Simple OLS Regression

- Section 2.1 of Heiss (2020)

- Consider the following empirical model: $$ y = \beta_0 + \beta_1 x + u \tag{2.1} $$

- According to Wooldridge (2006, Section 2.2), the ordinary least squares (OLS) estimators are given by

- The fitted (predicted) values, $\hat{y}$, are given by $$ \hat{y} = \hat{\beta}_0 + \hat{\beta}_1 x \tag{2.4} $$ such that $$ y = \hat{y} + \hat{u} $$

Example 2.3: CEO Compensation and Stock Returns (Wooldridge, 2006)

- Consider the following simple regression model:

$$ \text{salary} = \beta_0 + \beta_1 \text{roe} + u $$

where

salaryis CEO compensation in thousands of dollars androeis the return on equity, measured in percentage points.

Estimating Simple Regression “By Hand”

# Load the dataset from the 'wooldridge' package

data(ceosal1, package="wooldridge")

attach(ceosal1) # avoids writing 'ceosal1$' before every variable

cov(salary, roe) # covariance between the dependent and independent variables

## [1] 1342.538

var(roe) # variance of the return on equity

## [1] 72.56499

mean(roe) # mean return on equity

## [1] 17.18421

mean(salary) # mean salary

## [1] 1281.12

# Compute the OLS coefficients "by hand"

( b1_hat = cov(salary, roe) / var(roe) ) # by (2.3)

## [1] 18.50119

( b0_hat = mean(salary) - var(roe)*mean(salary) ) # by (2.2)

## [1] -91683.31

detach(ceosal1) # stop looking for variables inside the 'ceosal1' object

- We see that a one-percentage-point increase in return on equity (

roe) is associated with an increase of about 18 thousand dollars in CEO compensation.

Estimating Simple Regression with lm()

- A more convenient way to estimate an OLS model is to use the

lm()function. - In a univariate model, we write the dependent and independent variables separated by a tilde (

~):

lm(ceosal1$salary ~ ceosal1$roe)

##

## Call:

## lm(formula = ceosal1$salary ~ ceosal1$roe)

##

## Coefficients:

## (Intercept) ceosal1$roe

## 963.2 18.5

- We can also omit the

ceosal1$prefix by supplyingdata = ceosal1.

lm(salary ~ roe, data=ceosal1)

