- We now turn to more general forms of hypothesis testing that are not usually reported automatically in basic regression output.

Wald Test

Consider:

- $G$: the number of linear restrictions;

- $\boldsymbol{\beta}$: the $(K+1) \times 1$ parameter vector;

- $\boldsymbol{h}$: a $G \times 1$ vector of constants;

- $\boldsymbol{R}$: a $G \times (K+1)$ matrix made up of row vectors $\boldsymbol{r}'_g$ of dimension $1 \times (K+1)$, for $g=1, 2, ..., G$;

- the multivariate model:

Using these matrices and vectors, we can write hypothesis tests of the form: \begin{align} \text{H}_0: &\underset{G\times (K+1)}{\boldsymbol{R}} \underset{(K+1)\times 1}{\boldsymbol{\beta}} = \underset{G \times 1}{\boldsymbol{h}} \\ \text{H}_0: &\left[ \begin{matrix} \boldsymbol{r}'_1 \\ \boldsymbol{r}'_2 \\ \vdots \\ \boldsymbol{r}'_{G} \end{matrix} \right] \boldsymbol{\beta} = \left[ \begin{matrix} h_1 \\ h_2 \\ \vdots \\ h_G \end{matrix} \right] \\ \text{H}_0: &\left\{ \begin{matrix} \boldsymbol{r}'_1 \boldsymbol{\beta} = h_1 \\ \boldsymbol{r}'_2 \boldsymbol{\beta} = h_2 \\ \vdots \\ \boldsymbol{r}'_G \boldsymbol{\beta} = h_G \end{matrix} \right. \end{align}

A Single Linear Restriction

Consider the model: $$y = \beta_0 + \beta_1 x_1 + \beta_2 x_2 + u$$

There are $K=2$ explanatory variables, hence 3 parameters.

One linear restriction implies $G=1$.

In this specific case, $$\boldsymbol{R} = \boldsymbol{r}'_1\ \implies\ \text{H}_0:\ \boldsymbol{r}'_1 \boldsymbol{\beta} = h_1 $$

Example 1: H$_0: \ \beta_1 = 4$

- Here $h_1 = 4$

- The vector $r'_1$ can be written as

- So the null hypothesis is $$\text{H}_0:\ \left[ \begin{matrix} 0 & 1 & 0 \end{matrix} \right] \left[ \begin{matrix} \beta_0 \\ \beta_1 \\ \beta_2 \end{matrix} \right] = 4\ \iff\ \beta_1 = 4 $$

Example 2: H$_0: \ \beta_1 + \beta_2 = 2$

- Here $h_1 = 2$

- The vector $r'_1$ can be written as

- So the null hypothesis is $$\text{H}_0:\ \left[ \begin{matrix} 0 & 1 & 1 \end{matrix} \right] \left[ \begin{matrix} \beta_0 \\ \beta_1 \\ \beta_2 \end{matrix} \right] = 2\ \iff\ \beta_1 + \beta_2 = 2 $$

Example 3: H$_0: \ \beta_1 = \beta_2$

Note that $$\beta_1 = \beta_2 \iff \beta_1 - \beta_2 = 0 $$

Therefore $h_1 = 0$

The vector $r'_1$ can be written as

- So the null hypothesis is $$\text{H}_0:\ \left[ \begin{matrix} 0 & 1 & -1 \end{matrix} \right] \left[ \begin{matrix} \beta_0 \\ \beta_1 \\ \beta_2 \end{matrix} \right] = 0\ \iff\ \beta_1 - \beta_2 = 0 $$

