\begin{align} \log(\text{salary}) = &\beta_0 + \beta_1. \text{years} + \beta_2. \text{gameyr} + \beta_3. \text{bavg} + \\

&\beta_4 .\text{hrunsyr} + \beta_5. \text{rbisyr} + \varepsilon \end{align}

where:

log(salary): log salary in 1993years: years spent in Major League Baseballgamesyr: average number of games per yearbavg: career batting averagehrunsyr: average number of home runs per yearrbisyr: average number of runs batted in per year

data(mlb1, package="wooldridge")

# Estimating the full (unrestricted) model

resMLB = lm(log(salary) ~ years + gamesyr + bavg + hrunsyr + rbisyr, data=mlb1)

round(summary(resMLB)$coef, 5) # estimated coefficients

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 11.19242 0.28882 38.75184 0.00000

## years 0.06886 0.01211 5.68430 0.00000

## gamesyr 0.01255 0.00265 4.74244 0.00000

## bavg 0.00098 0.00110 0.88681 0.37579

## hrunsyr 0.01443 0.01606 0.89864 0.36947

## rbisyr 0.01077 0.00717 1.50046 0.13440

Individually, the variables

bavg,hrunsyr, andrbisyrare not statistically significant.We want to test whether they are jointly significant, that is, $$ \text{H}_0:\ \left\{ \begin{matrix} \beta_3 = 0 \\ \beta_4 = 0 \\ \beta_5 = 0\end{matrix} \right. $$

Thus, we have $$ \boldsymbol{R} = \left[ \begin{matrix} \boldsymbol{r}'_1 \\ \boldsymbol{r}'_2 \\ \boldsymbol{r}'_3 \end{matrix} \right] = \left[ \begin{matrix} 0 & 0 & 0 & 1 & 0 & 0 \\ 0 & 0 & 0 & 0 & 1 & 0 \\ 0 & 0 & 0 & 0 & 0 & 1 \end{matrix} \right] $$

Using Wald.test()

# Extracting the variance-covariance matrix of the estimator

Vbhat = vcov(resMLB)

round(Vbhat, 5)

## (Intercept) years gamesyr bavg hrunsyr rbisyr

## (Intercept) 0.08342 0.00001 -0.00027 -0.00029 -0.00148 0.00082

## years 0.00001 0.00015 -0.00001 0.00000 -0.00002 0.00001

## gamesyr -0.00027 -0.00001 0.00001 0.00000 0.00002 -0.00002

## bavg -0.00029 0.00000 0.00000 0.00000 0.00000 0.00000

## hrunsyr -0.00148 -0.00002 0.00002 0.00000 0.00026 -0.00010

## rbisyr 0.00082 0.00001 -0.00002 0.00000 -0.00010 0.00005

# Computing the Wald statistic

# install.packages("aod") # installing the required package

aod::wald.test(Sigma = Vbhat, # variance-covariance matrix

b = coef(resMLB), # estimated coefficients

Terms = 4:6, # positions of the parameters to be tested

H0 = c(0, 0, 0) # vector h (all equal to zero)

)

## Wald test:

## ----------

##

## Chi-squared test:

## X2 = 28.7, df = 3, P(> X2) = 2.7e-06

- We reject the null hypothesis and therefore conclude that the parameters $\beta_3, \beta_4 \text{ and } \beta_5$ are jointly significant.

Computing It By Hand

- Estimating the model

# Creating the log_salary variable

mlb1$log_salary = log(mlb1$salary)

name_y = "log_salary"

names_X = c("years", "gamesyr", "bavg", "hrunsyr", "rbisyr")

# Creating the y vector

y = as.matrix(mlb1[,name_y]) # converting a data-frame column to a matrix

# Creating the covariate matrix X with a first column of 1s

X = as.matrix( cbind( const=1, mlb1[,names_X] ) ) # binding a column of 1s to the covariates

# Extracting N and K

N = nrow(mlb1)

K = ncol(X) - 1

# Estimating the model

bhat = solve( t(X) %*% X ) %*% t(X) %*% y

round(bhat, 5)