##

## Call:

## lm(formula = salary ~ roe, data = ceosal1)

##

## Coefficients:

## (Intercept) roe

## 963.2 18.5

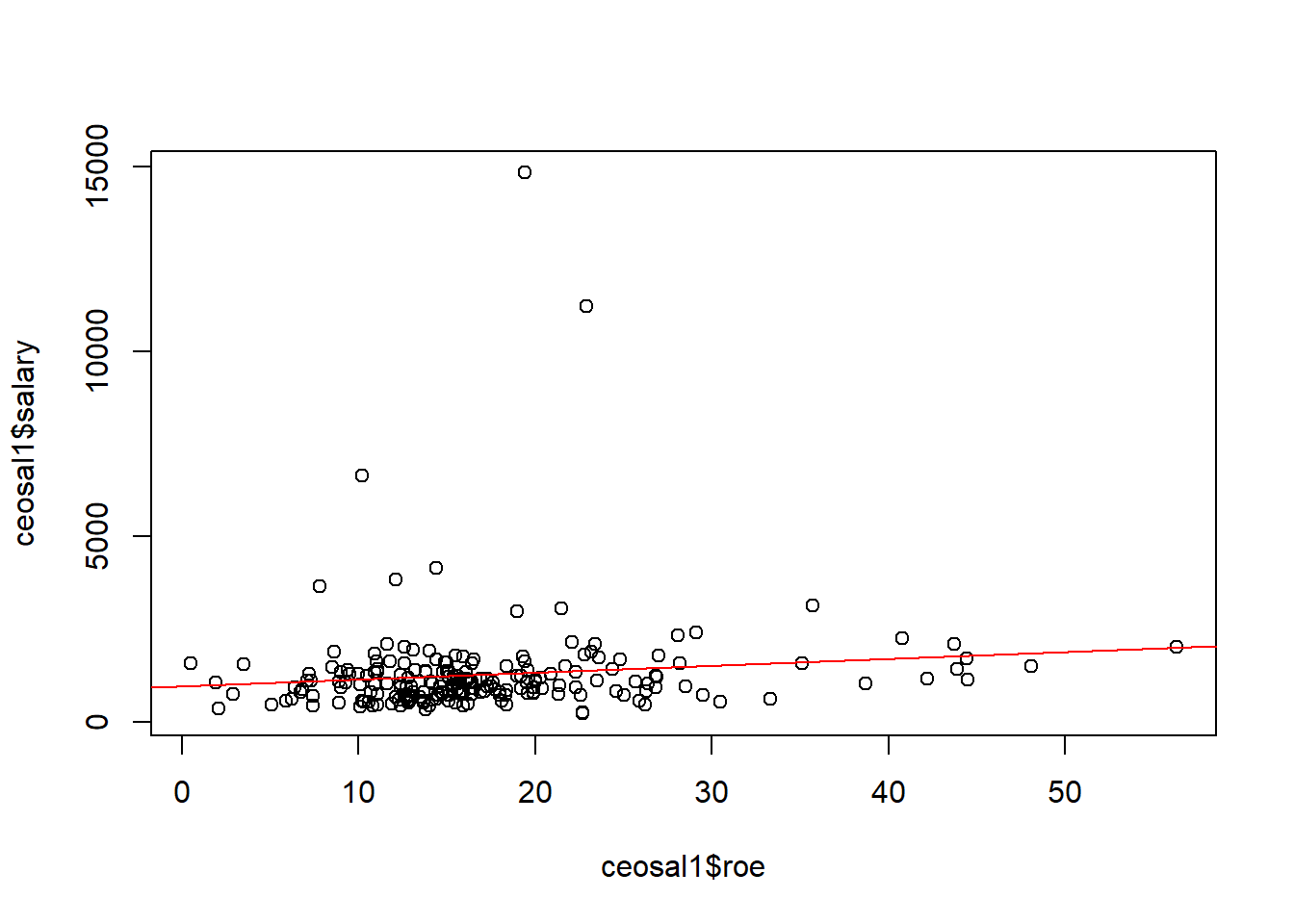

- We can use

lm()to add the regression line to a scatterplot.

# Scatterplot

plot(ceosal1$roe, ceosal1$salary)

# Add the regression line

abline(lm(salary ~ roe, data=ceosal1), col="red")

Coefficients, Fitted Values, and Residuals

- Section 2.2 of Heiss (2020)

- We can store the estimation results in an object (a

list) and then extract information from it.

# Store the regression results in an object

CEOregres = lm(salary ~ roe, data=ceosal1)

# Check the names of the components stored in the object

names(CEOregres)

## [1] "coefficients" "residuals" "effects" "rank"

## [5] "fitted.values" "assign" "qr" "df.residual"

## [9] "xlevels" "call" "terms" "model"

- We can use

coef()to extract the estimated regression coefficients.

( bhat = coef(CEOregres) )

## (Intercept) roe

## 963.19134 18.50119

bhat_0 = bhat["(Intercept)"] # or bhat[1]

bhat_1 = bhat["roe"] # or bhat[2]

- Given these estimated parameters, we can calculate the fitted values, $\hat{y}$, and the residuals, $\hat{u}$, for each observation $i=1, ..., n$:

# Extract ceosal1 columns as vectors

sal = ceosal1$salary

roe = ceosal1$roe

# Compute fitted values

sal_hat = bhat_0 + (bhat_1 * roe)

# Compute residuals

u_hat = sal - sal_hat

# Display the first 6 rows of sal, roe, sal_hat, and u_hat

head( cbind(sal, roe, sal_hat, u_hat) )

## sal roe sal_hat u_hat

## [1,] 1095 14.1 1224.058 -129.0581

## [2,] 1001 10.9 1164.854 -163.8543

## [3,] 1122 23.5 1397.969 -275.9692

## [4,] 578 5.9 1072.348 -494.3483

## [5,] 1368 13.8 1218.508 149.4923

## [6,] 1145 20.0 1333.215 -188.2151

- With

fitted()andresid(), we can extract the fitted values and residuals directly from the regression object:

head( cbind(fitted(CEOregres), resid(CEOregres)) )

## [,1] [,2]

## 1 1224.058 -129.0581

## 2 1164.854 -163.8543

## 3 1397.969 -275.9692

## 4 1072.348 -494.3483

## 5 1218.508 149.4923

## 6 1333.215 -188.2151

# Or equivalently

head( cbind(CEOregres$fitted.values, CEOregres$residuals) )