Implementing It in R

Evaluating the Null with a Single Restriction

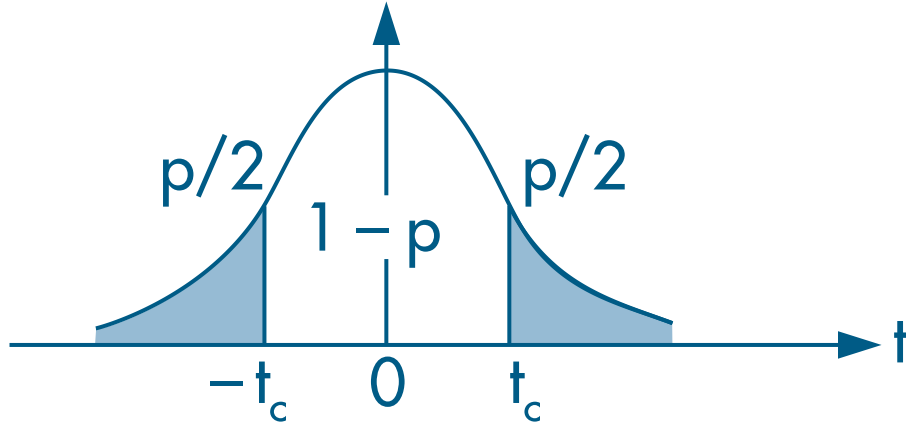

In the case of a single restriction, we assume that $$ \boldsymbol{r}'_1 \hat{\boldsymbol{\beta}} \sim N(\boldsymbol{r}'_1 \hat{\boldsymbol{\beta}};\ \boldsymbol{r}'_1 \boldsymbol{V_{\beta(x)} r_1})$$

The corresponding t statistic is $$ t = \frac{\boldsymbol{r}'_1 \hat{\boldsymbol{\beta}} - h_1}{\sqrt{\boldsymbol{r}'_1 S^2 (\boldsymbol{X}'\boldsymbol{X})^{-1} \boldsymbol{r}_1}} = \frac{\boldsymbol{r}'_1 \hat{\boldsymbol{\beta}} - h_1}{\sqrt{\boldsymbol{r}'_1 \boldsymbol{V_{\beta(x)}} \boldsymbol{r}_1}} $$

In small samples, we also need to assume that $ u|x \sim N(0; \sigma^2) $.

Choose a significance level $\alpha$ and reject the null if the t statistic falls outside the acceptance region.

(Continued) Example 7.5: The Log Wage Equation (Wooldridge, 2006)

- Earlier, we estimated the following model:

\begin{align} \log(\text{wage}) = &\beta_0 + \beta_1 \text{female} + \beta_2 \text{married} + \delta_2 \text{female*married} + \beta_3 \text{educ} +\\ &\beta_4 \text{exper} + \beta_5 \text{exper}^2 + \beta_6 \text{tenure} + \beta_7 \text{tenure}^2 + u \end{align} where:

wage: average hourly wagefemale: dummy equal to 1 for women and 0 for menmarried: dummy equal to 1 for married individuals and 0 for unmarried individualsfemale*married: interaction between thefemaleandmarrieddummieseduc: years of educationexper: years of experience (expersq= years squared)tenure: years with the current employer (tenursq= years squared)

# Load the required dataset

data(wage1, package="wooldridge")

# Estimate the model

res_7.14 = lm(lwage ~ female*married + educ + exper + expersq + tenure + tenursq, data=wage1)

round( summary(res_7.14)$coef, 4 )

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 0.3214 0.1000 3.2135 0.0014

## female -0.1104 0.0557 -1.9797 0.0483

## married 0.2127 0.0554 3.8419 0.0001

## educ 0.0789 0.0067 11.7873 0.0000

## exper 0.0268 0.0052 5.1118 0.0000

## expersq -0.0005 0.0001 -4.8471 0.0000

## tenure 0.0291 0.0068 4.3016 0.0000

## tenursq -0.0005 0.0002 -2.3056 0.0215

## female:married -0.3006 0.0718 -4.1885 0.0000

- We already know that the effect of marriage differs between women and men because the coefficient on

female:married( $\delta_2$) is significant. - However, to assess whether the effect of marriage on women’s wages is itself significant, we need to test whether H$_0 :\ \beta_2 + \delta_2 = 0$.

- Since there is only one restriction, the hypothesis can be evaluated with a t test:

# Extract regression objects

bhat = matrix(coef(res_7.14), ncol=1) # coefficients as a column vector

Vbhat = vcov(res_7.14) # variance-covariance matrix of the estimator

N = nrow(wage1) # number of observations

K = length(bhat) - 1 # number of covariates

uhat = residuals(res_7.14) # regression residuals

# Create the row vector that defines the restriction

r1prime = matrix(c(0, 0, 1, 0, 0, 0, 0, 0, 1), nrow=1) # restriction vector

h1 = 0 # constant under H0

G = 1 # number of restrictions

# Compute the t test

t = (r1prime %*% bhat - h1) / sqrt(r1prime %*% Vbhat %*% t(r1prime))

abs(t)

## [,1]

## [1,] 1.679475

# Compute the 5% two-sided critical value

c = qt(1 - 0.05/2, df=N-K-1)

c

## [1] 1.964563

# Compute the p-value

p = pt(-abs(t), N-K-1) * 2

p

## [,1]

## [1,] 0.09366368

Since $|t| < 2$ (an approximate 5% critical value), we do not reject the null hypothesis and conclude that the effect of marriage on women’s wages ( $\beta_2 + \delta_2$) is not statistically significant.