## [,1]

## const 11.19242

## years 0.06886

## gamesyr 0.01255

## bavg 0.00098

## hrunsyr 0.01443

## rbisyr 0.01077

# Computing residuals

ehat = y - X %*% bhat

# Variance of the error term

sig2hat = as.numeric( t(ehat) %*% ehat / (N-K-1) )

# Variance-covariance matrix of the estimator

Vbhat = sig2hat * solve( t(X) %*% X )

round(Vbhat, 5)

## const years gamesyr bavg hrunsyr rbisyr

## const 0.08342 0.00001 -0.00027 -0.00029 -0.00148 0.00082

## years 0.00001 0.00015 -0.00001 0.00000 -0.00002 0.00001

## gamesyr -0.00027 -0.00001 0.00001 0.00000 0.00002 -0.00002

## bavg -0.00029 0.00000 0.00000 0.00000 0.00000 0.00000

## hrunsyr -0.00148 -0.00002 0.00002 0.00000 0.00026 -0.00010

## rbisyr 0.00082 0.00001 -0.00002 0.00000 -0.00010 0.00005

- Next, we build the restriction matrix.

# Number of restrictions

G = 3

# Restriction matrix

R = matrix(c(0, 0, 0, 1, 0, 0,

0, 0, 0, 0, 1, 0,

0, 0, 0, 0, 0, 1),

nrow=G, byrow=TRUE)

R

## [,1] [,2] [,3] [,4] [,5] [,6]

## [1,] 0 0 0 1 0 0

## [2,] 0 0 0 0 1 0

## [3,] 0 0 0 0 0 1

# Vector of constants h

h = matrix(c(0, 0, 0),

nrow=3, ncol=1)

h

## [,1]

## [1,] 0

## [2,] 0

## [3,] 0

- Remember that, by default,

matrix()fills a matrix by column. - Here, however, it is more intuitive to fill the restriction matrix by row, since each row corresponds to one restriction. That is why we used

byrow=TRUE. - The Wald statistic is therefore $$ w(\hat{\boldsymbol{\beta}}) = \left[ \boldsymbol{R}\hat{\boldsymbol{\beta}} - \boldsymbol{h} \right]' \left[ \boldsymbol{R V_{\hat{\beta}} R}' \right]^{-1} \left[ \boldsymbol{R}\hat{\boldsymbol{\beta}} - \boldsymbol{h} \right]\ \sim\ \chi^2_{(G)} $$

# Wald statistic

w = t( R %*% bhat - h ) %*% solve( R %*% Vbhat %*% t(R) ) %*% (R %*% bhat - h)

w

## [,1]

## [1,] 28.65076

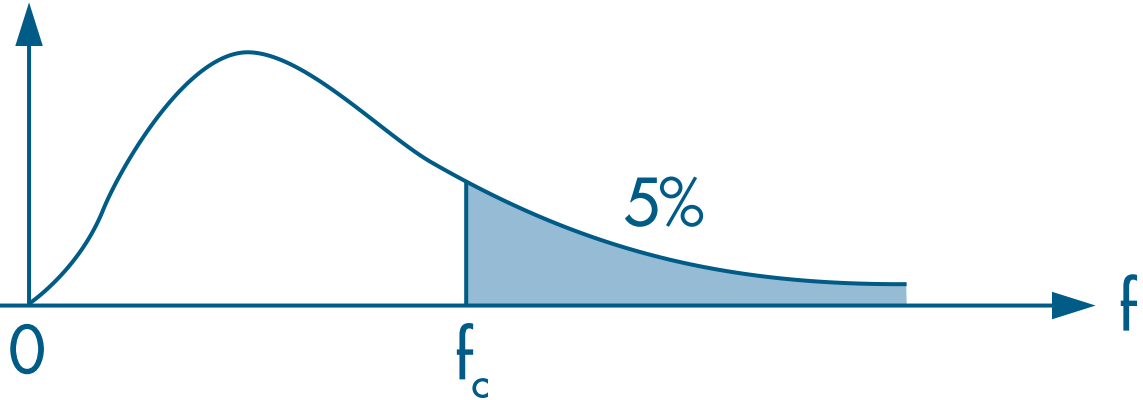

# Finding the 5% chi-squared critical value

alpha = 0.05

c = qchisq(1-alpha, df=G)

c

## [1] 7.814728

# Comparing the Wald statistic with the critical value

w > c

## [,1]

## [1,] TRUE

- Since the Wald statistic (= 28.65) is larger than the critical value (= 7.81), we reject the joint null hypothesis that all tested parameters are equal to zero.