## [,1] [,2]

## 1 1224.058 -129.0581

## 2 1164.854 -163.8543

## 3 1397.969 -275.9692

## 4 1072.348 -494.3483

## 5 1218.508 149.4923

## 6 1333.215 -188.2151

In Section 2.3 of Wooldridge (2006), OLS estimation implies the following sample properties: \begin{align} &\sum^n_{i=1}{\hat{u}_i} = 0 \quad \implies \quad \bar{\hat{u}} = 0 \tag{2.7} \\ &\sum^n_{i=1}{x_i \hat{u}_i} = 0 \quad \implies \quad Cov(x,\hat{u}) = 0 \tag{2.8} \\ &\bar{y}=\hat{\beta}_0 + \hat{\beta}_1.\bar{x} \tag{2.9} \end{align}

We can verify them in our example:

# Checking (2.7)

mean(u_hat) # very close to 0

## [1] -2.666235e-14

# Checking (2.8)

cor(ceosal1$roe, u_hat) # very close to 0

## [1] -6.038735e-17

# Checking (2.9)

mean(ceosal1$salary)

## [1] 1281.12

mean(sal_hat)

## [1] 1281.12

- IMPORTANT: This only means that OLS chooses $\hat{\beta}_0$ and $\hat{\beta}_1$ so that 2.7, 2.8, and 2.9 hold in the sample.

- This does NOT mean that the following population assumptions are necessarily true: \begin{align} &E(u) = 0 \tag{2.7'} \\ &Cov(x, u) = 0 \tag{2.8'} \end{align}

- In fact, if 2.7’ and 2.8’ do not hold, OLS estimation will be biased.

Log Transformations

- Section 2.4 of Heiss (2020)

- We can also estimate models after transforming variables from levels into logarithms.

- This is especially useful for turning nonlinear models into linear ones, such as when the parameter appears in the exponent rather than multiplicatively:

$$ y = A K^\alpha L^\beta\quad \overset{\text{log}}{\rightarrow}\quad \log(y) = \log(A) + \alpha \log(K) + \beta \log(L) $$

- Log transformations are also commonly used for dependent variables with $y \ge 0$.

- There are two main ways to apply a log transformation:

- create a new vector/column containing the logged variable, or

- use the

log()function directly insidelm().

Example 2.11: CEO Compensation and Firm Sales (Wooldridge, 2006)

Consider the variables:

wage: annual salary, in thousands of dollarssales: firm sales, in millions of dollars

Level-level model:

# Load the dataset

data(ceosal1, package="wooldridge")

# Estimate the level-level model

lm(salary ~ sales, data=ceosal1)

##

## Call:

## lm(formula = salary ~ sales, data = ceosal1)

##

## Coefficients:

## (Intercept) sales

## 1.174e+03 1.547e-02

- An increase of US$1 million in sales is associated with an increase of US$0.01547 thousand in CEO compensation.

- Log-level model:

# Estimate the log-level model

lm(log(salary) ~ sales, data=ceosal1)

##

## Call:

## lm(formula = log(salary) ~ sales, data = ceosal1)

##

## Coefficients:

## (Intercept) sales

## 6.847e+00 1.498e-05

- An increase of US$1 million in sales tends to raise CEO salary by about 0.0015% ($=100 \beta_1%$).

- Log-log model:

# Estimate the log-log model

lm(log(salary) ~ log(sales), data=ceosal1)

##

## Call:

## lm(formula = log(salary) ~ log(sales), data = ceosal1)

##

## Coefficients:

## (Intercept) log(sales)

## 4.8220 0.2567

- A 1% increase in sales is associated with an increase of about 0.257% in salary ($=\beta_1%$).

Regression Through the Origin and on a Constant

- Section 2.5 of Heiss (2020)

- To estimate the model without an intercept, we need to add

0 +to the regressors insidelm():

data(ceosal1, package="wooldridge")

lm(salary ~ 0 + roe, data=ceosal1)

##

## Call:

## lm(formula = salary ~ 0 + roe, data = ceosal1)

##

## Coefficients:

## roe

## 63.54

- If we regress a dependent variable on a constant only (

1), we obtain its sample mean.

lm(salary ~ 1, data=ceosal1)

##

## Call:

## lm(formula = salary ~ 1, data = ceosal1)

##

## Coefficients:

## (Intercept)

## 1281

mean(ceosal1$salary, na.rm=TRUE)

## [1] 1281.12

Difference in Means

- Based on Example C.6: the effect of job-training grants on worker productivity (Wooldridge, 2006).

- We can calculate a difference in means by regressing on a dummy variable that takes values 0 or 1.