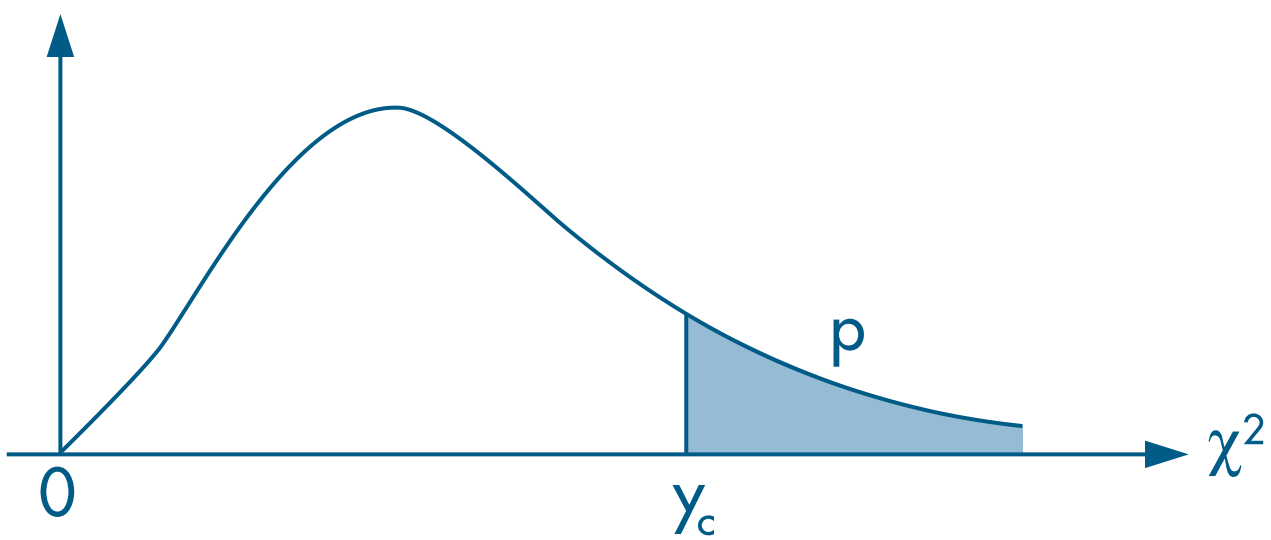

We can also evaluate the same restriction using the Wald test and the $\chi^2$ distribution with 1 degree of freedom, since there is only one restriction ( $G=1$).

Remember that the chi-squared test is right-tailed.

# Compute the Wald statistic

aux = r1prime %*% bhat - h1 # R beta - h

w = t(aux) %*% solve( r1prime %*% Vbhat %*% t(r1prime)) %*% aux

w

## [,1]

## [1,] 2.820636

# Compute the 5% chi-squared critical value

c = qchisq(1-0.05, df=G)

c

## [1] 3.841459

# Compute the p-value of w

p = 1 - pchisq(w, df=G)

p

## [,1]

## [1,] 0.09305951

Multiple Linear Restrictions

Example 4: H$_0: \ \beta_1 = 0\ \text{ e }\ \beta_1 + \beta_2 = 2$

- Here $h_1 = 0 \text{ and } h_2 = 2$

- The vectors $r'_1 \text{ and } r'_2$ can be written as

Therefore, $\boldsymbol{R}$ is $$ \boldsymbol{R} = \left[ \begin{matrix} \boldsymbol{r}'_1 \\ \boldsymbol{r}'_2 \end{matrix} \right] = \left[ \begin{matrix} 0 & 1 & 0 \\ 0 & 1 & 1 \end{matrix} \right] $$

So the null hypothesis is $$\text{H}_0:\ \boldsymbol{R} \boldsymbol{\beta} = \left[ \begin{matrix} 0 & 1 & 0 \\ 0 & 1 & 1 \end{matrix} \right] \left[ \begin{matrix} \beta_0 \\ \beta_1 \\ \beta_2 \end{matrix} \right] = \left[ \begin{matrix} h_1 \\ h_2 \end{matrix} \right]\ \iff\ \text{H}_0:\ \left\{ \begin{matrix} \beta_1 &= 0 \\ \beta_1 + \beta_2 &= 2 \end{matrix} \right. $$