- We could also evaluate the corresponding p-value:

1 - pchisq(w, df=G)

## [,1]

## [1,] 2.651604e-06

- Since it is smaller than 5%, we reject the null hypothesis.

F Test

- Section 4.3 of Heiss (2020)

- Another way to evaluate multiple restrictions is with the F test.

- Here we estimate two models:

- Unrestricted: includes all explanatory variables of interest

- Restricted: excludes some variables from the specification

- The F test compares the residual sums of squares (RSS) or the R$^2$ values of the two models.

- The intuition is straightforward: if the excluded variables are jointly significant, then the unrestricted model should have greater explanatory power.

- The F statistic can be computed as:

where

urdenotes the unrestricted model andrdenotes the restricted model.We then evaluate the F statistic using a right-tailed test based on the F distribution:

Implementing It in R

We continue using the

mlb1dataset from Section 4.5 of Wooldridge (2006).The unrestricted model (including all explanatory variables) is \begin{align} \log(\text{salary}) = &\beta_0 + \beta_1. \text{years} + \beta_2. \text{gameyr} + \beta_3. \text{bavg} + \\ &\beta_4 .\text{hrunsyr} + \beta_5. \text{rbisyr} + \varepsilon \end{align}

The restricted model (excluding the variables under test) is \begin{align} \log(\text{salary}) = &\beta_0 + \beta_1. \text{years} + \beta_2. \text{gameyr} + \varepsilon \end{align}

Using linearHypothesis()

- We can compute the F test with

linearHypothesis()from thecarpackage. - Besides the regression object, we must also provide a character vector listing the restrictions:

# Estimating the unrestricted model

res.ur = lm(log(salary) ~ years + gamesyr + bavg + hrunsyr + rbisyr, data=mlb1)

# Creating the vector of restrictions

myH0 = c("bavg = 0", "hrunsyr = 0", "rbisyr = 0")

# Applying the F test

# install.packages("car") # installing the required package

car::linearHypothesis(res.ur, myH0)

## Linear hypothesis test

##

## Hypothesis:

## bavg = 0

## hrunsyr = 0

## rbisyr = 0

##

## Model 1: restricted model

## Model 2: log(salary) ~ years + gamesyr + bavg + hrunsyr + rbisyr

##

## Res.Df RSS Df Sum of Sq F Pr(>F)

## 1 350 198.31

## 2 347 183.19 3 15.125 9.5503 4.474e-06 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

- In the second row (the unrestricted model), the residual sum of squares is lower than in the restricted model. So, as expected, the larger set of covariates provides more explanatory power.

- To evaluate the null hypothesis ( $\beta_3 = \beta_4 = \beta_5 = 0$), we can either compare the F statistic with a critical value or check whether the p-value is below the chosen significance level.

- From the p-value criterion above, we reject the null hypothesis.

- The 5% critical value can be obtained with:

qf(1-0.05, G, N-K-1)

## [1] 2.630641

- Since 9.55 > 2.63, we reject the null hypothesis.

Computing It By Hand

- Here we obtain the restricted and unrestricted estimates from

lm()directly, so we do not need to rework every estimation step from scratch.

# Estimating the unrestricted model

res.ur = lm(log(salary) ~ years + gamesyr + bavg + hrunsyr + rbisyr, data=mlb1)

# Estimating the restricted model

res.r = lm(log(salary) ~ years + gamesyr, data=mlb1)

# Extracting the R2 values from the regression results

r2.ur = summary(res.ur)$r.squared

r2.ur

## [1] 0.6278028

r2.r = summary(res.r)$r.squared

r2.r

## [1] 0.5970716

# Computing the F statistic

F = ( r2.ur - r2.r ) / (1 - r2.ur) * (N-K-1) / G

F

## [1] 9.550254

# F-test p-value

1 - pf(F, G, N-K-1)

## [1] 4.473708e-06