- First, we create a single vector of scrap rates by stacking

SR87andSR88:

SR87 = c(10, 1, 6, .45, 1.25, 1.3, 1.06, 3, 8.18, 1.67, .98,

1, .45, 5.03, 8, 9, 18, .28, 7, 3.97)

SR88 = c(3, 1, 5, .5, 1.54, 1.5, .8, 2, .67, 1.17, .51, .5,

.61, 6.7, 4, 7, 19, .2, 5, 3.83)

( SR = c(SR87, SR88) ) # stack SR87 and SR88 into a single vector

## [1] 10.00 1.00 6.00 0.45 1.25 1.30 1.06 3.00 8.18 1.67 0.98 1.00

## [13] 0.45 5.03 8.00 9.00 18.00 0.28 7.00 3.97 3.00 1.00 5.00 0.50

## [25] 1.54 1.50 0.80 2.00 0.67 1.17 0.51 0.50 0.61 6.70 4.00 7.00

## [37] 19.00 0.20 5.00 3.83

- Note that the first 20 values refer to scrap rates in 1987 and the last 20 refer to 1988.

- Next, we create a dummy variable called

group88that assigns value 1 to observations from 1988 and 0 to observations from 1987:

( group88 = c(rep(0, 20), rep(1, 20)) ) # 0/1 values for the first/last 20 observations

## [1] 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

## [39] 1 1

- Regressing the scrap rate on the dummy yields the difference in means:

lm(SR ~ group88)

##

## Call:

## lm(formula = SR ~ group88)

##

## Coefficients:

## (Intercept) group88

## 4.381 -1.154

Expected Values, Variance, and Standard Errors

Wooldridge (2006, Section 2.5) derives the estimator of the error variance: $$ \hat{\sigma}^2 = \frac{1}{n-2} \sum^n_{i=1}{\hat{u}^2_i} = \frac{n-1}{n-2} Var(\hat{u}) \tag{2.14} $$ where $Var(\hat{u}) = \frac{1}{n-1} \sum^n_{i=1}{\hat{u}^2_i}$.

Notice that we need to account for degrees of freedom because we are estimating two parameters ( $\hat{\beta}_0$ and $\hat{\beta}_1$).

Note that $\hat{\sigma} = \sqrt{\hat{\sigma}^2}$ is called the standard error of the regression (SER). In R, this appears as the residual standard error.

We can also obtain the standard errors of the estimators:

Example 2.12: Student Math Performance and the School Lunch Program (Wooldridge, 2006)

Consider the variables:

math10: the percentage of tenth graders who pass a standardized math examlnchprg: the percentage of students eligible for the school lunch program

The simple regression model is $$ \text{math10} = \beta_0 + \beta_1 \text{lnchprg} + u $$

data(meap93, package="wooldridge")

# Estimate the model and store it in the object 'results'

results = lm(math10 ~ lnchprg, data=meap93)

# Extract the number of observations

( n = nobs(results) )

## [1] 408

# Compute the standard error of the regression (square root of 2.14)

( SER = sqrt( (n-1)/(n-2) ) * sd(resid(results)) )

## [1] 9.565938

# Standard error of bhat_0 (2.15)

(1 / sqrt(n-1)) * (SER / sd(meap93$lnchprg)) * sqrt( mean(meap93$lnchprg^2) ) # Standard error of bhat_0

## [1] 0.9975824

(1 / sqrt(n-1)) * (SER / sd(meap93$lnchprg)) # bhat_1

## [1] 0.03483933

- The standard-error calculations can also be obtained with the

summary()function applied to the regression object:

summary(results)

##

## Call:

## lm(formula = math10 ~ lnchprg, data = meap93)

##

## Residuals:

## Min 1Q Median 3Q Max

## -24.386 -5.979 -1.207 4.865 45.845

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 32.14271 0.99758 32.221 <2e-16 ***

## lnchprg -0.31886 0.03484 -9.152 <2e-16 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 9.566 on 406 degrees of freedom

## Multiple R-squared: 0.171, Adjusted R-squared: 0.169

## F-statistic: 83.77 on 1 and 406 DF, p-value: < 2.2e-16

- Also note that, by default,

summary()reports two-sided hypothesis tests whose null hypotheses are $\beta_0 = 0$ and $\beta_1=0$. - In other words, it tests whether the estimated coefficients are statistically equal to zero and reports the corresponding t statistics and p-values.