Evaluating the Null with Multiple Restrictions

In the case of G restrictions, we assume that $$ \boldsymbol{R} \hat{\boldsymbol{\beta}} \sim N(\boldsymbol{R} \hat{\boldsymbol{\beta}};\ \sigma^2 \boldsymbol{R} \boldsymbol{V_{\beta(x)} R'})$$

The Wald statistic is $$ w(\hat{\boldsymbol{\beta}}) = \left[ \boldsymbol{R}\hat{\boldsymbol{\beta}} - \boldsymbol{h} \right]' \left[ \boldsymbol{R V_{\hat{\beta}} R}' \right]^{-1} \left[ \boldsymbol{R}\hat{\boldsymbol{\beta}} - \boldsymbol{h} \right]\ \sim\ \chi^2_{(G)} $$

Choose a significance level $\alpha$ and reject the null if the statistic $ w(\hat{\boldsymbol{\beta}})$ exceeds the critical value.

Implementing It in R

- As an example, we use the

mlb1dataset with statistics for Major League Baseball players (Wooldridge, 2006, Section 4.5). - We want to estimate the model: \begin{align} \log(\text{salary}) = &\beta_0 + \beta_1. \text{years} + \beta_2. \text{gameyr} + \beta_3. \text{bavg} + \\ &\beta_4 .\text{hrunsyr} + \beta_5. \text{rbisyr} + u \end{align}

where:

log(salary): log of 1993 salaryyears: years playing in Major League Baseballgamesyr: average number of games per yearbavg: career batting averagehrunsyr: average home runs per yearrbisyr: average runs batted in per year

data(mlb1, package="wooldridge")

# Estimate the full (unrestricted) model

resMLB = lm(log(salary) ~ years + gamesyr + bavg + hrunsyr + rbisyr, data=mlb1)

round(summary(resMLB)$coef, 5) # estimated coefficients

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 11.19242 0.28882 38.75184 0.00000

## years 0.06886 0.01211 5.68430 0.00000

## gamesyr 0.01255 0.00265 4.74244 0.00000

## bavg 0.00098 0.00110 0.88681 0.37579

## hrunsyr 0.01443 0.01606 0.89864 0.36947

## rbisyr 0.01077 0.00717 1.50046 0.13440

Notice that

bavg,hrunsyr, andrbisyrare individually statistically insignificant.We want to evaluate whether they are jointly significant, that is, $$ \text{H}_0:\ \left\{ \begin{matrix} \beta_3 = 0 \\ \beta_4 = 0 \\ \beta_5 = 0\end{matrix} \right. $$

Therefore, $$ \boldsymbol{R} = \left[ \begin{matrix} \boldsymbol{r}'_1 \\ \boldsymbol{r}'_2 \\ \boldsymbol{r}'_3 \end{matrix} \right] = \left[ \begin{matrix} 0 & 0 & 0 & 1 & 0 & 0 \\ 0 & 0 & 0 & 0 & 1 & 0 \\ 0 & 0 & 0 & 0 & 0 & 1 \end{matrix} \right] $$

Using the Wald.test() Function

# Extract the variance-covariance matrix of the estimator

Vbhat = vcov(resMLB)

round(Vbhat, 5)

## (Intercept) years gamesyr bavg hrunsyr rbisyr

## (Intercept) 0.08342 0.00001 -0.00027 -0.00029 -0.00148 0.00082

## years 0.00001 0.00015 -0.00001 0.00000 -0.00002 0.00001

## gamesyr -0.00027 -0.00001 0.00001 0.00000 0.00002 -0.00002

## bavg -0.00029 0.00000 0.00000 0.00000 0.00000 0.00000

## hrunsyr -0.00148 -0.00002 0.00002 0.00000 0.00026 -0.00010

## rbisyr 0.00082 0.00001 -0.00002 0.00000 -0.00010 0.00005

# Compute the Wald statistic

# install.packages("aod") # install the required package

aod::wald.test(Sigma = Vbhat, # variance-covariance matrix

b = coef(resMLB), # estimates

Terms = 4:6, # positions of the parameters being tested

H0 = c(0, 0, 0) # null hypothesis (all equal to zero)

)

## Wald test:

## ----------

##

## Chi-squared test:

## X2 = 28.7, df = 3, P(> X2) = 2.7e-06

# Wald test for the effect of root

# aod::wald.test(b = coef(resMLB), Sigma = vcov(resMLB), L=R, H0=h)

- We reject the null hypothesis and conclude that the parameters $\beta_3, \beta_4 \text{ and } \beta_5$ are jointly significant.