- In this case, the p-values are extremely small (

<2e-16, that is, smaller than $2 \times 10^{-16}$), so we reject both null hypotheses and conclude that the estimates are statistically significant. - We can also compute these statistics by hand:

# Extract the estimated coefficients

( estim = coef(summary(results)) )

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 32.1427116 0.99758239 32.220609 6.267302e-114

## lnchprg -0.3188643 0.03483933 -9.152422 2.746609e-18

# t statistics for H0: bhat = 0

( t_bhat_0 = (estim["(Intercept)", "Estimate"] - 0) / estim["(Intercept)", "Std. Error"] )

## [1] 32.22061

( t_bhat_1 = (estim["lnchprg", "Estimate"] - 0) / estim["lnchprg", "Std. Error"] )

## [1] -9.152422

# p-values for H0: bhat = 0

2 * (1 - pt(abs(t_bhat_0), n-1)) # p-value for bhat_0

## [1] 0

2 * (1 - pt(abs(t_bhat_1), n-1)) # p-value for bhat_1

## [1] 0

Assumption Violations

- Subsection 2.7.3 of Heiss (2020), but using the material from Worked Example 1.

- Simulating a linear model (John Hopkins/Coursera)

- In practice, we run regressions using observed data and do not know the true model that generated those observations.

- In R, however, we can posit a true data-generating process and simulate observations to study what happens when an econometric assumption is violated.

- We will use the example from Worked Example 1, where we want to study the relationship between hours of cooking practice and the number of kitchen burns.

No Assumption Violation: Example 1

- Let $y$ denote the number of kitchen burns and $x$ the number of hours spent learning how to cook.

- Suppose the true model is $$ y = a_0 + b_0 x + \varepsilon, \qquad \varepsilon \sim N(0, 2^2) \tag{1}$$ where $a_0=50$ and $b_0=-5$.

- Set

$a_0$ and

$b_0$, then simulate observations of

$x$ and

$y$.

- For convenience, we generate random draws from $x \sim N(5; 0.5^2)$. Here, the specific distribution of $x$ is not important.

a0 = 50

b0 = -5

N = 200 # number of observations

set.seed(1)

u = rnorm(N, 0, 2) # disturbances: 200 obs. with mean 0 and sd 2

x = rnorm(N, 5, 0.5) # 200 obs. with mean 5 and sd 0.5

y = a0 + b0*x + u # compute y from u and x

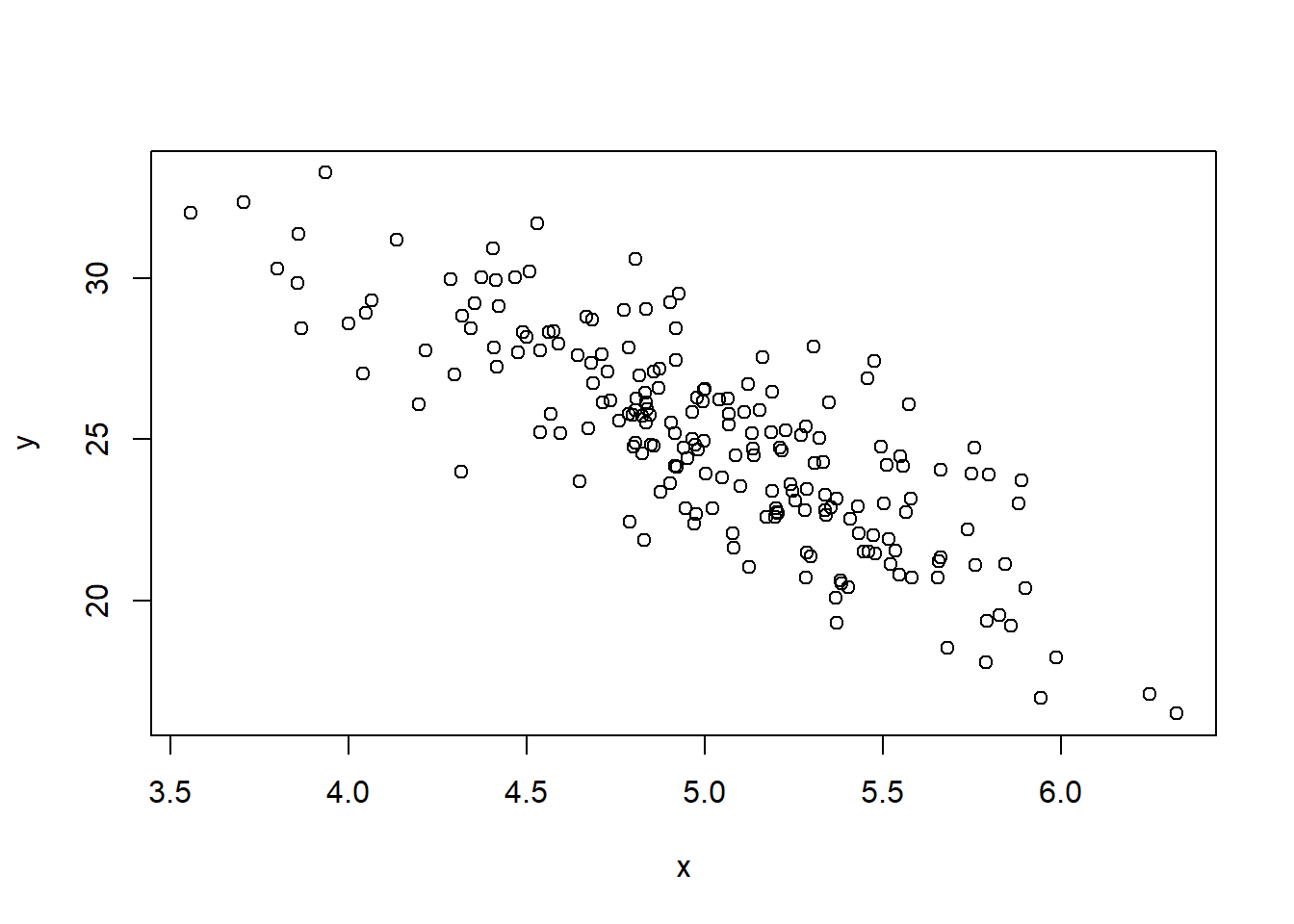

plot(x, y)

These simulated

$x$ and

$y$ values are the information we would observe in practice.

These simulated

$x$ and

$y$ values are the information we would observe in practice.- Estimate the parameters

$\hat{a}$ and

$\hat{b}$ by OLS using the simulated observations of

$y$ and

$x$.

- Suppose an economist writes the following empirical model: $$ y = a + b x + u, \tag{1a}$$ assuming that $E[u] = 0$ and $E[ux]=0$.

- To estimate the model by OLS, we use

lm().