Computing It “By Hand”

- Estimate the model

# Create the variable log_salary

mlb1$log_salary = log(mlb1$salary)

name_y = "log_salary"

names_X = c("years", "gamesyr", "bavg", "hrunsyr", "rbisyr")

# Create vector y

y = as.matrix(mlb1[,name_y]) # convert data-frame column into a matrix

# Create the covariate matrix X with a leading column of 1s

X = as.matrix( cbind( const=1, mlb1[,names_X] ) ) # bind 1s to the covariates

# Retrieve N and K

N = nrow(mlb1)

K = ncol(X) - 1

# Estimate the model

bhat = solve( t(X) %*% X ) %*% t(X) %*% y

round(bhat, 5)

## [,1]

## const 11.19242

## years 0.06886

## gamesyr 0.01255

## bavg 0.00098

## hrunsyr 0.01443

## rbisyr 0.01077

# Compute residuals

uhat = y - X %*% bhat

# Error-term variance

S2 = as.numeric( t(uhat) %*% uhat / (N-K-1) )

# Variance-covariance matrix of the estimator

Vbhat = S2 * solve( t(X) %*% X )

round(Vbhat, 5)

## const years gamesyr bavg hrunsyr rbisyr

## const 0.08342 0.00001 -0.00027 -0.00029 -0.00148 0.00082

## years 0.00001 0.00015 -0.00001 0.00000 -0.00002 0.00001

## gamesyr -0.00027 -0.00001 0.00001 0.00000 0.00002 -0.00002

## bavg -0.00029 0.00000 0.00000 0.00000 0.00000 0.00000

## hrunsyr -0.00148 -0.00002 0.00002 0.00000 0.00026 -0.00010

## rbisyr 0.00082 0.00001 -0.00002 0.00000 -0.00010 0.00005

- Now create the restriction matrix:

# Number of restrictions

G = 3

# Restriction matrix

R = matrix(c(0, 0, 0, 1, 0, 0,

0, 0, 0, 0, 1, 0,

0, 0, 0, 0, 0, 1),

nrow=G, byrow=TRUE)

R

## [,1] [,2] [,3] [,4] [,5] [,6]

## [1,] 0 0 0 1 0 0

## [2,] 0 0 0 0 1 0

## [3,] 0 0 0 0 0 1

# Vector of constants h

h = matrix(c(0, 0, 0),

nrow=3, ncol=1)

h

## [,1]

## [1,] 0

## [2,] 0

## [3,] 0

- Remember that

matrix()fills by column by default. - Here it is more intuitive to fill the restrictions by row, since each row represents one restriction. That is why we used

byrow=TRUE. - The Wald statistic is then $$ w(\hat{\boldsymbol{\beta}}) = \left[ \boldsymbol{R}\hat{\boldsymbol{\beta}} - \boldsymbol{h} \right]' \left[ \boldsymbol{R V_{\hat{\beta}} R}' \right]^{-1} \left[ \boldsymbol{R}\hat{\boldsymbol{\beta}} - \boldsymbol{h} \right]\ \sim\ \chi^2_{(G)} $$

# Wald statistic

w = t( R %*% bhat - h ) %*% solve( R %*% Vbhat %*% t(R) ) %*% (R %*% bhat - h)

w

## [,1]

## [1,] 28.65076

# Find the 5% chi-squared critical value

alpha = 0.05

c = qchisq(1-alpha, df=G)

c

## [1] 7.814728

# Compare the Wald statistic with the critical value

w > c

## [,1]

## [1,] TRUE

- Since the Wald statistic (= 28.65) is greater than the critical value (= 7.81), we reject the joint null that all tested parameters are equal to zero.

- We can also evaluate the p-value from the Wald statistic:

1 - pchisq(w, df=G)

## [,1]

## [1,] 2.651604e-06

- Because it is below 5%, we reject the null hypothesis.

F Test

- Section 4.3 of Heiss (2020)

- Another way to evaluate multiple restrictions is with the F test.

- Here we estimate two models:

- unrestricted: includes all explanatory variables of interest;

- restricted: excludes some variables.

- The F test compares the residual sum of squares (RSS) or the R$^2$ of the two models.

- The intuition is straightforward: if the excluded variables are jointly significant, the unrestricted model should fit the data better.

- The F statistic can be computed as

where ur denotes the unrestricted model and r denotes the restricted model.