lm(y ~ x) # regress y on x by OLS

##

## Call:

## lm(formula = y ~ x)

##

## Coefficients:

## (Intercept) x

## 50.463 -5.078

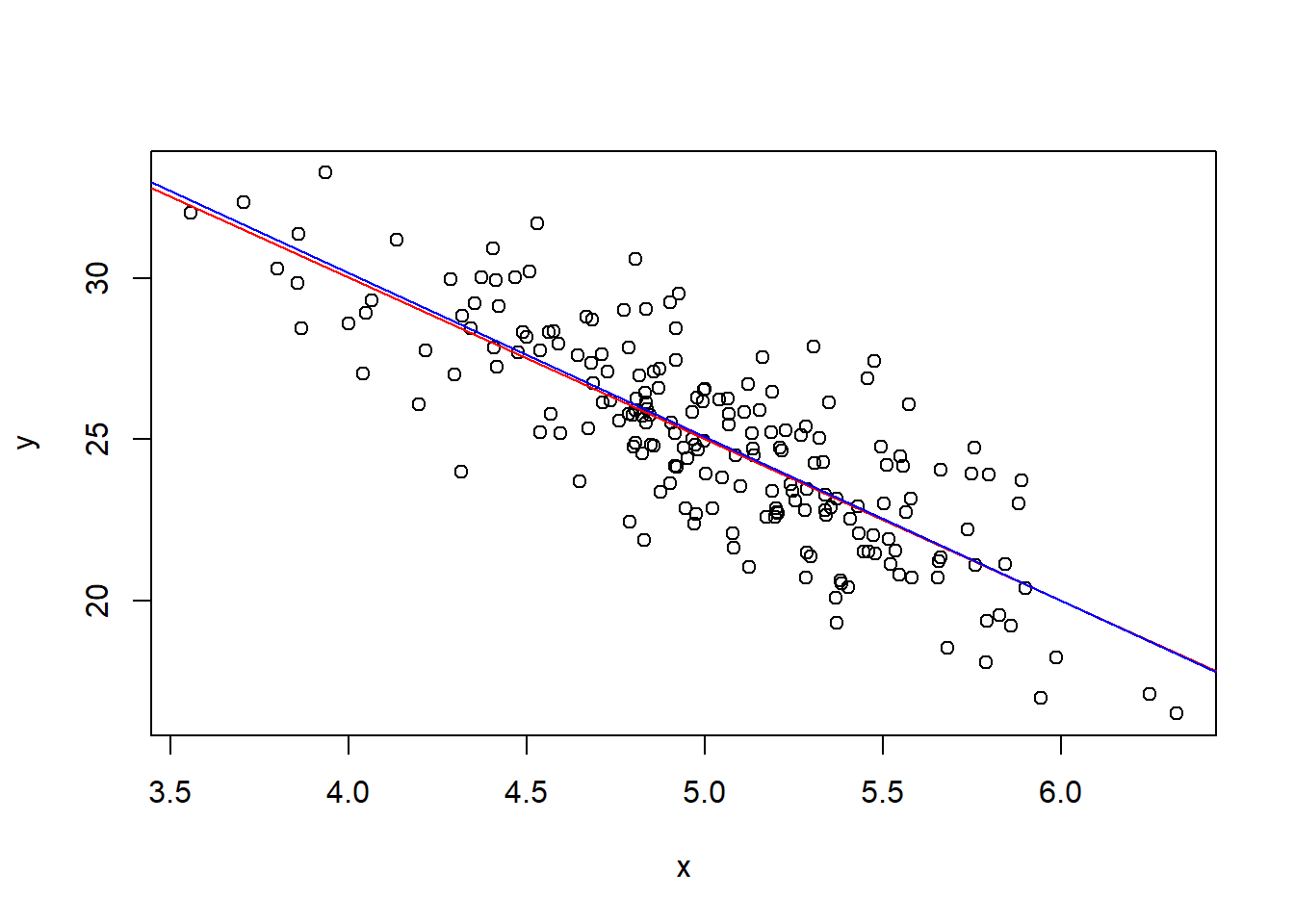

- Notice that the population parameters are recovered reasonably well ( $\hat{a} \approx 50 = a_0$ and $\hat{b} \approx -5 = b_0$).

plot(x, y) # plot x against y

abline(a=50, b=-5, col="red") # true model line

abline(lm(y ~ x), col="blue") # estimated line from the observed data

No Assumption Violation: Example 2

- Now suppose that, in the true model, the number of burns $y$ is determined both by hours of practice $x$ and by hours actually spent cooking $z$:

$$ y = a_0 + b_0 x + c_0 z + u, \qquad u \sim N(0, 2^2) \tag{2} $$ where $a_0=50$, $b_0=-5$, and $c_0=3$. For convenience, we generate random draws from $x \sim N(5; 0.5^2)$ and $z \sim N(1.875; 0.25^2)$. By construction, $z$ is uncorrelated with $x$ in the true model.

- First, let us simulate the observations:

a0 = 50

b0 = -5

c0 = 3

N = 200 # number of observations

set.seed(1)

u = rnorm(N, 0, 2) # disturbances: 200 obs. with mean 0 and sd 2

x = rnorm(N, 5, 0.5) # 200 obs. with mean 5 and sd 0.5

z = rnorm(N, 1.875, 0.25) # 200 obs. with mean 1.875 and sd 0.25

y = a0 + b0*x + c0*z + u # compute y from u, x, and z

Suppose an economist writes the following empirical model: $$ y = a + b x + u, \tag{2a}$$ assuming that $E[u] = 0$ and $E[ux] = 0$.

Notice that the economist omitted the hours-cooking variable $z$, so it is absorbed into the regression error term.

However, because $z$ is unrelated to $x$, this omission does not bias the estimate of $\hat{b}$:

cor(x, z) # correlation between x and z -> close to 0

## [1] -0.02625278

lm(y ~ x) # OLS estimation

##

## Call:

## lm(formula = y ~ x)

##

## Coefficients:

## (Intercept) x

## 56.27 -5.12

- Since $\hat{b} \approx -5 = b_0$, OLS successfully recovers the population parameter $b_0$ even though the economist excluded $z$ from the model.

- In many economic applications, the main goal is to estimate the relationship or causal effect between $y$ and $x$. We therefore do not need to include every variable that affects $y$, as long as $E(ux) = 0$ holds; that is, as long as no omitted explanatory variable correlated with $x$ is hiding inside the error term.

Violation of E(ux)=0

- Now suppose that, in the true model, the more someone practices cooking, the more time they actually spend cooking. In other words,

$x$ is related to

$z$.

- Assume that $z \sim N(1.875x; (0.25)^2)$:

set.seed(1)

e = rnorm(N, 0, 2) # disturbances: 200 obs. with mean 0 and sd 2

x = rnorm(N, 5, 0.5) # 200 obs. with mean 5 and sd 0.5

z = rnorm(N, 1.875*x, 0.25) # 200 obs. with mean 1.875x and sd 0.25

y = a0 + b0*x + c0*z + e # compute y from e, x, and z

cor(x, z) # correlation between x and z

## [1] 0.9618748

- Now $x$ and $z$ are strongly correlated.

- Estimate the empirical model $$ y = a + b x + u,$$ assuming that $E[u] = 0$ and $E[ux]=0$.

lm(y ~ x) # OLS estimation

##

## Call:

## lm(formula = y ~ x)

##

## Coefficients:

## (Intercept) x

## 50.6406 0.5053

- Here, $\hat{b} = 0.5 \neq -5 = b_0$. This happens because $z$ was omitted from the model and is therefore absorbed into the residual $\hat{u}$. Since $z$ is correlated with $x$, we have $E(ux)\neq 0$, which violates the key OLS exogeneity assumption.

- If we include $z$ in the regression, we recover an estimate close to $b_0$:

lm(y ~ x + z)

##

## Call:

## lm(formula = y ~ x + z)

##

## Coefficients:

## (Intercept) x z

## 50.435 -5.953 3.470

Violation of E(u)=0

- Now assume that $E[u] = k$, where $k \neq 0$ is a constant.

- Let $k = 10$:

a0 = 50

b0 = -5

k = 10

set.seed(1)

u = rnorm(N, k, 2) # disturbances: 200 obs. with mean k and sd 2

x = rnorm(N, 5, 0.5) # 200 obs. with mean 5 and sd 0.5

y = a0 + b0*x + u # compute y from u and x

- If an economist estimates an empirical model that imposes $E[u] = 0$, then:

lm(y ~ x) # OLS estimation

##

## Call:

## lm(formula = y ~ x)

##

## Coefficients:

## (Intercept) x

## 60.463 -5.078

- Notice that $E[u] \neq 0$ affects the intercept estimate, so $\hat{a} \neq a_0$, but it does not affect $\hat{b} \approx b_0$, which is usually the parameter of primary interest in economic applications.

Violation of Homoskedasticity

- Now suppose that $u \sim N(0, (2x)^2)$, so the variance increases with $x$. In other words, the error variance depends on $x$, and homoskedasticity fails.

a0 = 50

b0 = -5

set.seed(1)

x = rnorm(N, 5, 0.5) # 200 obs. with mean 5 and sd 0.5

u = rnorm(N, 0, 2*x) # disturbances with sd equal to 2x

y = a0 + b0*x + u # compute y from u and x

lm(y ~ x) # OLS estimation

##

## Call:

## lm(formula = y ~ x)

##

## Coefficients:

## (Intercept) x

## 51.221 -5.166

- Even with heteroskedasticity, we can still recover $\hat{b} \approx b_0$ in this simulation. But with a smaller sample, it becomes more likely that $\hat{b} \neq b_0$. Try repeating the exercise with smaller values of $N$.

Goodness of Fit

- Section 2.3 of Heiss (2020)

- The total sum of squares (TSS), explained sum of squares (ESS), and residual sum of squares (RSS) can be written as

\begin{align} SQT &= \sum^n_{i=1}{(y_i - \bar{y})^2} = (n-1) . Var(y) \tag{2.10}\\ SQE &= \sum^n_{i=1}{(\hat{y}_i - \bar{y})^2} = (n-1) . Var(\hat{y}) \tag{2.11}\\ SQR &= \sum^n_{i=1}{(\hat{u}_i - 0)^2} = (n-1) . Var(\hat{u}) \tag{2.12} \end{align} where $Var(x) = \frac{1}{n-1} \sum^n_{i=1}{(x_i - \bar{x})^2}$.

- Wooldridge (2006) defines the coefficient of determination as \begin{align} R^2 &= \frac{SQE}{SQT} = 1 - \frac{SQR}{SQT}\\ &= \frac{Var(\hat{y})}{Var(y)} = 1 - \frac{Var(\hat{u})}{Var(y)} \tag{2.13} \end{align} because $SQT = SQE + SQR$.

# Compute R^2 in three equivalent ways:

var(sal_hat) / var(sal)

## [1] 0.01318862

1 - var(u_hat)/var(sal)

## [1] 0.01318862

cor(sal, sal_hat)^2 # squared correlation between the dependent variable and fitted values

## [1] 0.01318862

- A more convenient way to obtain

$R^2$ is to use

summary()on the regression object. This produces a more detailed regression table, including $R^2$:

summary(CEOregres)

##

## Call:

## lm(formula = salary ~ roe, data = ceosal1)

##

## Residuals:

## Min 1Q Median 3Q Max

## -1160.2 -526.0 -254.0 138.8 13499.9

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 963.19 213.24 4.517 1.05e-05 ***

## roe 18.50 11.12 1.663 0.0978 .

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 1367 on 207 degrees of freedom

## Multiple R-squared: 0.01319, Adjusted R-squared: 0.008421

## F-statistic: 2.767 on 1 and 207 DF, p-value: 0.09777