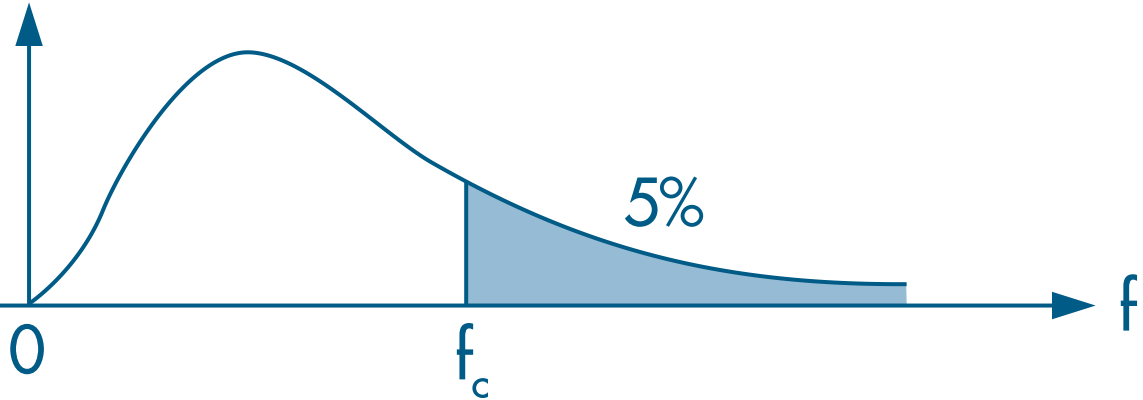

- We then evaluate the statistic using a right-tailed F test:

Implementing It in R

We continue using the

mlb1dataset from Section 4.5 of Wooldridge (2006).The unrestricted model, with all explanatory variables, is \begin{align} \log(\text{salary}) = &\beta_0 + \beta_1. \text{years} + \beta_2. \text{gameyr} + \beta_3. \text{bavg} + \\ &\beta_4 .\text{hrunsyr} + \beta_5. \text{rbisyr} + u \end{align}

The restricted model, which excludes the tested variables, is \begin{align} \log(\text{salary}) = &\beta_0 + \beta_1. \text{years} + \beta_2. \text{gameyr} + u \end{align}

Using linearHypothesis()

- We can run the F test with the

linearHypothesis()function from thecarpackage. - In addition to the estimated model object, we provide a character vector listing the restrictions:

# Estimate the unrestricted model

res.ur = lm(log(salary) ~ years + gamesyr + bavg + hrunsyr + rbisyr, data=mlb1)

# Create a vector with the restrictions

myH0 = c("bavg = 0", "hrunsyr = 0", "rbisyr = 0")

# Apply the F test

# install.packages("car") # install the required package

car::linearHypothesis(res.ur, myH0)

## Linear hypothesis test

##

## Hypothesis:

## bavg = 0

## hrunsyr = 0

## rbisyr = 0

##

## Model 1: restricted model

## Model 2: log(salary) ~ years + gamesyr + bavg + hrunsyr + rbisyr

##

## Res.Df RSS Df Sum of Sq F Pr(>F)

## 1 350 198.31

## 2 347 183.19 3 15.125 9.5503 4.474e-06 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

- Notice that in the second row, which corresponds to the unrestricted model, the residual sum of squares (RSS) is smaller than in the restricted model. Hence the larger set of covariates provides more explanatory power, as expected.

- To evaluate the null hypothesis ( $\beta_3 = \beta_4 = \beta_5 = 0$), we can either compare the F statistic with a critical value or compare the p-value with the chosen significance level.

- From the p-value criterion above, we reject the null hypothesis.

- The 5% critical value can be obtained with:

qf(1-0.05, G, N-K-1)

## [1] 2.630641

- Since 9.55 > 2.63, we reject the null hypothesis.

Computing It “By Hand”

- Here we use the unrestricted and restricted models estimated with

lm()so that we do not need to redo the full estimation procedure twice.

# Estimate the unrestricted model

res.ur = lm(log(salary) ~ years + gamesyr + bavg + hrunsyr + rbisyr, data=mlb1)

# Estimate the restricted model

res.r = lm(log(salary) ~ years + gamesyr, data=mlb1)

# Extract the R2 from each fitted model

r2.ur = summary(res.ur)$r.squared

r2.ur

## [1] 0.6278028

r2.r = summary(res.r)$r.squared

r2.r

## [1] 0.5970716

# Compute the F statistic

F = ( r2.ur - r2.r ) / (1 - r2.ur) * (N-K-1) / G

F

## [1] 9.550254

# p-value of the F test

1 - pf(F, G, N-K-1)

## [1] 4.473708e-06